Average Car, House, and Contents Insurance Cost NZ 2026

Are insurance bills burning a hole in your back pocket in 2026? If so, you're not alone.

Whether you're in Auckland, Wellington or Christchurch, premiums have been climbing significantly in recent years, and Kiwis everywhere are asking the same question: what's happening, and why?

We look at the latest Quashed data on car, house, and contents insurance premiums across New Zealand. Our insights highlight trends on insurance premium changes, based on our latest market data.

You'll discover in this article how much NZ consumers are paying on average for their car insurance, house insurance, and contents insurance. We also breakdown the costs of these insurance across the Auckland, Wellington and Christchurch region.

KEY FINDING: The $1,560 "Loyalty Tax"

Kiwis who don't shop around for insurance are paying an average "loyalty tax" of $1,560 per year across their car, house, and contents policies combined. This represents the difference between staying with your current insurer and finding the best available rates in Q1 2026. The average New Zealand household paying for all three insurance types (house, car, and contents) now faces a combined annual cost of $5,020, largely unchanged from last year and 29% higher than three years ago in Q1 2023.

Average Cost of Comprehensive Car Insurance in New Zealand

The average cost of comprehensive car insurance across New Zealand is $1,267 per year (or $106 per month) as of our latest Q1 2026 Quashed Index data published in April 2026. The data in this section covers comprehensive policies only. Costs for third party, fire and theft (TPFT) or third party only (TPO) policies will differ. The cost of comprehensive car insurance in New Zealand has increased significantly over recent years, as shown below.

Average comprehensive car insurance premiums (2023 - 2026)

Year Ended | Yearly Costs ($) | Year-on-Year Difference ($) |

Q1 2023 | $950 | - |

Q1 2024 | $1,311 | + $361 |

Q1 2025 | $1,271 | - $40 |

Q1 2026 | $1,267 | - $4 |

Important trend: Car insurance premiums have now been declining for two consecutive periods after the sharp 38% spike in Q1 2024. That said, car owners rolling over their existing policies are still seeing an average 3% increase at renewal, so shopping around remains important.

The bigger picture: Despite recent easing, comprehensive car insurance still costs 33% more than it did three years ago in Q1 2023, when the national average was just $950. That's an extra $317 per year that Kiwi drivers are now paying compared to 2023.

Average regional differences in comprehensive car insurance premiums

Comprehensive car insurance costs vary by location. Auckland car owners now pay roughly $1,478 per year, or $123 per month on average, for comprehensive car insurance. In comparison, Wellington drivers pay about $1,115 per year ($93 monthly), while in Canterbury, the average cost is approximately $1,166 annually or $97 monthly. Q1 2026 data is shown below:

Average comprehensive car insurance premiums by region (Q1 2026)

Region | Yearly Costs ($) | Monthly Costs ($) |

National | $1,267 | $106 |

Auckland | $1,478 | $123 |

Canterbury | $1,166 | $97 |

Wellington | $1,115 | $93 |

Why do car insurance costs vary so much by location?

According to Quashed CEO Justin Lim, it comes down to risk. “In densely populated cities like Auckland, where vehicle numbers have been increasing, there’s a higher likelihood of accidents, and this is reflected in car insurance premiums,” explains Lim. He adds, “Areas with high rates of car theft or vandalism also face higher costs. Finally, natural disasters like floods force insurers to adjust premiums to manage these risks more effectively.”

Got questions? Be sure to check out our Car Insurance FAQs at the end of this article.

How much could Kiwis save by comparing comprehensive car insurance providers?

The gap between the average highest and lowest comprehensive car insurance premiums offered across insurers we display on Quashed has widened over time. In Q1 2026, consumers who shopped their comprehensive car insurance with the Quashed Market Scan found a cheaper policy 81% of the time, with average savings of $377 per year.

Average comprehensive car insurance premium differences across insurers (2022 - 2025)

Year Ended | Yearly Difference ($) | Year-on-Year Increase % |

Q1 2022 | $356 | — |

Q1 2023 | $447 | + 26% |

Q1 2024 | $756 | + 69% |

Q1 2025 | $679 | - 11% |

Want to save on your car insurance? Our Further Reading section at the end of this article covers expert tips on car, house, and contents insurance.

Average Cost of House Insurance in New Zealand

The average cost of house insurance in New Zealand is $2,949 per year (or $246 per month) as of Q1 2026, based on Quashed Index data published in April 2026. Let’s take a look at how house insurance costs have changed over the past few years.

Average house insurance premiums (2023 - 2026)

Year Ended | Yearly Costs ($) | Year-on-Year Difference ($) |

Q1 2023 | $2,247 | — |

Q1 2024 | $2,785 | + $538 |

Q1 2025 | $2,898 | + $113 |

Q1 2026 | $2,949 | + $51 |

Important trend: House insurance premiums have now risen for three consecutive periods, though the rate of increase continues to slow, from +24% in Q1 2024, to +4% in Q1 2025, to +2% in Q1 2026. While the pace is easing, house insurance remains the most expensive of the three policy types and the only one still trending upward year-on-year.

The bigger picture: Over the past three years, house insurance premiums have risen 31%, adding $702 to the average annual premium since Q1 2023. For homeowners in Wellington, where premiums already sit at $4,738 per year, the cumulative impact is especially significant.

Regional differences in house insurance costs (Q1 2026)

Homeowners in Auckland pay an average of $2,063 per year ($172 per month) for house insurance. While this may seem high, it’s actually below the national average of $2,949. Wellington homeowners pay significantly more, with an average annual premium of $4,738 ($395 per month), more than twice that of Auckland. And Christchurch homeowners sit in the middle, with their average annual house insurance premiums at $2,903 ($242 per month).

Region | Yearly Costs ($) | Monthly Costs ($) |

National | $2,949 | $246 |

Auckland | $2,063 | $172 |

Canterbury | $2,903 | $242 |

Wellington | $4,738 | $395 |

Want to see how your house insurance stacks up? Use the Quashed Market Scan to compare providers in minutes. Our Further Reading section at the end of this article also covers expert tips on car, house, and contents insurance.

How much could Kiwis save by comparing house insurance?

House insurance premiums aren't one-size-fits-all. They vary a lot depending on your insurer and policy. In Q1 2026, Quashed users who shopped their house insurance with the Quashed Market Scan found a cheaper policy 67% of the time, with average savings of $908 per year. If you haven't compared your house insurance recently, it's worth running a scan to see where you stand.

Average house insurance premium differences across insurers (2022 - 2025)

Year Ended | Yearly Difference ($) | Year-on-Year Increase % |

Q1 2022 | $605 | — |

Q1 2023 | $799 | + 32% |

Q1 2024 | $975 | + 22% |

Q1 2025 | $1,143 | + 17% |

Got questions? Be sure to check out our House Insurance FAQs at the end of the blog.

Average Cost of Contents Insurance in New Zealand

The average cost of contents insurance in New Zealand is $804 per year ($67 per month) as of Q1 2026, based on Quashed Index data. Prices have climbed over time, reflecting the broader insurance trends in NZ, though contents premiums have recently started to ease.

Average contents insurance premiums (2023 - 2026)

Year Ended | Yearly Costs ($) | Year-on-Year Difference ($) |

Q1 2023 | $688 | — |

Q1 2024 | $852 | + $164 |

Q1 2025 | $828 | - $24 |

Q1 2026 | $804 | - $24 |

Important trend: Contents insurance is now the only insurance type to show sustained year-on-year declines, dropping 3% from Q1 2025 to Q1 2026. This is good news for renters and homeowners looking to keep costs down. Interestingly, the average contents insurance sum insured amount jumped 20% compared to a year ago, with the biggest increase observed in the under-30 age group, suggesting younger Kiwis are insuring more of their belongings.

The bigger picture: Even with two consecutive years of decline, contents insurance is still 17% higher than it was in Q1 2023, when the average premium was $688. That's an extra $116 per year. The recent easing is welcome, but premiums have not returned anywhere near pre-2024 levels.

Regional differences in contents insurance costs (Q1 2026)

Aucklanders are paying an average of $676 per year ($56 per month). Meanwhile, Wellingtonians face the highest contents insurance premiums, averaging $995 per year ($83 per month). Christchurch homeowners and renters can expect to pay roughly $790 per year ($66 per month).

Region | Yearly Costs ($) | Monthly Costs ($) |

National | $804 | $67 |

Auckland | $676 | $56 |

Canterbury | $790 | $66 |

Wellington | $995 | $83 |

Wondering if you could get a better deal on your contents insurance? Compare providers with the Quashed Market Scan. And be sure to check out our Contents Insurance FAQs at the end of this article.

How much could Kiwis save by comparing contents insurance?

Based on our latest data, we've found that premiums for contents insurance vary widely across insurers. In Q1 2026, consumers who shopped their contents insurance with the Quashed Market Scan found a cheaper policy 76% of the time, with average savings of $275 per year. Run a free scan on Quashed to see if you could be paying less.

Average contents insurance premium differences across insurers (2022 - 2025)

Year Ended | Yearly Difference ($) | Year-on-Year Increase % |

Q1 2022 | $267 | — |

Q1 2023 | $336 | + 26% |

Q1 2024 | $461 | + 37% |

Q1 2025 | $431 | - 6% |

How Insurance Costs Vary by Age Group

Not all Kiwis are feeling the same pinch. The Q1 2026 Quashed Index reveals a clear pattern: the over-50 age groups have experienced the sharpest premium increases over the past year and the past three years, in both dollar and percentage terms.

Average general insurance costs by age group (Q1 2026)

Age Group | Yearly Cost ($) | 1-Year Change | 3-Year Change |

25-30 | $4,722 | -$26 (-0.5%) | +$1,204 (+34%) |

31-39 | $4,795 | +$22 (+0.4%) | +$968 (+25%) |

40-50 | $5,019 | +$10 (+0.2%) | +$1,142 (+29%) |

51-60 | $5,111 | +$133 (+3%) | +$1,107 (+28%) |

61+ | $5,106 | +$100 (+2%) | +$1,316 (+35%) |

Younger consumers (under 40) saw their premiums hold steady or even dip slightly over the past year. Meanwhile, those aged 51-60 experienced the largest dollar increase at $133, and the 61+ group saw the biggest three-year jump at $1,316 (35%). This raises an important question: is loyalty costing older Kiwis more?

If you’re over 50, it’s especially worth running a Quashed Market Scan to check whether you could be paying less. The data suggests that younger, more active shoppers may be keeping their premiums in check by comparing more often.

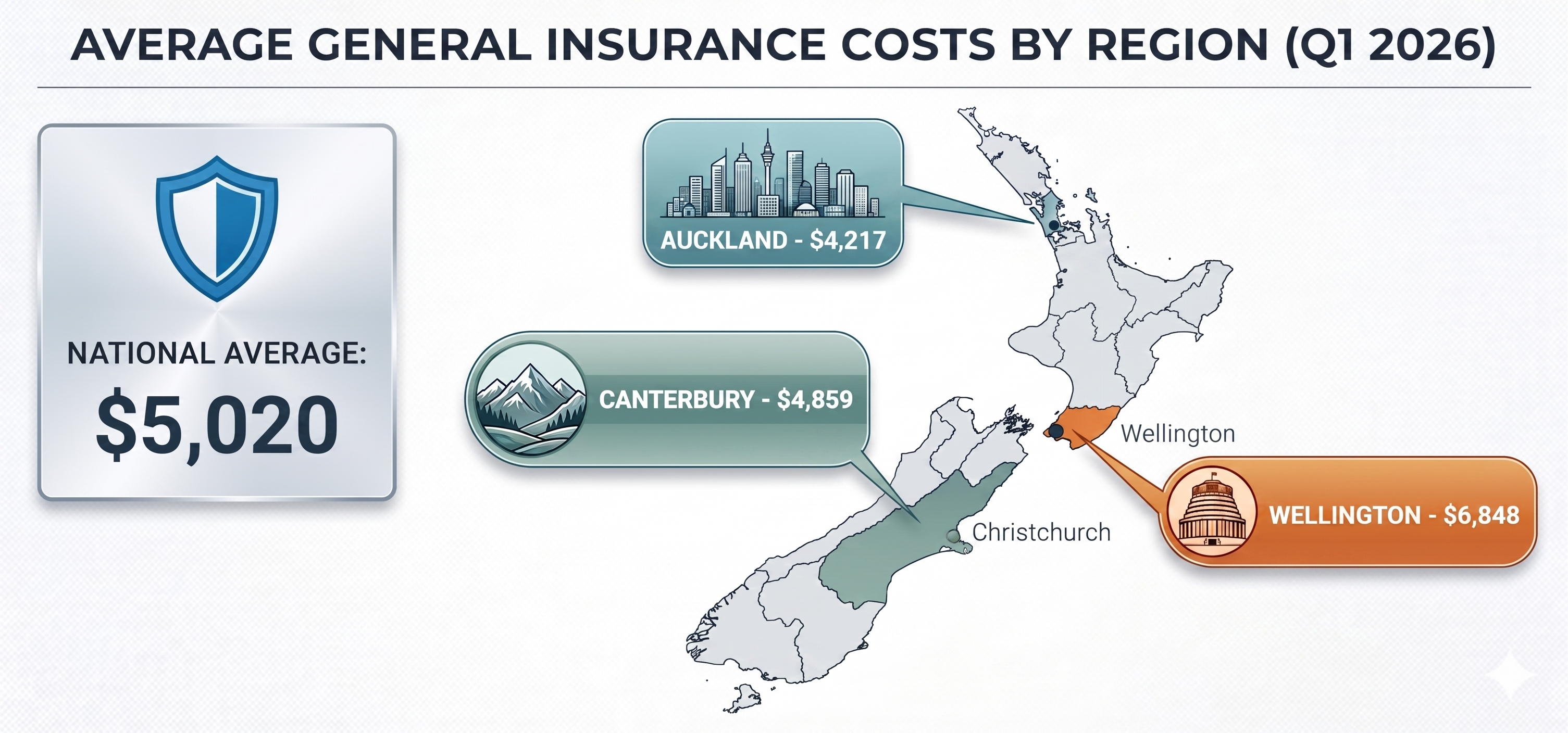

Combined Insurance Costs by Region

When you add up house, car (comprehensive), and contents insurance, the regional differences become stark. Here’s what the average Kiwi household is paying across all three policies in Q1 2026:

Average general insurance costs by region (Q1 2026)

Region | Yearly Cost ($) | Year-on-Year Change |

National | $5,020 | No change |

Auckland | $4,217 | -4% |

Canterbury | $4,859 | -1% |

Wellington | $6,848 | +1% |

Wellington households are paying $6,848 per year for general insurance, more than $2,600 above what Auckland households pay. This gap is driven primarily by Wellington’s significantly higher house insurance costs, which reflect the region’s earthquake and weather-related risk profile. Auckland, despite being the most expensive region for car insurance, actually has the lowest combined general insurance costs of the three main centres.

Wherever you’re based, comparing across multiple insurers is one of the most effective ways to manage these costs. Use the Quashed Market Scan to see how your premiums stack up.

What Kiwis can do to keep insurance costs affordable

1. Shop for insurance across 4-5 insurers

Comparing more options increases the likelihood you’ll find a cheaper and/or better policy. For example, comprehensive cover for a 2020 Toyota Corolla in Auckland can cost between $960 and $1,790. That’s a significant $830 difference across five insurance providers. Use the Quashed Market Scan to compare your options in minutes.

2. Reduce your sum insured and increase your excess

Reducing your sum insured to reflect current value (as appropriate) and increasing your excess to a higher amount you can afford will lower your premiums. For example, adjusting the sum insured for the Toyota Corolla from $24,000 to $22,000 and the excess from $500 to $1,500 reduces premiums to between $673 and $1,258, saving up to 30%. You can do this easily using the Quashed Market Scan and instantly see potential savings!

3. Switch to a lower tier of cover

If you’re thinking about cancelling your policy due to cost, consider switching to a lower tier of cover instead. It can significantly reduce costs while keeping some level of insurance in place. For example, switching from comprehensive to third party, fire and theft insurance reduces premiums on average by 40-60%. A third party, fire and theft policy would cost $580 to $690 for the Toyota Corolla.

Quashed’s Quarterly Insurance Index

The Quashed Insurance Index is a quarterly publication. The aim of this is to provide NZ consumers and NZ agencies with a benchmark for the cost of insurance in and across New Zealand. The data and insights published are based on tens of thousands of insurance premiums and quotes our platform retrieves across insurance companies in NZ.

Further reading

Car insurance

Car Insurance Guide: Learn the essentials of car insurance.

Saving on Car Insurance: Smart ways to lower your premiums.

Sorting Out Your Car Insurance Renewal: Stay on top of your renewal.

Cheapest Versus Best Car Insurance: Find the right balance.

Car Insurance Quotes: Get the best deal for you.

House insurance

House Insurance Guide: Understand the key basics.

Climate Change and House Insurance: How it impacts your cover.

Why Are House Insurance Premiums Increasing?: What’s driving the rise.

House Insurance Key Considerations: What to look out for.

8 Budget Hacks for House Insurance: Save without cutting corners.

Contents insurance

Complete Guide to Contents Insurance: Everything you need to know.

Key Considerations with Contents Insurance: Find coverage options.

Saving on Contents Insurance: Simple tips to reduce costs.

Contents Insurance Tips for Kiwi Seniors: Special advice for senior Kiwis.

Car insurance FAQs

Why have my car insurance premiums increased so much in NZ?

Premiums can rise due to factors like higher repair costs, inflation, and natural disasters. Even small claims or changes in your area can impact your premium. If you’re seeing a sudden spike, it’s a good idea to shop around to see if you can find a better deal.

Is shopping around for my car insurance really worth the effort?

Absolutely. Shopping around helps you find the best deal. At Quashed, we simplify this by providing real-time comparisons of various providers. It’s easy to find the right coverage at the best price with just a few clicks.

What factors should I consider when choosing an insurer?

Don’t just focus on price. Look at the coverage options, customer service, and how easy it is to make a claim. Consider the excess amount and whether the policy suits your needs. Make sure you’re not paying for coverage you don’t need.

Do loyalty discounts actually make a difference in my premiums?

Not always. Insurers often offer the best rates to new customers. Long-term customers may not get the same deal, so it’s worth comparing prices each year to avoid paying the “loyalty tax.”

What’s the impact of a claims history on my insurance premiums?

A history of claims can increase your premiums, as insurers view it as a higher risk. If you’ve been claim-free for a while, it could work in your favour when it’s time for renewal.

How does the value of my car or home affect my premiums?

The higher the value of your assets, the higher your premiums. This is because it costs more to repair or replace expensive cars and homes. Insurers base premiums on the potential cost to fix or replace your items.

Does my car’s safety rating impact the cost of my insurance?

Yes, safer cars with better ratings (like airbags and stability control) can lower your premiums. Insurers consider these features because safer cars are less likely to be involved in serious accidents, resulting in fewer claims.

House insurance FAQs

How can I avoid overpaying for house insurance?

Make sure you’re not over-insuring. Check that your sum insured reflects the actual cost of rebuilding your home, not the market value. Be mindful of unnecessary add-ons, and consider increasing your excess to lower premiums. Shopping around each year can also help ensure you’re getting the best deal.

How can I find discounts or better deals on my insurance premium?

Quashed makes finding discounts easy by providing real-time comparisons from different providers. You can also save by bundling policies, adjusting your coverage, or installing security systems.

Contents insurance FAQs

How do insurance providers determine the cost of my contents insurance?

The cost is determined by factors like the value of the items you’re insuring and the risk associated with your location. Insurers consider whether your home is secure (e.g., alarms or security systems) and the likelihood of claims in your area, like crime rates or natural disaster risks.

Why should renters consider contents insurance?

Renters should consider contents insurance to protect their personal belongings from unexpected events like theft, fire, or accidental damage. Even if you’re not responsible for the building itself, your possessions (furniture, electronics, clothing, etc.) are valuable, and contents insurance can help replace them if something goes wrong.

General insurance FAQs

How do natural disasters and global events impact insurance costs in NZ?

Natural disasters like floods or earthquakes can drive up premiums due to the increased risk. Global events, such as rising reinsurance costs from worldwide disasters, can also affect premiums in New Zealand.

Is it better to increase my excess to save on premiums?

Increasing your excess can lower your premium, but it’s important to find a balance. A higher excess means you pay more out of pocket if you need to make a claim. If you rarely claim, a higher excess can save you money, but if you expect to claim soon, keep it lower.

What do I need to know about regional variations in insurance premiums in NZ?

Premiums can vary depending on where you live. Areas prone to natural disasters, high crime rates, or higher repair costs typically have higher premiums. Even the cost of materials and labour can affect premiums based on location.