Sorting your insurance is often pushed to the bottom of the to-do list—fair enough. But comparing car, home, and contents insurance in NZ doesn’t have to be overwhelming. With Quashed, you can quickly compare policies, avoid overpaying, and make smarter decisions.

Sound familiar? Sound painful? Insurance shouldn’t be this way (even though it was born this way—sorry, Lady Gaga). That’s exactly why we built Quashed—to make comparing insurance in New Zealand quick, simple, and stress-free. Whether you’re looking to cut costs or check if your cover still stacks up, we help you make smart, informed choices—without the hassle.

Let’s take a closer look at why comparing insurance matters—and how Quashed makes it easier than ever to find the right cover.

Why compare car, house, and contents insurance in NZ?

Look, we all know insurance is personal—what works for your mate down the road might not work for you.

It really comes down to your own situation, budget, and what you need cover for. That’s why it’s important to compare insurance in New Zealand and find a policy that truly fits your needs. Taking a proper look at different insurance providers means you can:

Stop paying too much for cover you don't actually need

Spot better deals and extra benefits you might've missed

Feel confident you've got the right protection sorted

So, what are Kiwis actually paying for insurance? Let’s take a look at the numbers to understand how insurance costs are tracking and what you might expect.

How much are Kiwis paying for insurance?

We know insurance can feel like a mystery, so we've crunched the numbers in our latest Quashed Index to give you a clearer picture of where things stand.

Insurance Type | Average Annual Insurance Cost ($) | Annual Increase % |

House Insurance | $2,704 | 2.1% |

Car Insurance | $1,325 | 6.7% |

Contents Insurance | $823 | 0.9% |

Source: Quashed, data as at Q4 2024. Actual costs will vary depending on the insurer, policy coverage, excess levels, and individual risk factors such as age, location, and driving history.

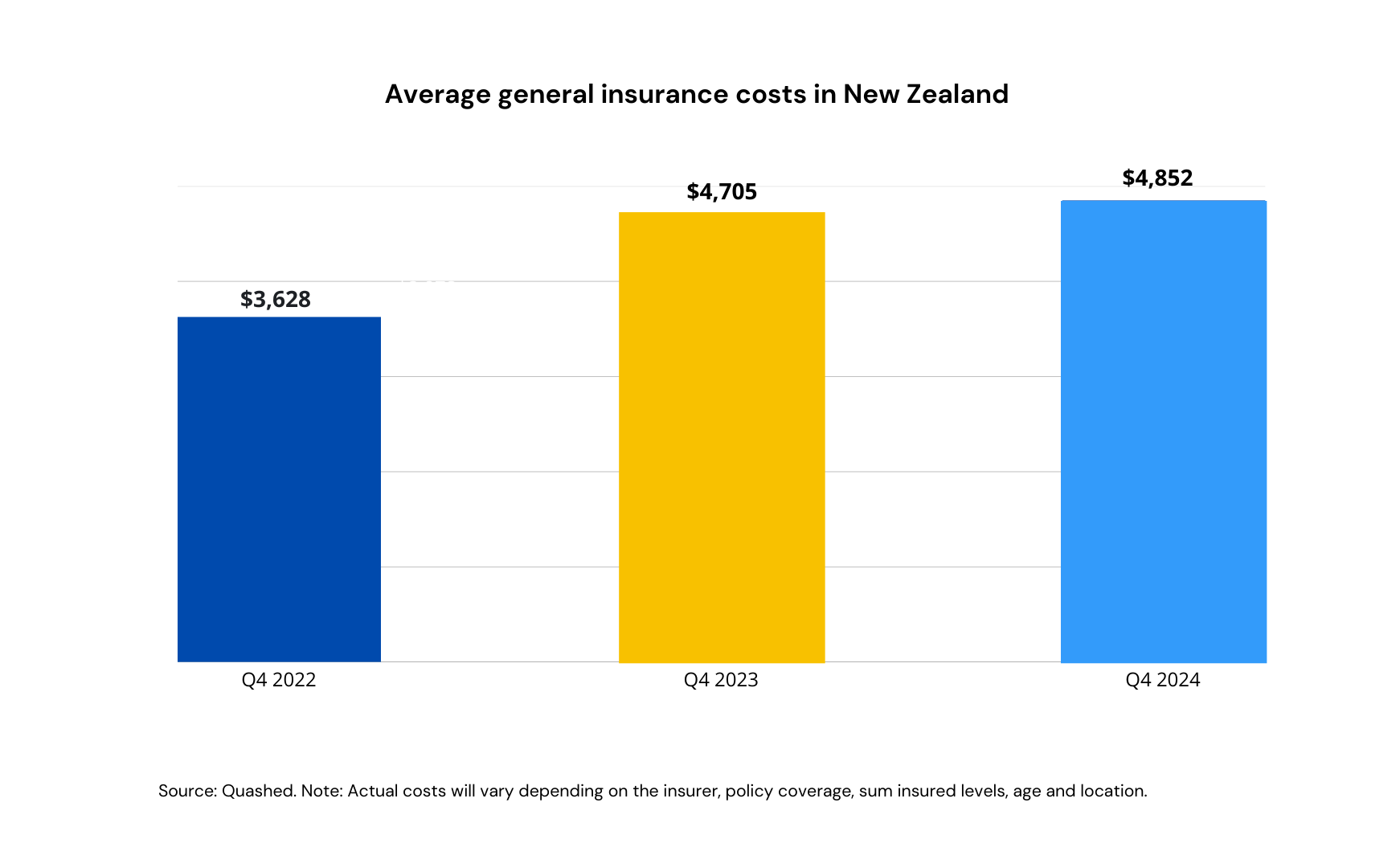

Insurance costs in New Zealand have been steadily climbing in recent years, and it’s not just your imagination. From Q4 2022 to Q4 2024, the average cost of general insurance has seen some significant jumps, as you'll see in the graph below.

Back in Q4 2022, the average cost was $3,628. By Q4 2023, that had shot up by 29.7% to $4,705. And, if you thought that was steep, the latest data from Q4 2024 shows the average cost at $4,852—an increase of another 3.1%.

Digging a little deeper, our Quashed Index shows specific types of insurance following a similar trend. House insurance now averages $2,704, which represents a 2.1% increase from last year. Car insurance is sitting at $1,325, up 6.7%, and contents insurance? It’s up 0.9%, now averaging $823.

These rising costs are a reality check for Kiwis as they try to stay on top of their insurance game. With premiums climbing and policies getting more complicated, it’s more important than ever to make sure you’re making the right choices when it comes to your insurance needs.

What affects your insurance costs in NZ?

Insurance premiums in New Zealand are influenced by several factors. Understanding these can help you make informed decisions and potentially reduce your costs.

Location: Homes in areas prone to natural disasters or higher crime rates generally have higher premiums.

Policy coverage: Comprehensive policies cost more but provide broader protection compared to basic or third-party-only options.

Home and vehicle value: Higher-value homes and cars typically cost more to insure due to their higher replacement costs.

Age and driving history: Younger drivers and those with previous claims often face higher car insurance premiums.

Excess amount:Choosing a higher excess can lower your monthly premiums, but it also means paying more out-of-pocket if you need to make a claim.

Claims history: Frequent claims can result in insurers charging higher premiums to offset the risk.

Inflation and rebuild costs: Rising construction costs, inflation, and supply chain disruptions continue to push up home insurance premiums.

How to Reduce Your Insurance Costs

If your insurance feels expensive, there are ways to manage your premiums:

Review your coverage: Ensure you are not over-insured or paying for extras you do not need.

Increase your excess: A higher excess can lower your premiums, but only if you can afford the out-of-pocket cost in the event of a claim.

Compare providers regularly: Insurers adjust their pricing frequently, so using a tool like Quashed helps you keep track of wha's happening.

Comparing insurance options gives you a clear view of where you might be overpaying. Get tailored quotes with Quashed and find a policy that suits your needs in minutes.

Why compare with Quashed?

We get it—comparing insurance the old-school way means spending hours scrolling through insurer websites, trying to make sense of confusing policies and fine print. With Quashed, you can skip the hassle and let us do the hard work for you.

Our smart, AI-powered platform analyses your current cover, compares it against the market, and highlights better options—all in one place. No more sifting through endless tabs or deciphering insurance jargon. We provide clear, side-by-side comparisons that show you what matters most, making it easy to spot the right policy without the headache.

And because we’re insurer-neutral, you can trust that our recommendations are all about you—not pushing one provider over another. Thousands of Kiwis have already saved time and money with Quashed, and you can too.

So, how does it actually work?

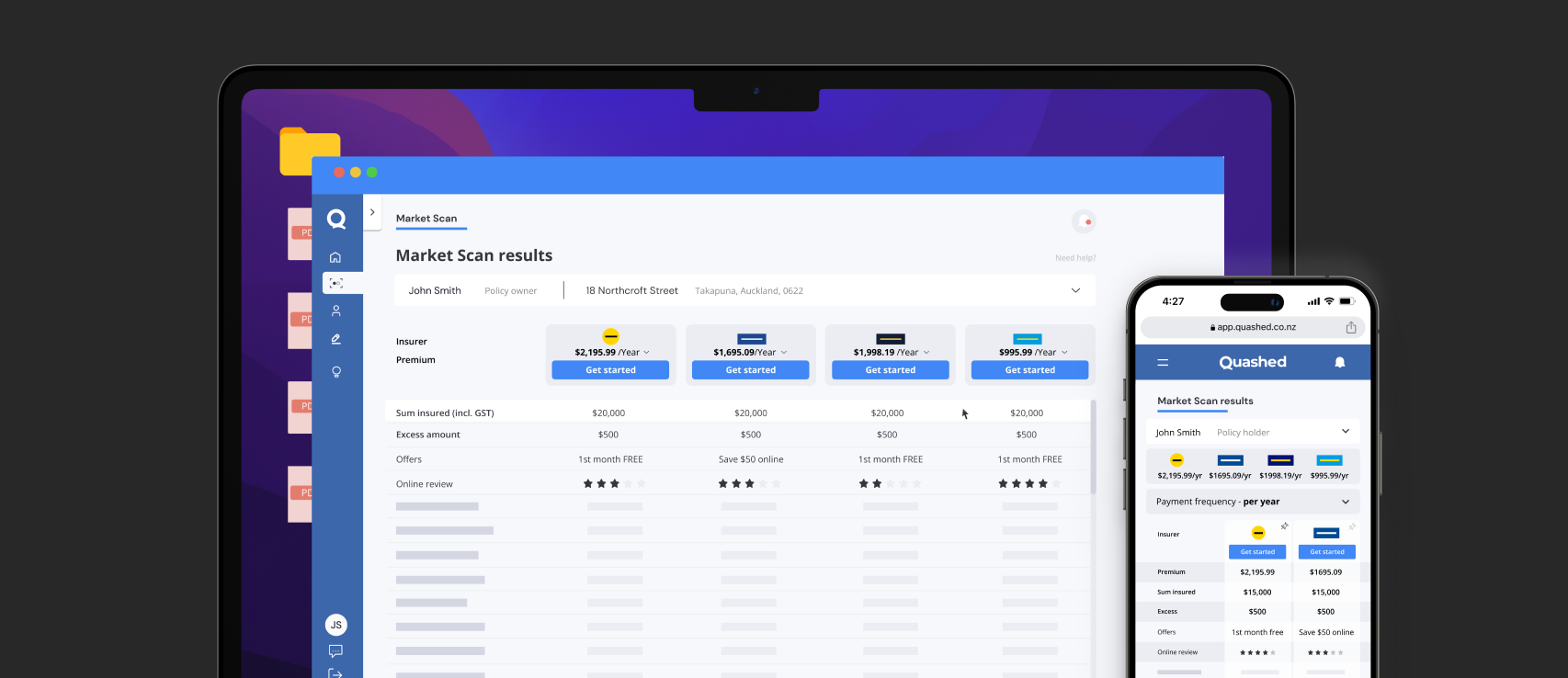

How market scan by Quashed works

Sorting your insurance has never been easier with Market Scan, our smart Kiwi tool that takes the hassle out of comparing policies.

Forget spending hours trawling insurer websites or decoding complicated fine print—simply upload your insurance docs, and we get to work. We’ll analyse your current cover and compare it against top insurers to find options that better suit your needs.

In just minutes, we’ll present you with tailored insurance options, breaking down both costs and coverage in plain English—no confusing jargon, just the facts you need to make a confident choice.

Whether you're new to insurance or know your way around policies, Market Scan makes it simple, fast, and 100% free.

Ready to compare insurance?

Take the guesswork out of comparing insurance with Market Scan.

It’s fast, free, and designed for Kiwis who want options—without the hassle.

Further reading

Here are some great reads we've selected for you:

How to Save Money on Insurance: Clever tricks to cut your insurance costs

Insurance Mistakes to Avoid: Costly blunders that could drain your wallet

Comparing Insurance Costs for Cars: Insurance cost differences across the most popular vehicles

Compare House Insurance Quotes: Smart ways to evaluate house insurance cover

Cheapest vs Best Car Insurance: Striking the perfect balance between price and protection

Car Insurance Quotes Guide: Insider tips to compare and save

Key considerations with Contents Insurance: Snagging affordable cover without cutting corners

Average Insurance Costs in NZ: A deep dive into what Kiwis really pay

Home Insurance Guide: A must-read for protecting your biggest asset

Complete Contents Insurance Guide: Everything you need to know—minus the jargon

Renewing Car Insurance Tips: A no-fuss guide to your next policy refresh

Moneyhub v Quashed: Learn more about how they compare when it comes to insurance

Tesla and Insurance: The costs of insuring a Tesla

FAQs

Cost & premiums

Why is my house insurance getting more expensive in NZ?

House insurance premiums are rising due to inflation, increasing rebuild costs, and more frequent extreme weather events. Even if you haven’t made a claim, insurers are adjusting premiums based on broader industry risks.

Key reasons for rising costs:

Building costs have increased – New Zealand construction costs have risen considerably.

More frequent and severe weather events – New Zealand experienced its wettest year on record in 2023, leading to a surge in claims

Rising reinsurance costs – Global insurance companies that back local insurers have raised their prices due to climate-related disasters. These costs are passed down to customers.

Risk reassessments by location – Some regions, previously considered lower-risk, have been reclassified due to flood mapping and climate concerns.

How can I lower my house insurance costs?

There are several ways to reduce your premiums without compromising on essential cover.

Increase your excess – A higher excess means lower premiums, but also higher out-of-pocket costs when making a claim.

Review your sum insured – Ensure your coverage reflects the true rebuild cost without over-insuring or under-insuring.

Bundle policies – Many insurers offer discounts when you combine house and contents insurance.

Pay annually instead of monthly – Some insurers charge extra for monthly payments.

Compare quotes with Quashed – Shopping around ensures you’re not overpaying. Prices can vary significantly between providers.

Coverage basics

What exactly does house insurance cover in NZ?

House insurance covers damage to your home caused by events such as fire, storms, floods, and burglary. Coverage varies by policy, but most standard policies include:

Rebuild costs if your home is damaged or destroyed.

Temporary accommodation if your home is unlivable due to an insured event.

Liability cover if someone is injured on your property.

Natural disaster protection in partnership with NHC for earthquakes, landslides, and tsunamis.

Getting the right cover

How do I know if I’m insuring my house for the right amount?

Your sum insured should reflect the cost of fully rebuilding your home. If it’s set too low, you may have to cover the shortfall in a claim. How to get it right:

Use a rebuild cost calculator like Cordell Sum Sure to get an accurate estimate.

Account for extra costs such as demolition, debris removal, and council fees.

Update your sum insured if you renovate or extend your home.

Check insurer policies—some offer full replacement options.

What should I check when comparing insurance policies?

Key factors to compare:

Sum insured – Does the policy fully cover rebuild costs?

Excess options – A higher excess lowers premiums but increases claim costs.

Policy exclusions – Check what’s not covered, such as gradual wear and tear.

Claims process – Consider customer reviews and insurer reputation.

Additional cover options – Some policies include extras like alternative accommodation and gradual damage protection.

Claims & problems

What’s the first thing I should do when making a claim?

Take immediate action to document the damage and notify your insurer.

Claims process:

Photograph and video the damage for evidence.

Contact your insurer as soon as possible to start the claim.

Prevent further damage if safe to do so, such as covering broken windows.

Keep receipts for emergency repairs or replacements.

Follow your insurer’s process to avoid claim delays.

What happens if I’m underinsured?

Underinsurance occurs when your sum insured isn’t enough to cover the full cost of rebuilding your home. If this happens, you may have to contribute to the shortfall.

Consequences of underinsurance:

You may need to cover part of the rebuild cost yourself.

Some insurers apply proportionate payouts, meaning they reduce what they pay based on how underinsured you are.

Your mortgage lender may require higher coverage before approving a home loan.

Special situations

Do I need different insurance for a rental property?

Yes—standard house insurance does not cover rental-related risks. Landlord insurance provides additional protection.

Key differences in landlord insurance:

Loss of rent cover if tenants stop paying or the property becomes unlivable.

Tenant damage cover for accidental or intentional damage.

Liability protection if a tenant or visitor is injured on the property.

Meth contamination cover in some policies for decontamination costs.

How does house insurance work for apartments or units?

Apartment owners need to consider both body corporate insurance and private insurance.

What you need to check:

Body corporate insurance covers the building structure and shared areas.

Your private insurance covers fixtures, fittings, and personal liability.

Unit damage responsibilities vary by policy—check what’s covered

This article provides general information only and does not constitute insurance or financial advice. Insurance policies vary between providers, and you should check with your insurer or a licensed adviser for guidance specific to your situation. For full details, refer to Quashed’s terms and conditions.