Car Insurance for Young Kiwis: Expensive As?

You're young. You've got your wheels. And suddenly, people are talking about premiums, excesses, and insurance policies that might as well be written in a foreign language.

Sound familiar? The truth is, car insurance for the under-25s in New Zealand comes with challenges. It’s not only “confusing as,” but it’s also “expensive as.”

This guide ditches the jargon and gets down to business. We'll break down everything you need to know about young driver insurance, from understanding the basics to finding ways to keep those premiums from burning a hole in your pocket.

How much does car insurance cost for young Kiwis?

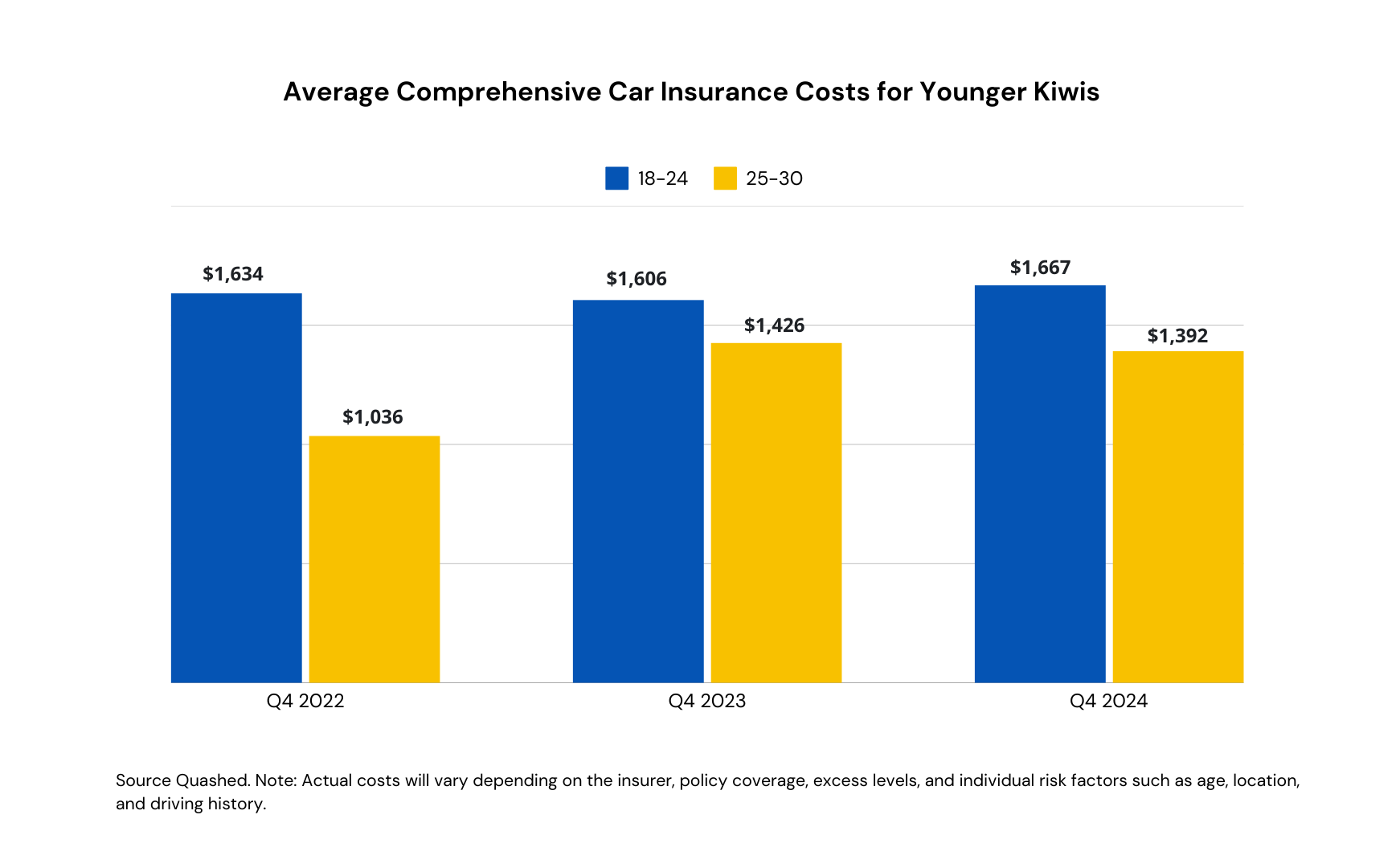

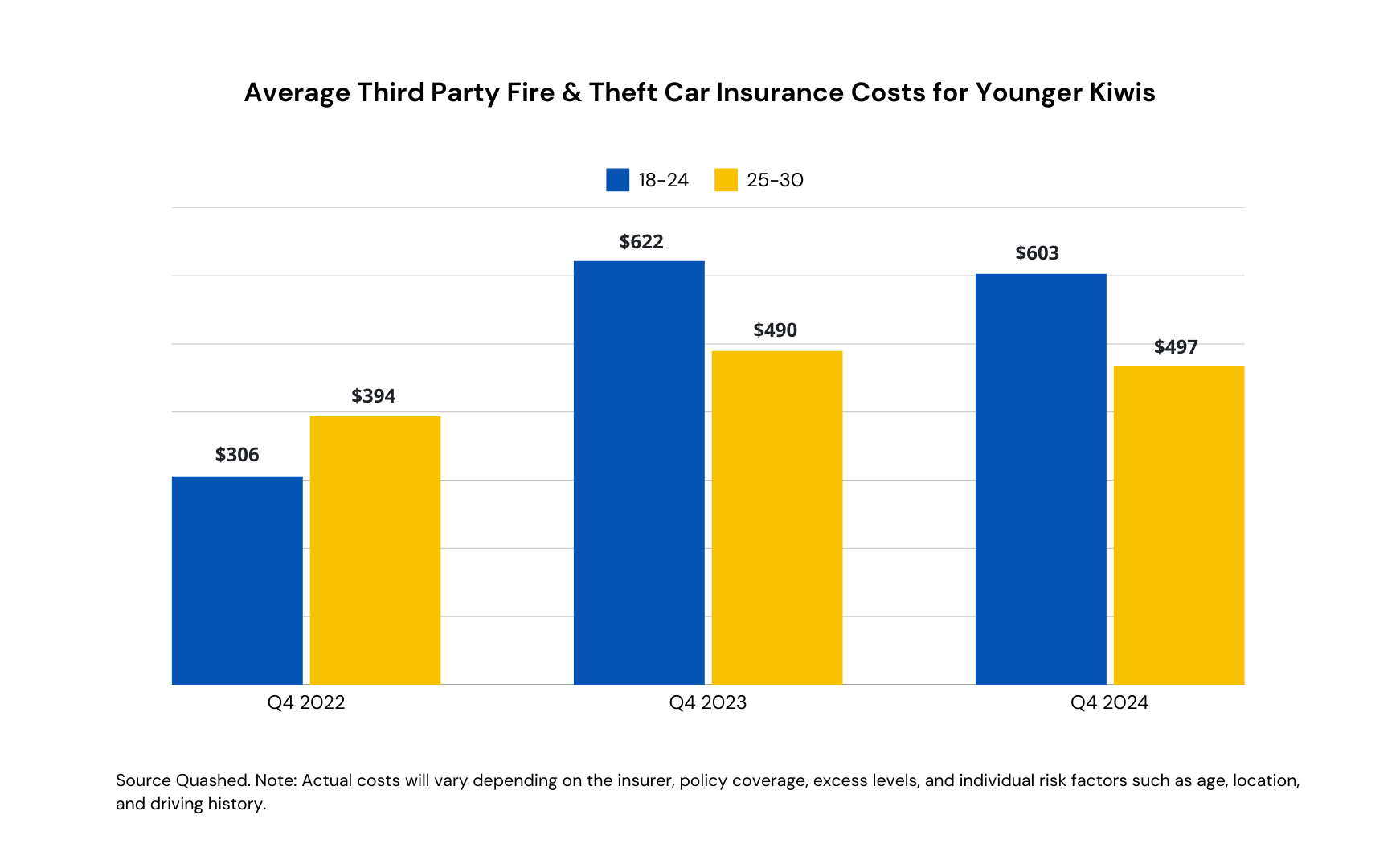

Car insurance isn’t cheap—especially for younger drivers. According to the Quashed Index, the average Kiwi pays $1,325 for comprehensive cover and $476 for third-party fire and theft insurance. But younger drivers are hit with even steeper costs. So, what’s the damage for young Kiwis? Check out the numbers below:

Average Comprehensive Car Insurance Cost $

Year | 18-24 | 25-30 |

|---|---|---|

Q4 2022 | $1,634 | $1,036 |

Q4 2023 | $1,606 | $1,426 |

Q4 2024 | $1,667 | $1,392 |

2 year change % | 2% | 34% |

Third Party Fire & Theft Car Insurance Cost $

Year | 18-24 | 25-30 |

|---|---|---|

Q4 2022 | $306 | $394 |

Q4 2023 | $622 | $490 |

Q4 2024 | $603 | $467 |

2 year change % | 97% | 19% |

Source Quashed. Note: Actual costs will vary depending on the insurer, policy coverage, excess levels, and individual risk factors such as age, location, and driving history. Check out the charts for a quick visual breakdown.

Source: Quashed

Why do younger drivers pay more for car insurance?

Insurance companies consider drivers under 25 a higher risk, and the data backs this up. According to ACC, young drivers aged 16-24 are overrepresented in serious road injuries and fatalities in New Zealand.

16-24-year-olds make up just 13% of licence holders but account for 30% of serious road injuries and over 25% of fatalities.

The first six months of having a restricted licence is the riskiest period for young drivers.

Lack of experience means higher accident rates, more claims, and steeper insurance premiums.

Because younger drivers are statistically more likely to claim, insurers charge higher premiums to balance the risk

Looking for ways to reduce your premiums?

Let’s break down your two main options:

Comprehensive car insurance (higher protection, higher cost)

Third-party fire and theft insurance (cheaper but with less coverage)

Choosing the right cover: Comprehensive versus Third-party Fire and Theft Insurance

Now that we’ve covered the costs, let’s break down the different types of car insurance.

Comprehensive car insurance: Think of this as the "essentials" package. It covers damage to your car—whether it’s an accident, theft, or even fire—as well as any damage you cause to other vehicles. If you're looking for comprehensive car insurance for under 25 drivers, this type of cover offers the most protection even fire), as well as any damage you cause to other vehicles.

Third-party, fire and theft insurance: This is more like the "basics" package. It covers damage you cause to other people's cars or property, plus protection if your car is stolen or damaged by fire. However, it won’t cover repairs to your own vehicle if you're at fault. It's a popular option for those looking for affordable car insurance for young drivers, especially when driving an older car.

What are the pros and cons here? Comprehensive car insurance – "The essentials"

Pros:

Covers your car and others—you're sorted no matter who's at fault.

Great for newer or expensive cars.

Often includes handy extras like roadside assistance.

Cons:

Higher premiums, making it pricier for car insurance for under 25 drivers.

Might not be worth it for an older car.

Third-party, fire & theft – "The basics"

Pros:

Cheaper and easier on your budget—ideal for those seeking cheap car insurance for young drivers.

Covers damage to others' cars and protects against fire and theft.

A good option if your car isn’t worth much.

Cons:

Doesn’t cover damage to your car if you crash.

You'll need to pay for your own repairs.

Fewer extras like roadside assistance.

Alright, so you've got a good idea of the different types of cover—but there’s one more thing you need to think about: your excess. It’s the amount you have to pay if something goes wrong and you need to make a claim. Getting it right can make a big difference in what you pay upfront and down the line. Let’s break it down.

What is an excess? And what’s the deal with it?

Your excess is the amount you have to pay if you make a claim. Picking the right excess can seriously affect what you fork out upfront and when things go wrong:

Lower excess = Higher premium: You’ll pay more now, but less if you need to claim.

Higher excess = Lower premium: You’ll save on premiums but will need to cough up more if you have an accident.

Tip: Quashed lets you adjust your excess for both comprehensive car insurance for young drivers and third-party policies, so you can see how it impacts your premium in real time.

Keen to cut those premiums? The good news is, there are ways to save without skimping on cover.

Practical ways to lower car insurance costs

Looking to save on your car insurance as an under-25 driver? Here are a few practical tips:

Drive a car that�’s cheaper to insure: Smaller, lower-powered cars usually mean lower premiums.

Switch policy types: Consider changing to Fire, Theft and Third Party.

Up your excess: Choosing a higher excess can shrink your premium.

Bundle up: If your family has multiple policies, bundling could score you a discount.

Stay safe: A clean driving record can help bring your costs down over time.

Compare with Quashed: Analyse your options without the hassle of searching all over the place.

Example: Savings from switching policies

If you're wondering how much you could save by changing your insurance type, here’s a hypothetical example:

Vehicle: Toyota Corolla

Sum insured: $3,000

Excess: $500

Profile: 24-year-old male in Auckland

Yearly Average Car Insurance Cost $ | |

|---|---|

Comprehensive Car Insurance | $947 |

Fire, Theft and Third Party | $549 |

Saving from switching | $398 |

Source Quashed. Note: Actual costs will vary depending on the insurer, policy coverage, excess levels, and individual risk factors such as age, location, and driving history.

In this example, switching from comprehensive to fire, theft, and third-party insurance saves $398 a year—nice, right? But before you make the switch, think about what cover actually works for you. Saving money is great, but you still want to be sorted if something goes wrong.

Why use Quashed to compare car insurance?

We make it easy to see your options all in one place, so you don’t have to spend hours hopping between websites or calling insurers. With Quashed, you can:

Compare side by side: See what different insurers are offering at a glance—no more guesswork.

Find a deal that fits your vibe: Whether you want the cheapest option or the best coverage, Quashed helps you analyse what's for you.

No confusing jargon: We break down the details so you actually know what you're signing up for.

Save time: With just a few clicks, you can sort out your insurance without the hassle.

Car insurance that makes sense

Over 45,000 Kiwis have joined Quashed—are you next?

Compare car insurance for under 25s with real-time quotes and side-by-side comparisons.

Sign up now and start comparing in minutes—save time and hassle today!!

Further reading

Smart Ways to Slash Your Car Insurance: Useful tips to reduce your car insurance costs.

Why Is Car Insurance So Expensive?: Find out why premiums are rising.

Key Factors in Choosing Insurance: What to consider when picking a policy.

Cheapest Versus Best Car Insurance in NZ: Cheapest vs best insurance options.

Car Insurance Quotes: How to compare quotes easily.

Debunking Car Insurance Myths: Common car insurance myths busted.

Sorting Out Your Car Insurance Renewal: Tips for renewing your car insurance.

Car Insurance for Aucklanders: Insurance tips for Auckland drivers.

FAQs

Ways to save on car insurance

How can I lower my car insurance costs?

You can lower your car insurance costs by:

Comparing quotes from different insurers—prices vary significantly.

Increasing your excess to reduce your premium.

Bundling policies (e.g., car and contents insurance) to unlock discounts.

Checking that your sum insured matches your car's current market value.

Does loyalty to my current insurer pay off?

Not always. Many insurers offer better rates to new customers than existing ones. To get the best deal:

Compare premiums annually to check for better options.

Call your insurer and negotiate—mentioning competitor rates can help.

Look for multi-policy or long-term customer discounts.

Is it cheaper to be a named driver on my parents' policy?

Yes, in some cases, being added to a parent's policy can reduce costs. However:

Some insurers restrict this to young drivers who only occasionally use the car.

Listing the actual main driver incorrectly could cause claim issues.

It’s best to check with the insurer to avoid complications.

Is it worth switching to a new insurer?

It can be. Some insurers offer lower rates, better claims service, or additional perks. To decide:

Compare policies side by side (not just the price—look at excess and coverage).

Read customer reviews about claims processing and service.

Check for sign-up discounts, but ensure they’re worth it long-term.

Choosing insurance

Should I go for third-party insurance instead of comprehensive?

Third-party insurance is cheaper, but it has fewer protections:

Covers damage to other vehicles if you cause an accident.

Third-party, fire & theft adds cover for theft and fire damage.

Does not cover damage to your own car if you're at fault.

You could be out of pocket if hit by an uninsured driver.

What’s the easiest way to compare car insurance policies?

The fastest way to compare is by:

Using insurer websites for quick quotes.

Checking comparison tools to see price and policy features side by side.

Looking beyond just price—check excess levels, claim processes, and perks like roadside assistance.

Factors that affect your premium

Why is my excess so high as a young driver?

Young drivers typically face higher excesses because they’re considered higher risk.

Will modifying my car increase my insurance costs?

Yes, most modifications increase premiums because they:

Raise the risk of theft (e.g., custom wheels, body kits).

Increase accident risk (e.g., lowered suspension, turbo kits).

Affect repairs —custom parts cost more to replace.

Some insurers may decline cover for modified cars, so check before making changes.

Does my location affect my insurance costs?

Yes, where you live impacts your premium:

Higher costs: Cities with high accident or theft rates (e.g., Auckland).

Lower costs: Smaller towns or areas with fewer claims.

Parking your car in a locked garage instead of on the street can reduce costs.

Claims & coverage

What happens if I make a claim that wasn’t my fault?

If another driver is at fault, your no-claims bonus may be protected, but:

You may still need to pay the excess upfront and get it reimbursed later.

If the other driver is uninsured, your claim might be handled as an at-fault claim, affecting your premium.

Some policies offer uninsured driver cover, so check your policy details.

What should I do if my car is stolen or written off?

If your car is stolen or a total loss:

Report the theft to police and get a case number.

Notify your insurer and provide all required documents.

If insured for market value, expect a payout based on your car’s current worth.

If insured for agreed value, you’ll get the pre-set amount stated in your policy.

This article provides general information only and does not constitute insurance or financial advice. Insurance policies vary between providers, and you should check with your insurer or a licensed adviser for guidance specific to your situation. For full details, refer to Quashed’s terms and conditions.