NZ Landlord Guide 2026: Navigating Vacant Property Insurance & The "60-Day" Rule

By Alan Hardy @ Quashed.co.nz

Moving into 2026, many New Zealand property owners are discovering that the greatest risk to their investment isn't a difficult tenant, but an empty house. Whether you are between tenancies, marketing a property for sale, or undergoing renovations, a vacant home triggers specific "unoccupied" clauses that can severely restrict your coverage.

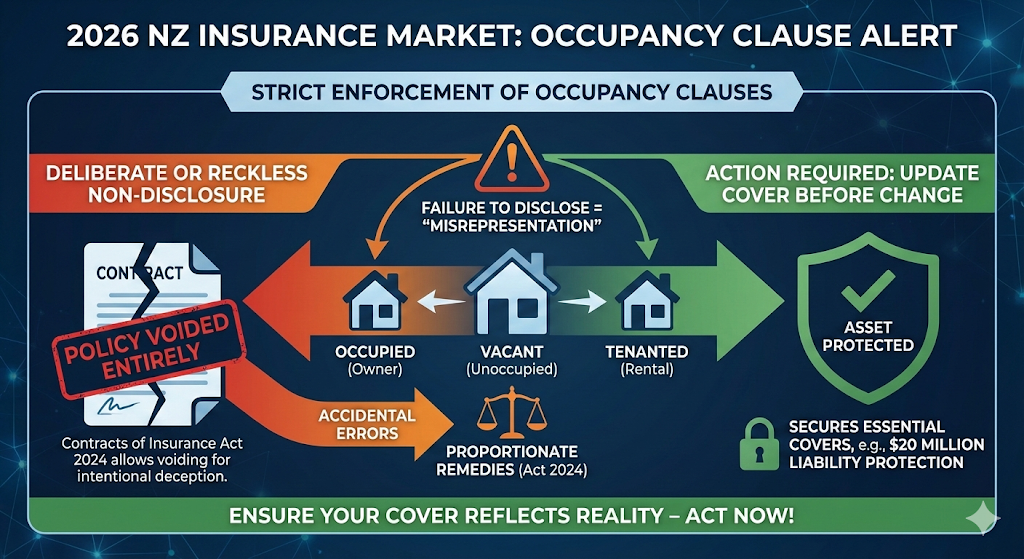

At Quashed, we see that most major NZ insurers apply strict penalties once a home has been vacant for a set period—typically 60 to 90 days. Under the Contracts of Insurance Act 2024, failing to disclose that your property is vacant is a "misrepresentation" of the risk. While the law now requires insurers to provide proportionate remedies for innocent mistakes, a "deliberate or reckless" failure to update your property status can still lead an insurer to void your policy entirely and decline your claim.

Step 1: Understanding the Unoccupied Home Penalty

The Issue

Landlord insurance contracts are built on the specific premise of the home being managed and occupied. When a property sits empty, the risk of undetected issues—such as gradual water damage, vandalism, or fire—increases significantly. Most Kiwi insurers will automatically reduce your cover to "Limited Cover" (often restricted to Fire and Explosion) or increase your excess once the vacancy limit is reached.

The Data

As shown in the Quashed Market Scan, the "vacancy clock" and the resulting penalties differ significantly between providers:

Insurer | Vacancy Limit (Days) | Typical Penalty After Limit Exceeded |

AMP | 60 Days | Additional excess often applies |

Initio | 60 Days | Additional excess often applies |

Tower | 90 Days | Limited cover and additional excess apply |

Trade Me | 90 Days | Limited cover and additional excess apply |

The Lesson

Do not assume you have "Full Replacement" cover if your property is empty for a long period. If you are planning a renovation or the property will be empty for more than 60 days, you must contact your insurer to request a formal vacant property extension. Insurers typically do not negotiate these terms at the time of a claim; you must seek written approval for the extension beforehand to ensure your asset remains protected.

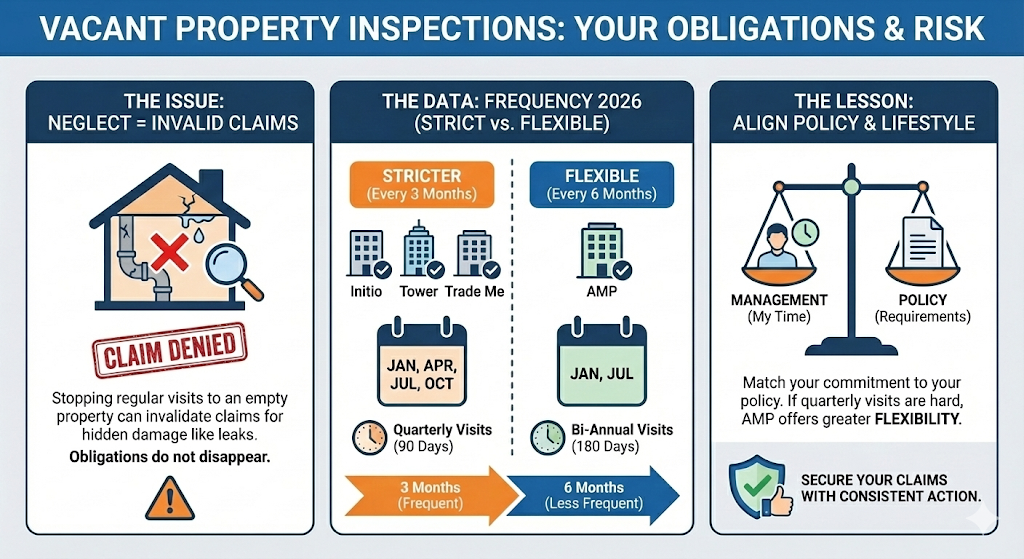

Step 2: The Mandatory Inspection Gap

The Issue

Even if your property is vacant, your inspection obligations do not disappear. Many owners make the mistake of stopping regular visits while a house is empty, which can invalidate claims for issues like hidden water leaks. In 2026, "Gradual Damage" (hidden leaks over time) remains a common cause of declined claims for vacant properties. If a pipe leaks behind a wall while a house is empty, it can cause tens of thousands in damage before it’s discovered.

The Data

In 2026, the frequency of required inspections remains a critical condition of maintaining valid cover:

Insurer | Required Inspection Frequency |

AMP | Every 6 Months |

Initio | Every 3 Months |

Tower | Every 3 Months |

Trade Me | Every 3 Months |

The Lesson

Quashed data shows that if you cannot visit a property every 90 days, you should prioritise an insurer like AMP that offers a 6-month window. Use the Quashed Market Scan to see if the price trade-off for this flexibility is worth it for your portfolio.

Step 3: Comparing the Cost of Protection

The Issue

The insurer that offered the best deal when your house was a rental may not be when it is under repair or a vacant investment. Staying with a provider that is no longer fit for your property's current status can lead to significant overpayment for reduced protection.

The Data

For a $1.3M property in Auckland, the price variance for landlord cover is substantial:

Policy Feature | Initio | Trade Me | AMP | Tower |

Annual Premium | $3,278.44 | $4,669.78 | $2,296.41 | $4,219.50 |

Standard Excess | $1,150 | $1,000 | $1,000 | $1,000 |

Financial Strength | AA (Very Strong) | A- (Strong) | AA- (Very Strong) | A- (Strong) |

The Lesson

The difference between the lowest and highest premium for the same home can exceed $2,300 per year. By using the Quashed Market Scan, you can identify which providers offer the best value for your property's specific occupancy status, ensuring you aren't paying a premium for cover that may be legally challenged during the claims process.

Final Verdict: Don't Gamble on a Void Policy

In the 2026 NZ market, insurers are strictly enforcing occupancy clauses. If you fail to disclose that a property is vacant or tenanted, it is considered a “misrepresentation”. While the Contracts of Insurance Act 2024 requires insurers to provide proportionate remedies for accidental errors, they can still void a policy entirely if a homeowner "deliberately or recklessly" fails to disclose a change in occupancy. To ensure your asset is actually protected—and to secure essential covers like $20 million in liability protection—you must update your cover before the property status changes.

Don't pay a "Loyalty Tax" for reduced protection on your empty property. Our data shows that for the same property, the price difference between insurers can exceed $2,300 per year.

Compare Real-Time Vacant Property Quotes Now with Quashed Market Scan

Related Reading

If you're managing a rental property or navigating a period of vacancy in 2026, staying informed about the evolving insurance landscape is crucial to protecting your investment. Explore these essential guides to ensure you have the right coverage and are meeting all your policy obligations:

Landlord Insurance: The Ins and Outs of Insuring Your Rental – A comprehensive deep-dive into the essential covers every property investor needs to protect their portfolio and mitigate risks in the 2026 market.

Tower Insurance 2026: Quashed Ultimate Kiwi Review – Explore the latest policy updates, vacancy limits, and coverage restrictions from one of New Zealand's largest insurers to see if they fit your current property status.

Is Initio Insurance Right for Kiwis? 2025 Review & Verdict by Quashed – Get an expert breakdown of Initio’s online-first insurance model and whether their specific inspection and vacancy terms offer the best value for your investment.

AMP Insurance NZ Review (2025): What You Need to Know – Understand the "Everyday" vs "Everyday Plus" tiers and how their 6-month inspection requirement compares to other major Kiwi providers.

Getting the Best Deal? Read this Contents Insurance Comparison Guide by Quashed (2025) – Learn how "Gradual Damage" extensions and sum-insured calculations change when a property is no longer owner-occupied.

Your Top House Insurance Questions Answered – Discover how renovations and safety features like smoke alarms impact your premiums and what happens to your cover when you go on holiday for more than 60 days.

FAQs

Does my insurance cover renovations? Most standard policies restrict cover if the home is unoccupied during major renovations. You must notify your insurer to ensure you are covered for the duration of the works and check if a "Construction" or "Alterations" add-on is required to protect against risks specific to building sites.

What happens if I forget to tell my insurer the house is empty? In 2026, this is a breach of your duty to take reasonable care not to make a misrepresentation. If the insurer would not have covered a vacant property under your current terms, they may reduce your payout proportionately. In cases deemed "deliberate or reckless," they may void the policy and decline the claim entirely.

Is specialised landlord insurance tax-deductible? Yes. Unlike standard homeowner insurance for your primary residence, premiums for a rental property are considered a business expense. In New Zealand, these costs are generally tax-deductible, helping to offset the cost of higher-tier protection.

What counts as an "inspection" for a vacant property? An inspection typically requires a physical visit to the property to check for issues like leaks, break-ins, or damage. In 2026, frequency requirements vary: AMP requires this every 6 months, while others like Tower and Initio require it every 3 months. Failing to document these visits can lead to a declined claim for gradual damage.

Can I get full cover for a house that is empty for more than 90 days? Standard policies usually drop to "Limited Cover" (Fire and Explosion only) after the 60 or 90-day limit. To maintain full replacement cover, you must request a formal vacant property extension and receive written approval from your insurer.

Can I get a discount for a vacant property since no one is using the utilities? Actually, the opposite is true. Because vacant homes are statistically more likely to suffer from undetected leaks or break-ins, premiums are often higher or come with significantly higher excesses. Using the Quashed Market Scan is the best way to see which insurers, like AMP, offer more competitive rates for vacant profiles.