Renting Your Old House in 2026? The Quashed NZ Guide to Why Standard House Insurance Fails

If you are moving into a new home and planning to rent out your former residence, your first priority must be your insurance policy. In New Zealand, a standard house insurance policy is designed solely for owner-occupiers. The moment you move out and a tenant moves in, that policy is no longer fit for purpose.

At Quashed, we strongly advise homeowners to notify their insurer and update their policy to Landlord coverage to avoid potentially breaching their obligation to “take reasonable care not to make a misrepresentation”. In 2026, insurers are strictly enforcing "occupancy clauses." If you are still paying for standard house insurance on a tenanted property, you are likely paying for cover that will be legally voided the moment you try to make a claim.

To see the price difference for your specific property, use the Quashed Market Scan to compare real-time landlord insurance quotes across New Zealand’s leading providers.

Step 1: The Critical Switch from Standard House to Landlord Insurance

The Issue

Standard house insurance is a contract based on the owner living on-site. When you rent the property out, the risk profile changes significantly. From an insurer's perspective, a tenant introduces risks that a homeowner does not—such as liability for tenant injuries or intentional damage. If you do not disclose and formally switch to a Landlord Policy, you have failed your responsibility to "take reasonable care not to make a misrepresentation."

The Data

Under the Fair Insurance Code, "material non-disclosure" allows an insurer to treat a policy as if it never existed. In the 2026 market, where premiums have risen across NZ, insurers are highly incentivised to verify occupancy during the claims process. If they find a tenant in a house covered by standard house insurance, they can void the payout for fire, flood, or even total loss.

The Lesson

Standard house insurance is for homes; Landlord Insurance is for investments. You must contact your provider or use Quashed to transition your cover before the first tenancy agreement begins. This switch is the only way to ensure your asset is actually protected.

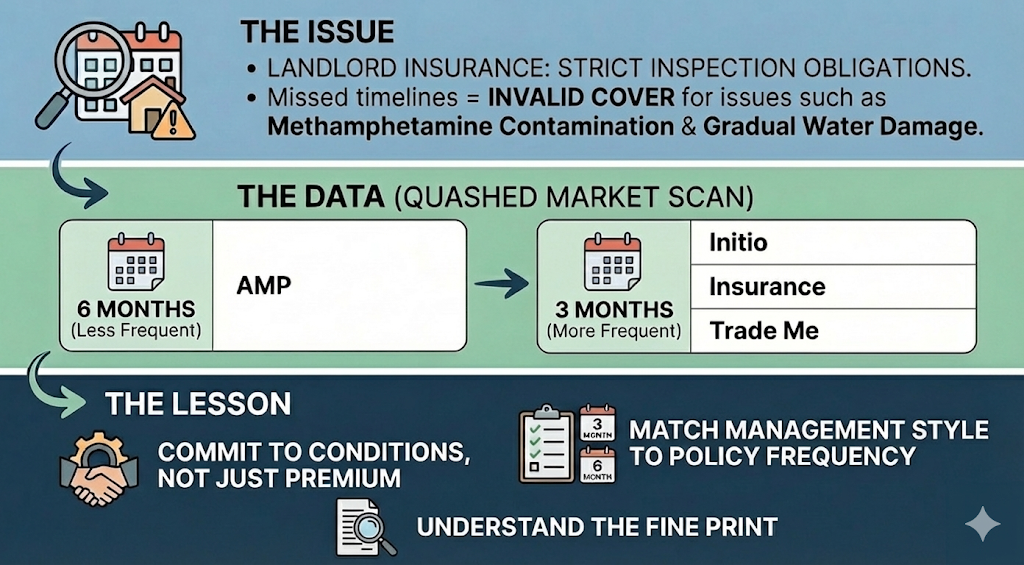

Step 2: Landlord-Specific Obligations (The Inspection Gap)

The Issue

Landlord Insurance policies come with strict "Inspection Obligations." If you fail to meet these specific timeframes, your cover for things like methamphetamine contamination or gradual water damage may become invalid.

The Data

As shown in the Quashed Market Scan, the requirements for landlords in 2026 can vary by insurance provider:

AMP | Initio | Tower Insurance | Trade Me | |

Mandatory Inspection Frequency | Every 6 months | Every 3 months | Every 3 months | Every 3 months |

The Lesson

Switching to Landlord Insurance isn't just about paying the premium; it’s about meeting the conditions. If you cannot commit to 3-monthly inspections, a policy from AMP may be the most suitable for you. Ensure your management style matches your policy fine print.

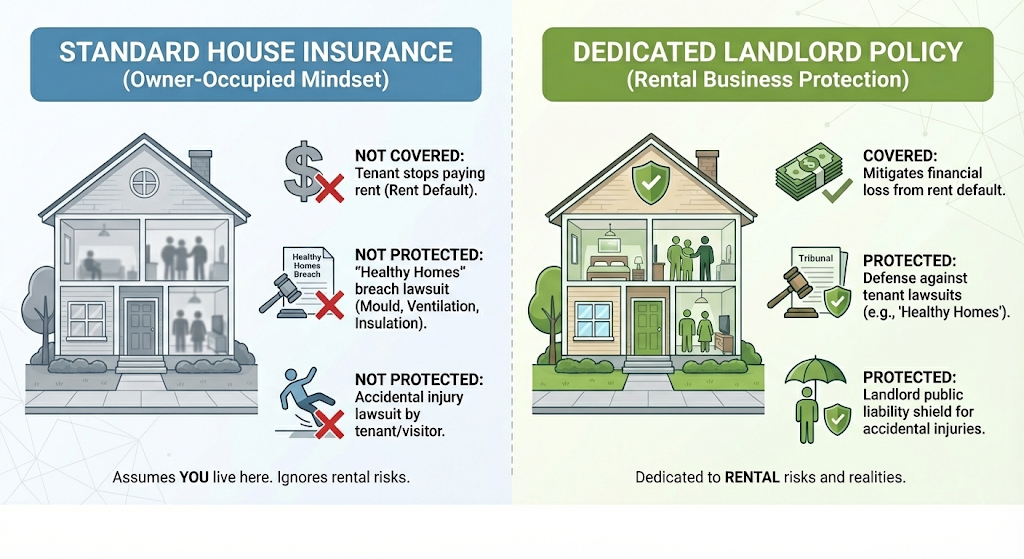

Step 3: Covering the "Landlord-Only" Blind Spots

The Issue

Standard house insurance is blind to the financial realities of renting. It will not pay you if a tenant stops paying rent, nor will it protect you if a tenant sues you for an accidental injury.

Crucially, it leaves you exposed to the modern legal landscape. As of 1 July 2025, all private rentals must comply with Healthy Homes standards. In 2026, the Tenancy Tribunal is no longer just issuing warnings—it is awarding exemplary damages of up to $7,200 for non-compliance. These are high-stakes risks that only a dedicated Landlord Policy can mitigate, turning a potential "sticker shock" penalty into a manageable, insured risk.

The Data

Data from Quashed illustrates the massive gap in protection levels between Landlord Insurance providers for an Auckland-based rental:

Benefit | AMP | Initio | Tower | Trade Me |

Loss of rent - insured loss | Option (up to 12 months) | Covered (up to 52 weeks) | Covered (up to 8 months) | Covered (up to 8 months) |

Loss of rent - failure of public utilities / access prevention | Option (up to 12 months) | Covered (up to 6 weeks) | Covered (up to 8 weeks) | Covered (up to 8 weeks) |

Loss of rent - lawful eviction non payment | Option (up to 12 months) | Covered (up to 6 weeks) | Covered (up to 8 weeks) | Covered (up to 8 weeks) |

Loss of rent - tenant vacating without required notice | Option (up to 12 months) | Covered (up to 6 weeks) | Covered (up to 8 weeks) | Covered (up to 8 weeks) |

Liability cover - property damages / bodily injury | $1 million | $2 million | $20 million | $20 million |

The Lesson

Standard house insurance leaves you exposed to these costs. By switching to a Landlord Policy, you can secure up to $20 million in liability protection or a full year of replacement rent. This protection is the foundation of a safe investment.

Step 4: Compare Prices and Coverage Across NZ Providers

The Issue

The biggest mistake homeowners make when renting their "old nest" is assuming their current provider is the best for a landlord policy. Price volatility in the 2026 NZ market means the most competitive home insurer may be the most expensive for landlords.

The Data

Comparing quotes for a $1.3M home in Auckland reveals a massive variance. Some providers focus on lower prices, while others charge a premium. These price differences are for the exact same risk profile and home:

Policy Feature | AMP | Initio | Tower Insurance | Trade Me |

Annual Premium | $2,296.41 | $3,278.44 | $4,219.50 | $4,669.78 |

Standard Excess | $1,000 | $1,150 | $1,000 | $1,000 |

Financial Strength | AA- (Very Strong) | AA (Very Strong) | A- (Strong) | A- (Strong) |

The Lesson

In 2026, there is a significant gap between the cheapest and most expensive landlord policy for the same home. If you renew with your current "standard" provider, you are likely paying a massive "Loyalty Tax."

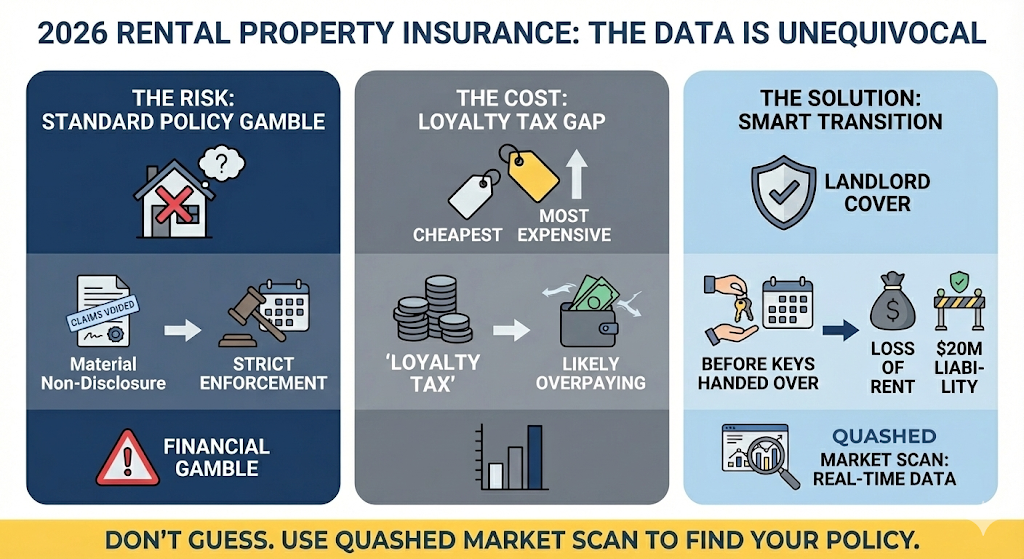

Final Verdict: Don't Pay the "Loyalty Tax" on a Void Policy

In 2026, the data is unequivocal: holding onto a standard house insurance policy for a rental property is a financial gamble you cannot win. Not only do you risk having your claims voided for "material non-disclosure" if a tenant causes damage, but you are also likely overpaying for the privilege.

Our data reveals a significant gap between the cheapest and most expensive landlord policies for the exact same risk profile. If you simply renew with your current provider, you are likely paying a massive "Loyalty Tax".

The market has shifted. Insurers are strictly enforcing occupancy clauses and inspection obligations. To ensure your asset is actually protected—and to secure essential covers like Loss of Rent and $20 million in liability protection—you must transition your cover before the keys are handed over.

Do not guess. Use the Quashed Market Scan to see real-time data and find the policy that matches your property and your budget.

Related Reading

Looking for more ways to protect your property and finances? Explore our expert reviews and guides below to navigate the nuances of the New Zealand insurance market with confidence:

MAS Insurance 2026 Reviewed — The Quashed Kiwi Breakdown: A comprehensive look at the mutual-owned model and how their "Area Replacement" policies differ from the standard sum-insured approach.

Is Initio Insurance Right for Kiwis? 2025 Review & Verdict by Quashed: We investigate Hamilton-based Initio's online-only platform, focusing on their specialised landlord protections like deliberate damage and meth cover.

Tower Insurance 2026: Quashed Ultimate Kiwi Review: An expert breakdown of Tower's simplified coverage levels and the mechanics of their transparent excess system for property owners.

Getting the Best Deal? Read this Contents Insurance Comparison Guide by Quashed (2025): Learn to navigate the fine print of contents policies, including hidden limits on high-value items and critical gradual damage extensions.

Ultimate NZ Guide to Contents Insurance (2025): Compare & Find the Best and Cheapest Cover - Quashed: Discover how regional location impacts your premium and the non-negotiable difference between Replacement Value and Indemnity Value.

Landlord Insurance: The Ins and Outs of Insuring Your Rental - Quashed: Our definitive guide to the unique risks of renting, covering everything from legal liability to intentional damage by tenants.

FAQs

Can I just add an "extension" to my standard house insurance? Some insurers allow a landlord extension, but it often lacks the comprehensive liability and loss-of-rent features of a standalone Landlord Policy. Always check if the base policy is still valid for a non-resident owner.

Is Landlord Insurance more expensive than standard house insurance? Generally, yes, because the risks are higher, however, it is a tax-deductible expense in NZ.

When exactly do I need to switch from my standard policy to a Landlord Policy? You must transition your cover before the first tenancy agreement begins. The moment you move out and a tenant moves in, your standard house insurance policy is no longer fit for purpose. To ensure your asset is protected and to avoid coverage gaps, this switch must happen before the keys are handed over.

I like my current insurer. Can’t I just renew with them when I become a landlord? Simply renewing with your current provider is often a financial mistake known as paying a "Loyalty Tax". The insurer that was cheapest for your owner-occupied home may be the most expensive for a landlord policy. Data shows a significant price gap between providers for the exact same risk profile, so it is crucial to compare quotes rather than assuming your current provider is the best fit.

Will my insurance really be voided just because I didn't tell the insurer I moved out? Yes. In 2026, insurers are strictly enforcing "occupancy clauses". If you fail to disclose that a tenant is living in the property, this is considered "material non-disclosure," which allows the insurer to treat the policy as if it never existed.