The End of Multi-Policy Discounts in NZ? Why You Must Shop Around in 2026

The "golden rule" of Kiwi insurance is dead. For decades, we’ve been told to bundle and save—keeping our house, car, and contents with one provider like State or AMI to unlock a loyalty discount.

In 2026, that loyalty is costing you money.

Major insurers are quietly removing Multi-Policy Discounts (MPD) and replacing them with risk-based pricing. This means your loyalty discount is likely vanishing, while your premiums rise. Our latest data at Quashed reveals a "Loyalty Tax" where thousands of Kiwis are overpaying for bundles that no longer exist.

At Quashed, we believe you should pay for cover, not empty promises. This guide explains why the bundle is vanishing and how breaking up your policies could be the smartest financial move you make this year.

Start below by reviewing the changes, then run a free Quashed Market Scan to see if your "bundle" is actually costing you more.

Before We Get Started, Which NZ Insurers Still Offer Multi-Policy Discounts in 2026?

As of 2026, the landscape has fundamentally shifted. Most major insurers, including State, AMI, AA Insurance, and Tower, have officially removed multi-policy discounts in favour of risk-based pricing. Currently, only niche or challenger brands like MAS and Cove still offer traditional bundling incentives to their customers.

Step 1. The Disappearing Act: Multi-Policy Discounts (MPD)

The Issue

You might still see a "Multi-Policy Discount" line item on your renewal notice today, but it is likely on borrowed time. Major players have been moving away from fixed-percentage discounts for new and existing customers, transitioning instead to "net-rated" pricing where the price reflects the specific risk, not the number of policies you hold.

The Data

Insurer | Removal for New Policies | Removal for Renewals |

State Insurance | March 2024 | May 2024 |

AMI | August 2024 | October 2024 |

AA Insurance | 28 January 2025 | 28 January 2025 |

Vero | 1 May 2025 | From 1 May 2025 |

AMP & ANZ | 1 May 2025 | From 1 May 2025 |

Tower Insurance | 28 January 2026 | 28 January 2026 |

Trade Me Insurance | 28 January 2026 | 28 January 2026 |

The Lesson

If you are sticking with one provider solely for a discount that is being deleted or absorbed into the base premium, you are effectively paying a premium for a benefit that no longer exists. Check your latest renewal letter carefully; if the discount line is gone or reduced, your reason for staying should be too.

Step 2. The Rise of "Risk-Based Pricing"

The Issue

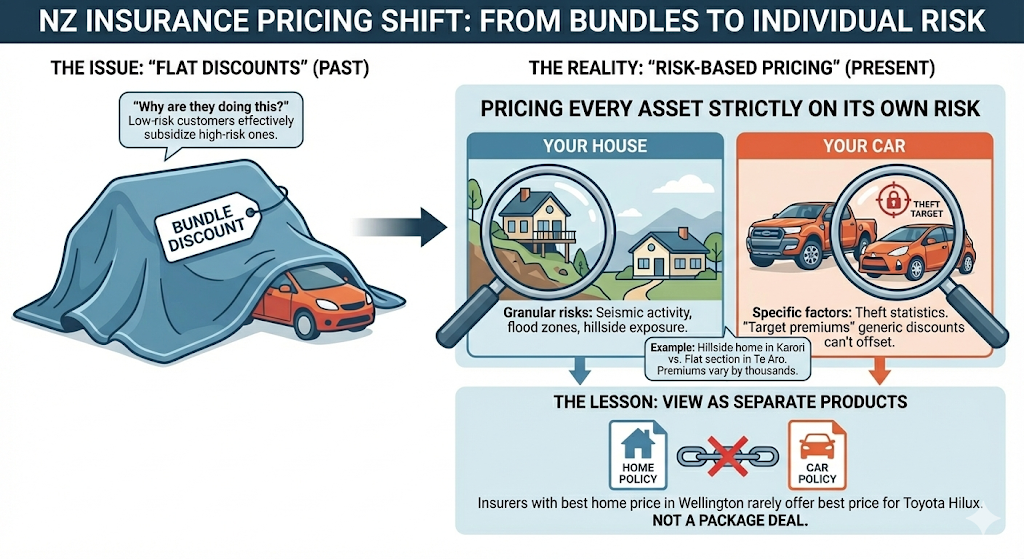

"Why are they doing this?" is the one of the most common questions. Insurers are moving away from "flat discounts" (where low-risk customers effectively subsidise high-risk ones) to "risk-based pricing".[a]

The Reality

In the past, a bundle discount might have masked the fact that your car insurance was actually overpriced. Now, insurers are pricing every single asset strictly on its own risk.

Your House: Priced on granular risks like seismic activity, flood zones, and hillside exposure. This can cause premiums to vary by thousands between suburbs—for example, a hillside home in Karori vs a flat section in Te Aro.

Your Car: Priced on specific factors like theft statistics. High-theft vehicles like the Ford Ranger or Toyota Aqua now face "target premiums" that a generic discount can't offset.

The Lesson

You must now view your insurance as separate products, not a package deal. The insurer that offers the best price for your home in Wellington is rarely the same insurer that offers the best price for your Toyota Hilux.

Step 3. The "Split Strategy": Why Decoupling Saves Money

The Issue

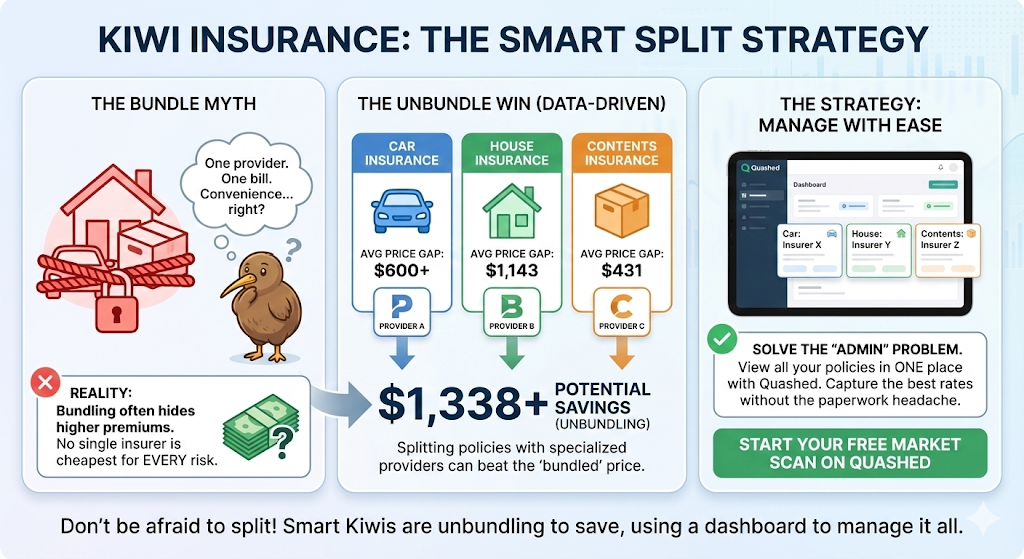

Most Kiwis assume that "bundling" their car and home insurance with one provider saves them money and hassle. They worry that splitting policies means double the paperwork. However, this convenience often comes with a hefty price tag that goes unnoticed until you compare.

The Data

Our data indicates that no single insurer is the cheapest for every risk. While one provider might offer a great rate for your home, they could be overcharging for your car. By decoupling your policies, you can capture the best rate for each asset.

The Price Gap: It isn't just about your car. While we frequently see price gaps of $600+ between insurers for the exact same vehicle, the differences in property cover are even more extreme. As seen in our 2025 NZ insurance price benchmark, our market scans revealed an average price gap of $1,143 for house insurance and $431 for contents insurance.

The Split Win: No single insurer is the cheapest across every category. Often, using two specialised providers (e.g., a dedicated car insurer + a separate home insurer) can beat a "bundled" price from a single provider.

Average Savings: The numbers add up fast when you unbundle. Drivers comparing quotes on Quashed found average potential savings of $384 per year. When you add the average savings found for House $653 and Contents $301 policies, "splitting" your providers could become a financial win.

The Strategy

Don't be afraid to split. Use the Quashed Dashboard to view all your policies in one place, regardless of which provider they are with. This solves the "admin" problem while letting you pocket the savings.

Step 4. The Hold Outs: Who Still Bundles?

The Issue

While the industry giants (IAG brands like State and AMI, plus AA Insurance) are exiting the discount game, a select few providers are bucking the trend. These "Hold Outs" use discounts to build membership or disrupt the market.

The Data

If you are determined to bundle, these are the verified providers where a Multi-Policy Discount (MPD) is still available in 2026:

Insurer | MPD Status | The Detail |

MAS (Medical Assurance Society) | Active | While MAS maintains a multi-policy discount, they have also moved toward risk-based pricing. Note: Membership eligibility remains the primary hurdle for most Kiwis, as you must meet specific professional criteria to join. |

Cove Insurance | Active | As a challenger brand, Cove incentivises bundling with discounts typically up to 10%. Uniquely, they allow "cross-category" bundling (e.g., Pet + Car), making them a top choice for younger demographics who may not yet own a home. |

Final Verdict: Insurance Loyalty is Leaving NZ, Long Live Comparison

The era of the "set and forget" bundle is over. With major insurers removing or changing multi-policy discounts, the market has shifted to a "best price wins" model.

This is actually good news for consumers who are willing to be active. It means you can cherry-pick the absolute best value for your car, your home, and your contents without being penalised for spreading your business.

Key Recommendation: Do not auto-renew your bundle in 2026.

Check your renewal: Has the discount disappeared or been "baked in"?

Test the market: Compare your insurance policies separately using Quashed.

Split and Save: Move your car to a specialist provider if the standalone savings outweigh your multi-policy discount.

Compare your policies now with the Quashed Market Scan to see if you can save.

Related Reading

Don't stop here—arm yourself with the latest data and expert tips to ensure you never overpay for cover again:

Multi-Policy Discounts on Insurance in NZ: What You Need to Know in 2025 A deep dive into the specific changes from State, AMI, and AA, and why regulatory pressure is forcing this market shift.

Ultimate NZ Guide to Car Insurance (2025): Compare & Find the Best and Cheapest Cover This comprehensive guide breaks down everything you need to know to save on your car insurance, including how premiums are calculated and what to look for in a policy.

How to Save Money on Insurance: Must Know in 2025 From adjusting your excess to bundling policies, we outline the high-impact strategies that can reduce your costs immediately.

How to Lower Your Contents Insurance Costs From raising your excess to avoiding the "monthly payment trap," discover research-backed ways to slash your premium.

Comprehensive vs Third Party Fire & Theft vs Third Party (Full NZ Breakdown) Review our breakdown of vehicle policy tiers to ensure you aren't over-insuring an older run-about or under-insuring your daily driver.

Does bundling your insurance make sense? We test the market to see if bundling actually saves money or if splitting your policies is the smarter move.

FAQs: Multi-Policy Discounts & Bundling (2026)

1. Which insurers are removing multi-policy discounts?

Our market data indicates a widespread industry shift away from fixed-percentage discounts.

Already Removed/Phasing Out (2024–2025): Major providers like State, AMI, and AA Insurance have already begun or completed the removal process. Vero, along with its partners AMP and ANZ, will remove discounts starting 1 May 2025.

Removing in 2026: Tower Insurance and Trade Me Insurance have confirmed they will remove the discount starting 28 January 2026.

2. Do any insurers still offer bundle discounts?

It varies by provider, but yes, some still use them. MAS is a key "hold out" that offers a standard multi-policy discount for two different policy types, plus a higher-tier "Goldshield" discount if you hold house, contents, and car policies together. Cove also offers discounts (typically up to 10%) to incentivise bundling. However, these are exceptions rather than the rule in 2026, so always check if the base premium is competitive first.

3. Does bundling ever still save money?

It can, but you must check the final price, not just the discount percentage. A 10% discount on an expensive policy might still cost you more than a separate policy from a competitor with no discount. You should compare the total dollar amount of separate policies vs. a bundle.

4. How significant is the price difference between insurers?

Our data indicates that the gap between the most expensive and cheapest providers is substantial. For the exact same vehicle, we frequently see price gaps of $600+. The difference is even more extreme for property; our 2025 Market Scans revealed an average price gap of $1,143 for house insurance and $431 for contents insurance. This suggests that "loyalty" to a single bundle could be costing you significantly more than the discount itself.

5. Will managing separate policies create more paperwork?

Many Kiwis worry that splitting policies means double the admin, but digital tools have solved this "convenience penalty". You can now upload policies from any insurer into the Quashed Dashboard to view your car, home, and contents cover in one place, regardless of which provider they are with. This allows you to cherry-pick the best rates from different specialists while keeping your management centralised.

6. How does "risk-based pricing" affect specific assets like my car or home?

Insurers generally now price every asset strictly on its own risk rather than spreading risk across a bundle.

For Homes: Pricing relies on granular risks like seismic activity or hillside exposure. This can cause premiums to vary by thousands between suburbs—for example, a hillside home in Karori versus a flat section in Te Aro.

For Cars: Models with high theft statistics, such as the Ford Ranger or Toyota Aqua, now may face "target premiums" that a generic multi-policy discount is unlikely to offset.