Contents Insurance 2025 Quashed Hacks: Get Maximum Cover for Minimum Price

Why Your Insurance Bill Is Too High

In today's economy, the cost of protecting your possessions—your furniture, electronics, clothing, and priceless valuables—is constantly on the rise. Many policyholders simply auto-renew, unknowingly locking themselves into costly, mediocre cover. The challenge isn't just finding the cheapest contents insurance policy; it's finding the best value—a policy that delivers maximum protection for your circumstances without draining your bank account.

Source: Figure.NZ, using data from Stats NZ. Licensed under CC BY 3.0 NZ.

Immediate Action: Stop letting insurers dictate your price. Run a free Quashed Market Scan and see competitor quotes side-by-side. At Quashed, we believe you shouldn't have to choose between a low premium and comprehensive protection. This guide reveals the smart strategy to unlock significant savings and secure the gold-standard cover you deserve.

The Price Hacks: 4 Ways to Instantly Lower Your Contents Insurance Premium

The sticker price on a contents insurance quote is just the starting point. Savvy consumers know that most insurers offer discounts and levers you can pull to dramatically reduce your annual premium. Here are the fastest ways to chip away at the cost:

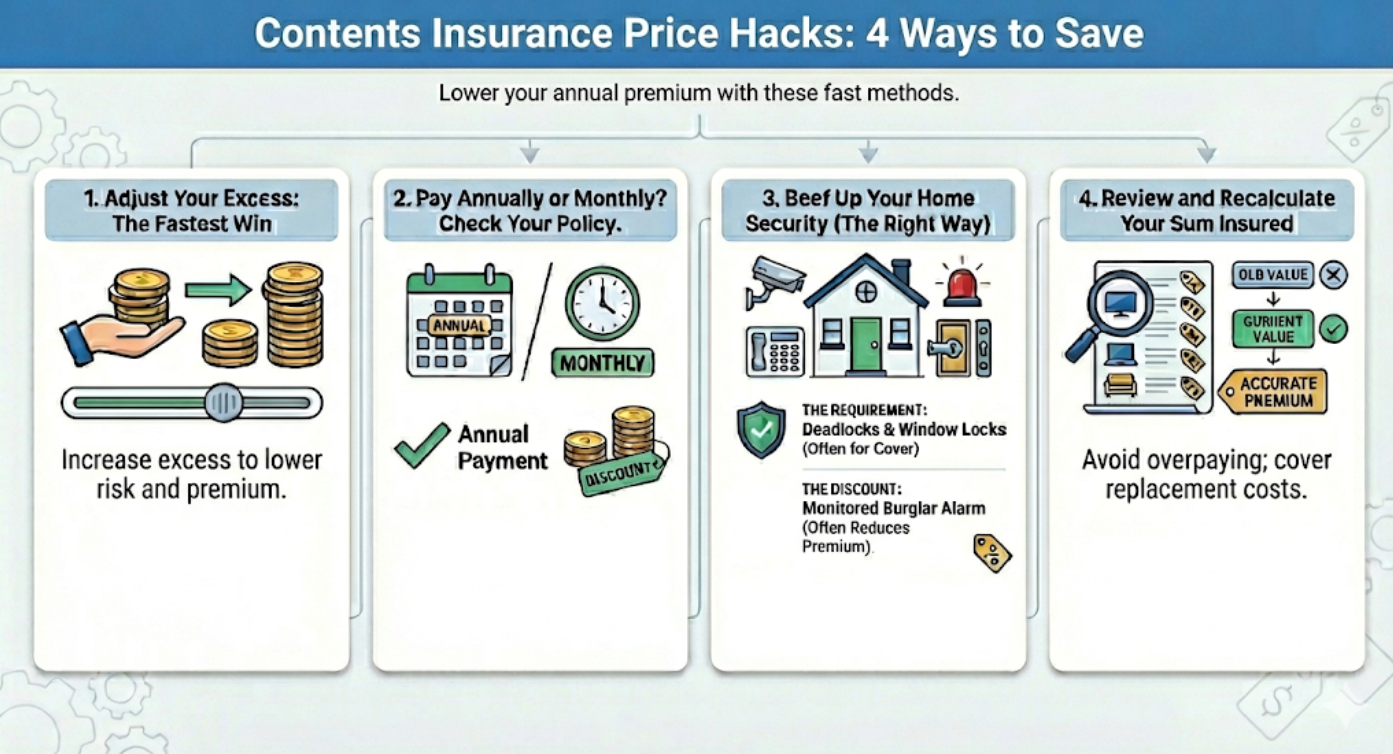

1. Adjust Your Excess: The Fastest Win

The excess is the amount you pay out-of-pocket when you make a claim. By increasing your excess from, say, $500 to $1,000, you signal to the insurer that you will cover smaller incidents yourself, lowering their risk and resulting in a significantly cheaper contents insurance premium.

Actionable Tip: Only choose an excess you can comfortably afford to pay tomorrow if disaster strikes.

2. Pay Annually or Monthly? Check Your Policy.

Some insurers charge a fee for the convenience of monthly or fortnightly payments. This can add significantly to your annual cost. Paying your premium in one lump sum may be a simple way to secure a discount and keep more money in your pocket.

3. Beef Up Your Home Security (The Right Way)

Insurers love low-risk homes, but it is vital to distinguish between what gets you a discount and what is a requirement.

The Requirement: Many policies require deadlocks on all external doors and key locks on windows just to qualify for theft cover. If you don't have them, you might not be covered at all.

The Discount: A monitored burglar alarm is often the trigger for a premium reduction.

Actionable Tip: Always inform your provider about security upgrades. Even if a specific discount doesn't apply, it improves your risk profile which can stabilize your premium.

4. Review and Recalculate Your Sum Insured

Are you paying to insure belongings you sold five years ago? Overestimating your Sum Insured (the maximum payout) means overpaying every year. Conversely, underinsuring is a massive risk.

Natural Hazards Cover: Since 2019, the Natural Hazards Commission (NHC/Tokū Tū Ake) no longer covers personal contents. This means your private insurer covers 100% of the loss for your belongings in a natural disaster, up to your chosen Sum Insured. You do not need to worry about a government "cap" for contents, but you must ensure your total Sum Insured is high enough to replace everything you own if a major event occurs.

Resource: For a deep dive on valuation, check out our guide: How to Set Your Sum Insured for Contents Insurance.

The Cover Deep Dive: What Makes a Policy "The Best"?

The best policy isn't the cheapest one; it's the one that pays out when you need it most. Focusing purely on premium cost can leave you dangerously underinsured. "Best" contents insurance means maximising these three critical coverage areas:

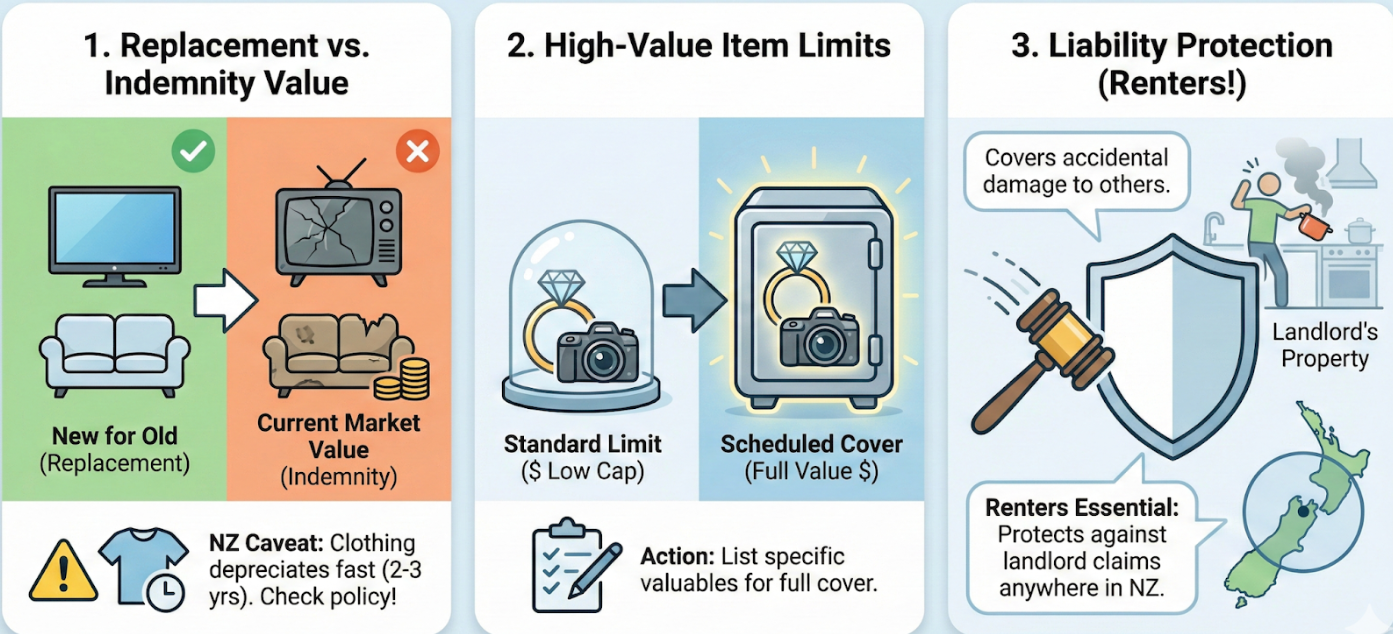

1. Replacement Value vs. Indemnity Value - This is arguably the most crucial feature to compare.

Replacement Value (New for Old): The insurer covers the full cost of replacing your lost or damaged item with a comparable new item, regardless of its age. This is the gold standard for electronics, furniture, and appliances.

Indemnity Value (Market Value): The insurer pays only the item's depreciated value (its worth at the time of loss).

Crucial NZ Caveat: Be aware that even comprehensive "Replacement" policies usually revert to Indemnity Value for items like clothing, footwear, and linen that are over a certain age (often 2-3 years).

2. Portable and High-Value Item Limits

Standard policies place low limits on specific high-risk items like jewellery, watches, artwork, and bicycles—especially when they are taken outside the home.

The Check: If you have a bike worth $3,500 and the standard policy limit is $2,000, you are $1,500 short. Aim for a policy that allows you to list these specific items for higher, scheduled cover.

3. Personal Legal Liability Protection Often overlooked, this cover protects you if you accidentally cause damage to someone else's property or injure them.

For Renters (Tenant's Liability): This is essential. If you accidentally cause damage to your landlord's property—for example, a kitchen fire that damages the building—this cover protects you from being held personally liable for the repair costs.

The Scope: It generally covers you anywhere in New Zealand, not just inside your home (e.g., if your shopping trolley scratches a car in the supermarket carpark).

The Golden Rule: Compare Policies to Get the Best Price AND Cover

You can apply all the cost-saving hacks in Section 1, but if you don't shop around, you will still be overpaying. Insurers use complex, risk-based pricing models that mean Company A might offer you the exact same comprehensive policy for hundreds less than Company B.

The only way to verify that you have found both the cheapest price and the best cover is to conduct a detailed, side-by-side comparison using tools like Quashed’s market scan.

The Quashed Advantage

Instead of spending hours filling out forms on multiple insurer websites and wading through jargon-heavy policy documents, Quashed's innovative platform allows you to:

Enter Your Details Once: Get quotes from all leading providers simultaneously.

See Policy Benefits Clearly: Our comparison tool strips away the confusion, showing you exactly where the limits and features differ—for example, instantly highlighting which policy offers higher cover for your contents.

Find Hidden Savings: Identify the company offering the greatest discount for your specific risk profile (e.g., your address and details).

Read More & Save More!