Open vs. Named Driver: Car Insurance Excess Guide (2026)

New Zealanders value flexibility. We lend our cars to flatmates for a grocery run, let partners drive on road trips, and hand the keys to visiting relatives.

Most Kiwi drivers operate on the assumption that their "Comprehensive" policy covers the vehicle, regardless of who is behind the wheel. While "Open Driver" policies are common in New Zealand, they often come with a stinging financial tail in the fine print: the Unlisted Driver Excess.

At Quashed, we believe you should pay for cover, not surprises. Our research shows that while Open Driver policies offer convenience, they require a clear understanding of the "excess triggers" buried in your policy wording.

This guide explains the difference between Open and Named driver policies and how to avoid the "hidden excess" trap.

Step 1. The Definitions: "Open" vs. "Named"

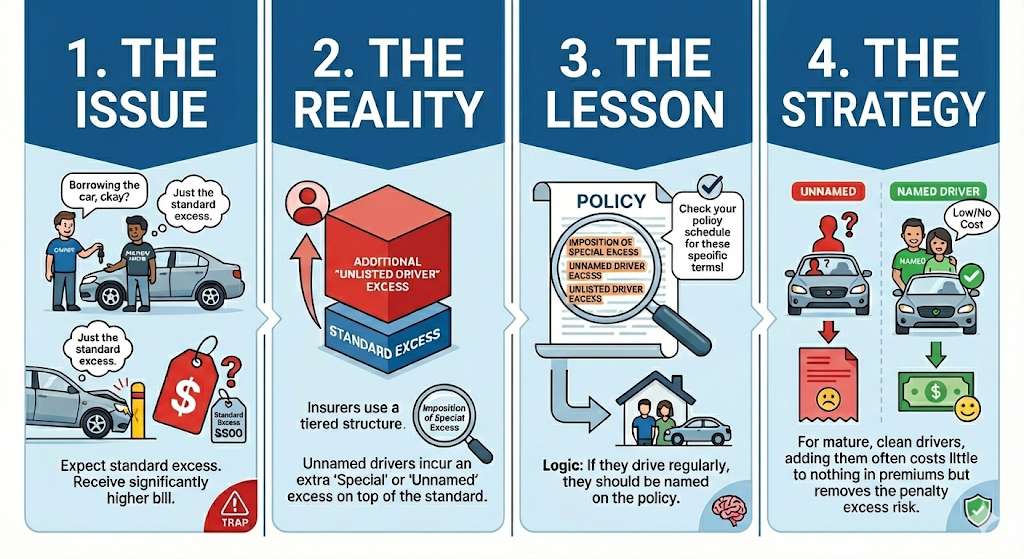

The Issue

There is a fundamental misunderstanding of what "Open Driver" actually means in NZ. Many policyholders interpret "Open" as "Unrestricted"—a "free pass" to let anyone drive. This leads to the dangerous assumption that coverage is identical regardless of who is in the driver's seat.

The Data

Insurance premiums are effectively a calculation of risk probability. An insurer needs to know who is driving to accurately predict the likelihood of a crash.

Named Driver Policy: This is a "Known Risk" agreement. You list every person who frequently drives the car. The insurer assesses the specific age, gender, and claim history of these individuals to calculate a precise—and often lower—premium.

Open Driver Policy: This is an "Unknown Risk" agreement. The insurer agrees to cover drivers they have never assessed (subject to license conditions). Because they cannot price this risk upfront, they manage it by shifting the financial burden to you at claim time. "Open" does not mean "free"; it means "open to other drivers, but the price tag changes depending on who has an accident".

The Lesson

An "Open" policy is not a blanket of protection; it is a conditional contract. The insurer offers you the convenience of not listing every occasional driver, but in exchange, they reserve the right to charge a significantly higher contribution (excess) if one of those unlisted drivers causes damage. You are essentially trading administrative convenience for higher financial exposure.

Step 2. The "Unlisted Driver" Excess Trap

The Issue

The most common trap Kiwis fall into is the "Unlisted Driver Excess." You have a standard excess you are comfortable paying. You lend your car to a partner, flatmate, or friend who lives with you but isn't named on the policy because you rely on the "Open Driver" clause. They have a minor accident—perhaps backing into a bollard or scraping a wall. You expect to pay your standard excess, but you receive a bill that is significantly higher.

The Data

Insurers use a "tiered" excess structure to manage the risk of unknown drivers. Most policies apply an additional excess (often called an "Imposition of Special Excess", "Unnamed Driver Excess", or “Unlisted Driver Excess") on top of your standard excess if the driver is not named.

The Lesson

Check your policy schedule specifically for the terms "Imposition of Special Excess", "Unnamed Driver Excess", or “Unlisted Driver Excess". The logic is straightforward: if someone is regularly driving your car they should be named.If your partner or flatmate drives the car, name them. For mature drivers with clean histories, this often costs little or nothing in additional premiums but removes the risk of the penalty excess entirely.

Step 3. The "Under 25" Danger Zone

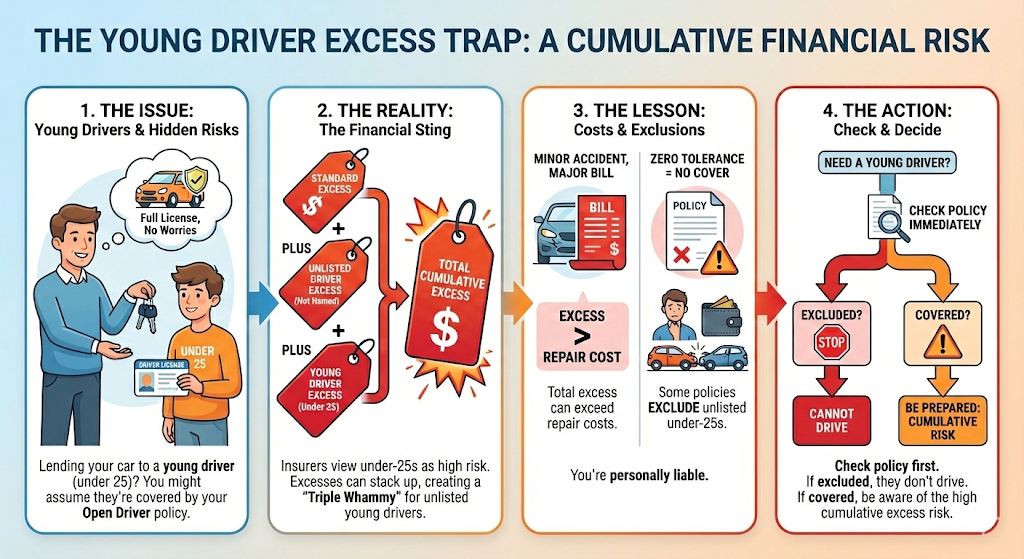

The Issue

In the eyes of an insurer, drivers under 25 represent a significantly higher risk. Major New Zealand insurers manage this with specific, often high-cost categories:

AA Insurance: Distinguishes between a "Young Driver Excess" (for those you’ve already listed) and a much higher "Unlisted Young Driver Excess".

State Insurance: Can apply an "Unlisted Driver Excess" reaching as high as $2,500 in some 2026 policy schedules if the driver is under 25 and not named.

Tower Insurance: Offers a "No under 25 driver" exclusion to lower premiums. If you select this, you have zero cover for young drivers, meaning you are personally liable for all damages.

The Data

If an unlisted young driver crashes your car, these costs are often cumulative. You don't just pay one; you pay the sum:

Standard Excess.

PLUS Unlisted Driver Excess.

PLUS Young Driver Excess.

Note on License Types: In NZ, an unlisted driver on a Learner or Restricted license often triggers an "Inexperienced Driver" excess, even if they are over 25. A 30-year-old on a Learner license is viewed as high-risk as a teenager by many providers.

The Lesson

The total payable excess can easily exceed the cost of the repairs themselves for minor accidents.

Zero Tolerance: Be aware that some policies explicitly exclude unlisted drivers under 25 entirely (age bracket may vary by provider). In this scenario, you have no cover at all—you would be personally liable for your own repairs and the damage to any other cars involved.

The Action: If a young driver needs to use the car, check your policy immediately. If the policy excludes them, they cannot drive. If it covers them, be prepared for the cumulative excess risk.

Step 4. The Cost-Benefit Analysis

The Issue

The primary reason people don't list drivers is the fear of price increases. "I don't want to list my flatmate because it will raise my premium" is the standard objection. Kiwis often choose to "hide" drivers to save money on the upfront premium.

The Data

This fear is often unfounded or exaggerated, depending on who you are adding.

Low Impact: Adding an experienced, clean-driving adult (e.g., a 30+ partner) often has little or no upward effect on your annual premium, but insurers differ and some changes can alter your premium or excess — so always compare first.

High Impact: Adding a high-risk driver (younger, inexperienced, or with a history of claims) will increase your premium. However, this increase is the "true cost" of the cover. By not paying it, you aren't saving money; you are simply gambling that they won't crash. If they do, the unlisted driver excess will likely dwarf the premium savings you made.

The Lesson

Read your policy carefully and don't guess—test the market. Use the Quashed Market Scan to see premium prices and check provider policies.

Insurer | Standard Excess | Unlisted Driver Excess (Under 25) | Can you exclude Under 25s? |

AA Insurance | Choice of $300–$1,000+ | $1,000+ (Unlisted penalty) | Yes |

State | Varies by policy | Up to $2,500 (Unlisted) | Yes |

Tower | Varies by policy | Cumulative (Triple Whammy) | Yes (Optional Exclusion) |

AMI | Varies by policy | High "Unnamed" Penalty | Yes |

Pro Tip: Always check your Certificate of Insurance. If you have opted for an "Under 25 Exclusion" to save on premiums, your "Open Driver" policy will not cover a young driver.

Final Verdict: Name Them or Pay the Price

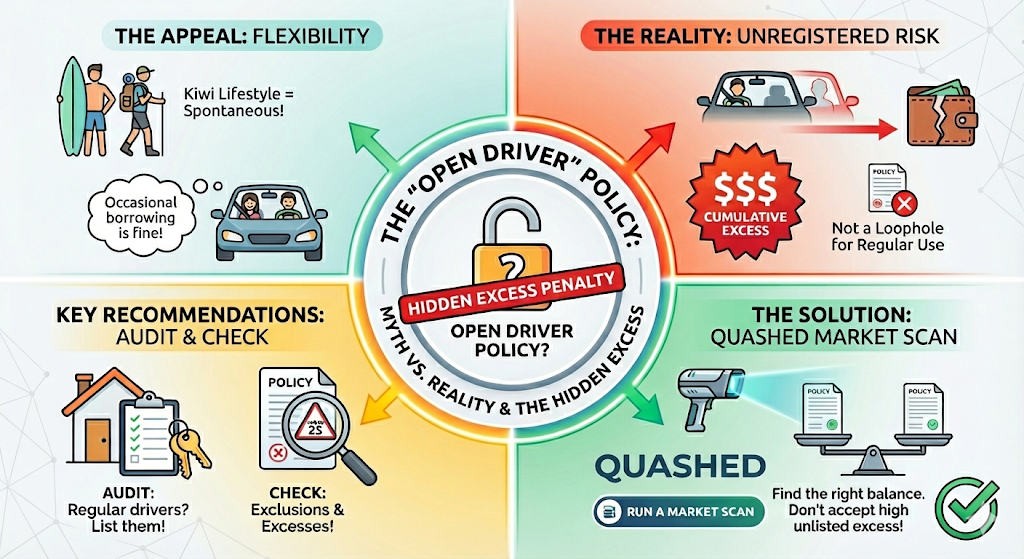

Flexibility is a key part of the Kiwi lifestyle, but in the insurance world, unregistered flexibility comes at a premium. The "Open Driver" policy is designed for the occasional, unplanned borrower. It is not designed as a loophole for regular drivers you simply forgot—or chose not—to list.

The "Hidden Excess" is essentially a penalty for not updating your policy to reflect reality. If you opt for the convenience of an Open policy without understanding the excess triggers, you are fronting a significant portion of any claim.

Key Recommendations

Audit your household: If someone has their own set of keys or drives the car weekly, put their name on the policy.

Check the exclusions: Specifically look for exclusions or high excesses for drivers under 25.

Compare Now: Don't accept a high unlisted driver excess as the only option. Run a Quashed Market Scan to find a policy that balances flexibility with fair excess structures.

Related Reading

Don't stop here. Stay informed with our latest market reports from December 2025:

Assurant Car Insurance NZ Review 2026 Discover why this challenger brand is consistently ranking as one of the cheapest options for cars valued between $5k–$25k in our latest pricing tests.

2026 Autosure Car Insurance Review: Worth the Money? A deep dive into one of NZ's most trusted brands for used vehicles, analysing their Mechanical Breakdown Insurance (MBI) and claims reliability.

2026 Provident Insurance Review We evaluate this 100% NZ-owned specialist to see if their unique perks like "incorrect refuelling" cover and digital claims process make them the best local choice.

Tower Insurance 2026: Quashed Ultimate Kiwi Review The ultimate guide for digital natives. We break down Tower's "excess-free glass" benefits and how their risk-based pricing affects your premiums.

MAS Insurance 2026 Reviewed — The Quashed Kiwi Breakdown Is the "Goldshield" discount worth sticking around for? We analyse the value of this premium mutual insurer for families with multiple assets.

Is Initio Insurance Right for Kiwis? 2025 Review & Verdict The verdict on this digital-first landlord and home insurer. See how their built-in "loss of rent" cover stacks up against traditional providers.

FAQs: Open vs. Named Drivers

1. Can my friend drive my car if they aren't on my insurance?

Generally, yes, if you have an "Open Driver" policy. However, if they have an accident, you will likely have to pay a significantly higher excess because they are unlisted.

2. Does adding a driver increase my premium?

It depends on the driver. Adding a mature driver with a clean record usually has little negative impact on your premium. Adding a driver under 25 will likely increase your premium, but it ensures they are fully covered without a massive excess.

3. How does the "Unlisted Driver Excess" work?

It is vital to understand that this excess can stack on top of your standard excess rather than replacing it. This means the costs can be cumulative; you are liable for your standard agreed excess plus the additional unlisted driver penalty. The total bill is the sum of these amounts, which can be significantly higher than a standard claim.

4. Does my insurance cover me driving someone else's car?

Not usually. Your comprehensive policy covers your car. It generally does not cover you driving other vehicles. You rely on their insurance when you drive their car.

5. Do I need to list my partner if I have an Open Policy?

Yes, it is highly recommended. While an Open Policy allows them to drive, if they are not specifically named on the policy schedule, they are considered an "Unlisted Driver". This means the extra unlisted driver excess would apply if they had an accident, even if you are married or living together.

6. Can a Learner Driver drive on my Open Policy?

Yes, in most cases, provided they are legally supervised by a driver who meets the supervisor requirements (usually holding a full NZ licence for 2+ years). However, the "Unlisted Driver Excess" and "Under 25 Excess" (if applicable) will still apply if they have an accident. Always check your specific policy wording, as some insurers exclude young drivers entirely.

7. How do I add a driver to my policy?

Adding a driver is usually a quick process that can be done via your insurer’s online portal or a phone call. Gather their full name, date of birth, and details of their driving history (including any past accidents or license suspensions). It is best to do this before they get behind the wheel, as you cannot add them retroactively after an accident.

8. If the unlisted driver is an experienced adult (over 25), does the extra excess still apply?

Yes. The "Unlisted Driver Excess" is a penalty for the driver not being named, regardless of their age or experience. Being over 25 means you avoid the specific Young Driver Excess, but you are still liable for the Unlisted Driver Excess if they are involved in an accident. The only way to avoid this risk is to name them on the policy.

9. If the accident wasn't the unlisted driver's fault, do I still pay?

Not necessarily, but it is much harder to have the excess waived. While major insurers like AMI, State, and AA may waive the excess if the other driver is identified and 100% at fault, they often strictly apply unlisted driver penalties during the initial claim process. If your driver isn't named, you are more likely to have to pay the "Unlisted Excess" upfront and wait for the insurer to recover costs from the third party before you get a refund.