Auckland vs. Wellington: What’s The Real Cost Of Protecting Your Stuff?

Moving between Wellington and Auckland isn’t just about swapping your wind jacket for a raincoat. These days, it’s also about understanding why your contents insurance might suddenly cost more—or less. As more Kiwis relocate between our two biggest cities, many are noticing surprising shifts in their insurance premiums. While both cities present unique challenges—Wellington’s fault lines and Auckland’s unpredictable weather—insurers assess these risks differently. This guide unpacks why your postcode matters when it comes to protecting your belongings and explores the factors driving the cost differences between these two cities. Whether you’re planning a move or just curious about why your premium differs from your cousin’s across the Strait, we’ll break down what’s influencing the market right now.

How does where you live affect contents insurance costs in NZ?

When it comes to contents insurance premiums, the biggest factor is risk—the higher the risk, the higher the premium. Your location plays a major role in how insurers calculate your premiums. Both Wellington and Auckland present unique challenges, meaning the cost of protecting your belongings can vary significantly based on where you live.

Want to understand more about contents insurance? Check out our further reading section below.

Which city has higher contents insurance premiums: Wellington or Auckland?

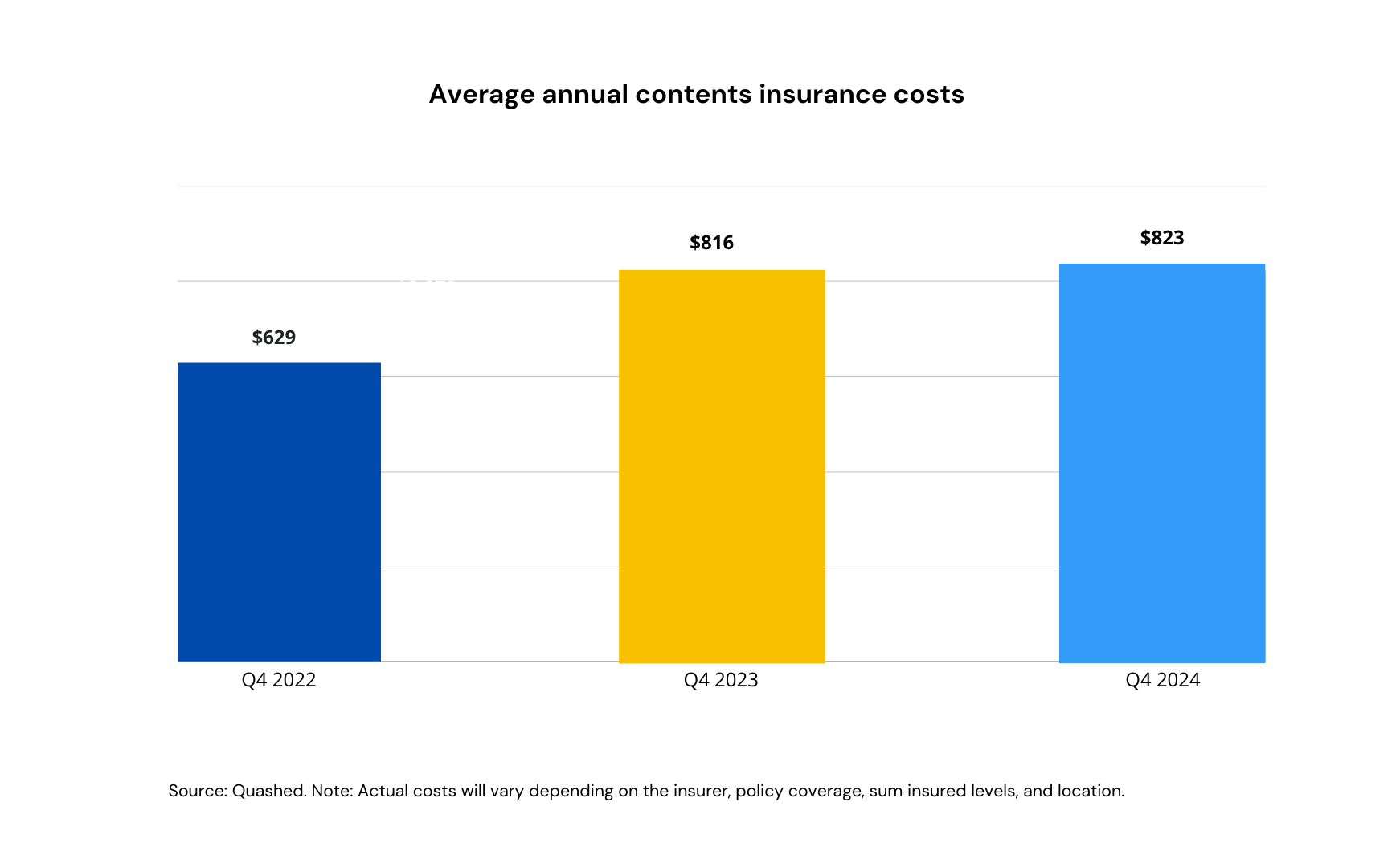

According to the latest Quashed Index data (Q4 2024), the average contents insurance premium in New Zealand is $823 per year, reflecting a modest 0.9% increase from Q4 2023.

Where you live can significantly affect your premium, as insurers assess risks differently across regions:

Wellington: The average contents insurance premium in Wellington is $990 per year, $167 higher than the national average. This is largely due to higher seismic risk, making claims for earthquake-related damage more likely. Insurers factor in this increased exposure when pricing policies.

Auckland: In contrast, Auckland’s average contents insurance premium is $754 per year, $69 below the national average. While Auckland faces weather-related risks like storms and flooding, the absence of significant earthquake risk helps keep contents insurance costs lower.

Curious about how to save on contents insurance? Check out our further reading section below.

What affects contents insurance premiums in Auckland and Wellington?

So why do premiums vary between Wellington and Auckland? Let’s break it down:

Natural Disasters

Wellington: One of the primary reasons for Wellington's higher premiums is the risk of earthquakes. Located on a fault line, Wellington is prone to seismic activity, which insurers factor into premiums.

Auckland: While Auckland isn’t at risk for earthquakes like Wellington, it’s still vulnerable to severe weather events, such as storms and occasional flooding. While these can still cause damage, the risk of catastrophic loss is generally lower than in Wellington.

Crime rates

Auckland: According Police Data, Auckland recorded 118,046 total reported crimes in 2024, with 85,277 theft incidents and 19,829 burglaries. In contrast, Wellington had 12,072 total reported crimes, including 8,584 thefts and 1,799 burglaries. These crime rate differences contribute to variations in insurance premiums as insurers assess burglary risk when pricing policies.

Wellington: Wellington’s lower crime rate helps offset the higher premiums associated with earthquake risk, making burglary-related premiums more affordable.

Population density and property type

Auckland: With a higher population density, many people in Auckland live in apartments or rental properties. These can sometimes reduce premiums thanks to added security features, like controlled entry or security cameras. However, shared walls and neighbouring tenants can increase the risk of accidental damage, which insurers take into account.

Wellington: Wellington has more older homes, especially in central areas like Mount Victoria or Aro Valley. Older homes can result in higher premiums due to the risk of damage during natural disasters, like earthquakes, and potential structural weaknesses.

How can I lower my contents insurance costs?

Whether you're in Auckland or Wellington, here are some tips to help lower your contents insurance premiums:

Increase your excess

Choosing a higher excess can lower your premiums. Just ensure it’s an amount you’re comfortable paying if you need to make a claim.

Improve security

Installing security features like deadbolts, window locks, or security cameras can help reduce your premiums. Auckland renters, in particular, may benefit from these upgrades in higher-crime areas.

Shop around

Use Quashed to compare contents insurance prices in real time from different providers.

Review your coverage

Make sure you're not overinsuring. Check that your contents insurance reflects the actual value of your belongings, and make adjustments as needed.

How does Quashed make comparing contents insurance easier?

When it comes to contents insurance, Quashed makes it easy. Here’s how:

Real-time comparisons: Quashed lets you compare real-time contents insurance quotes from multiple insurers, giving you up-to-date pricing to help you make an informed decision.

Personalisation: Quashed helps you tailor your search based on your location and needs.

Clear & easy-to-understand: No more complex jargon. Quashed breaks down your options in simple terms, making it easy to understand exactly what’s included in each policy.

Save time: Forget spending hours searching for quotes. Quashed makes insurance easier by allowing you to see multiple quotes in one place.

Wondering if you're overpaying for insurance?

Join 45,000+ Kiwis comparing and saving on their premiums.

Whether you're in a Wellington apartment or an Auckland townhouse, your location affects your rates—see how much you could save.

Get free, personalised quotes in minutes.

Further reading

Here are some helpful reads:

Complete Guide to Contents Insurance: A 101 explainer guide for Kiwis.

Key Considerations with Contents Insurance: A how-to guide for those wanting more.

Contents Insurance Costs: Learn more about the costs.

Lower your Contents Insurance Costs: Useful tips on reducing those costs!

FAQs

Why are contents insurance premiums different in Auckland and Wellington?

Contents insurance premiums differ due to risk factors like earthquakes, crime rates, and insurer claim data. Wellington often has higher premiums due to its seismic risk, while Auckland’s pricing can vary based on crime rates and weather-related risks.

Is it harder to get contents insurance in Wellington compared to Auckland?

Yes, Wellington residents may face stricter underwriting criteria or higher premiums due to earthquake risks. Some insurers may have more exclusions or require additional documentation compared to policies available in Auckland.

Why has my contents insurance premium increased even though I haven’t made a claim?

Premiums can rise due to inflation, rebuilding costs, or increased claims in your area. Even if you haven’t made a claim, insurers adjust pricing based on overall risk factors, such as a rise in natural disasters or theft rates.

How can I reduce my contents insurance premium in Auckland or Wellington?

You can lower your premium by:

Increasing your excess – A higher excess usually means lower premiums.

Reviewing your sum insured – Ensure you’re not over-insuring or under-insuring.

Bundling policies – Combining home and contents insurance often leads to discounts.

Enhancing security – Installing alarms or security systems can lower risk and costs.

Comparing providers – Insurance pricing varies, so shopping around can help.

Are certain insurers better for Auckland or Wellington contents insurance?

Some insurers specialise in high-risk areas like Wellington, while others offer more competitive rates in Auckland. Comparing policies from multiple providers ensures you get coverage that suits your location and risk profile.

Does living in an apartment vs. a house affect contents insurance pricing?

Yes, apartment dwellers in both cities may have lower premiums due to reduced theft risk and fire protection measures. However, body corporate rules and shared building insurance may affect what’s covered.

Will my contents insurance cover earthquakes in Wellington?

Most policies include earthquake coverage, but check your policy wording for exclusions and excess levels. Some insurers offer add-ons for additional protection, and EQC (Earthquake Commission) cover may apply.

How do I check if I’m over-insured or under-insured?

Use an online contents insurance calculator or make an inventory of your belongings to estimate replacement costs. Avoid setting your sum insured too low, as you might not get enough to replace everything in a claim.

Does my landlord’s insurance cover my contents?

No, landlord insurance covers the building but not your personal belongings. Tenants should have their own contents insurance to protect against theft, fire, and accidental damage.

This article provides general information only and does not constitute insurance or financial advice. Insurance policies vary between providers, and you should check with your insurer or a licensed adviser for guidance specific to your situation. For full details, refer to Quashed’s terms and conditions.