MAS Insurance 2026 Reviewed — The Quashed Kiwi Breakdown

Quick overview: MAS is a long-standing, New Zealand-owned mutual insurer offering home, contents, motor, life & income protection, and investment products. If you value local ownership, transparent cover, and community impact, MAS is worth considering.

What is MAS?

MAS, Medical Assurance Society, is a mutual insurer, which means it is owned by its members rather than external shareholders. This ensures that MAS prioritizes member value and long-term stability. Read more about MAS’s history and member-focused approach to understand their century-long commitment to Kiwis.

MAS’s Core Products

MAS offers a comprehensive suite of insurance and investment products designed for New Zealanders:

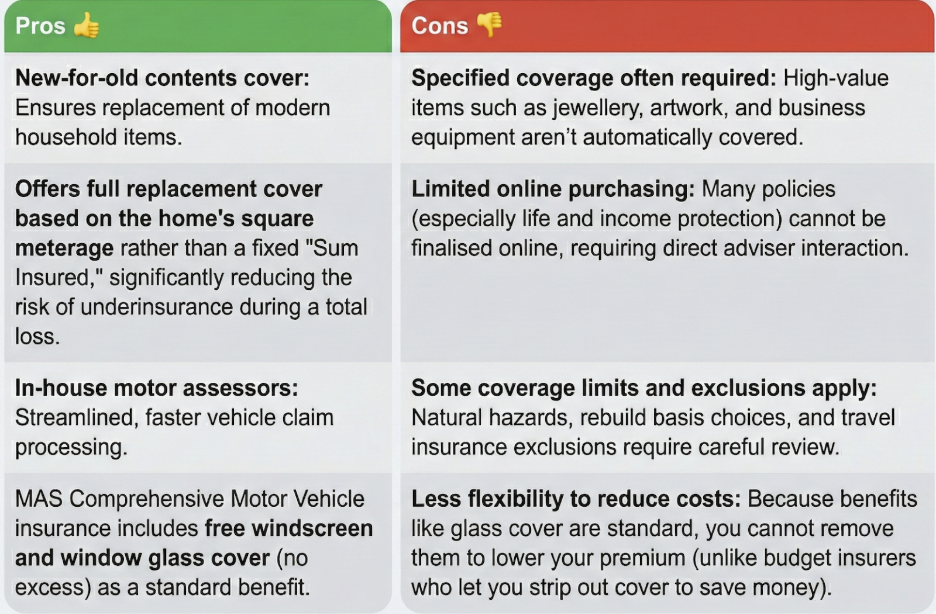

House Insurance: MAS covers your home against a wide range of risks, including fire, storm, flooding, earthquakes, accidental damage, and theft. It also protects permanent structures like walls, roofs, and garages, as well as fixtures such as built-in kitchens and bathrooms.

Contents Insurance: MAS provides new-for-old replacement and optional specified-item coverage for high-value items. Check out their Home Contents Calculator to get a quick estimate!

Motor Insurance: Choose from Comprehensive, TPFT (Third-Party Fire & Theft), or Third-Party only, with optional benefits like hire cars and no-excess glass claims.

Life & Income Protection: MAS Income Security insurance replaces up to 75% of your pre-disability income if illness or injury prevents you from working.

Why MAS Stands Out

MAS’s member-first approach: Being a mutual means MAS reinvests profits into member benefits and community projects.

Streamlined MAS motor claims support: MAS in-house assessors speed up vehicle claims for faster service.

Income protection support: MAS provides clear guidance for income security claims to ensure members know exactly what to expect.

Community impact: The MAS Foundation funds projects improving health and wellbeing across New Zealand.

Highly rated by customers: MAS consistently earns high satisfaction in home, contents, and motor insurance. Customers praise fast claims and responsive support on Reddit, while independent surveys like Canstar confirm strong service, coverage, and value. Insights on MoneyHub also shows similar positive feedback.

Things to Keep in Mind

MAS lets you get quotes online for house, contents, and car insurance, but you can’t fully purchase policies online like other insurers — finalising cover (especially life or income protection) usually requires going through a MAS adviser.

MAS premiums may not always be the cheapest; consider the value of member-focused service and support. Use Quashed Market Scan to see live quotes from other insurers like AMP, Cove, Tower Insurance, or Initio Insurance.

High-value items like jewellery, artwork, or business equipment often require specified coverage. Read policy details carefully.

Always review excesses, natural-hazard terms, and conditions before committing to a policy.

Pros and Cons — MAS Insurance (Quashed Kiwi, 2026)

Who MAS Works Best For

Kiwis who want a member-owned, local insurer instead of shareholder-driven companies.

Homeowners or professionals seeking transparent coverage and strong claims support.

People who care about giving back — MAS members help fund community projects through the MAS Foundation.

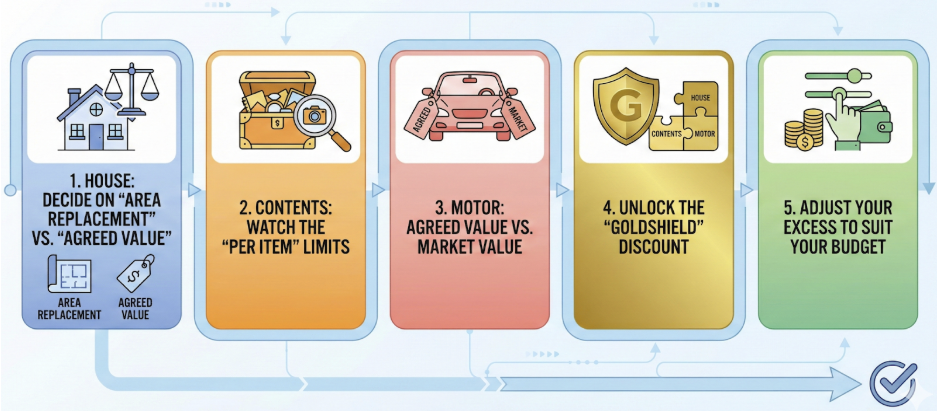

Quashed’s MAS Insurance Buying Checklist

1. House: Decide on "Area Replacement" vs. "Agreed Value" MAS is one of the few insurers in NZ that still offers Area Replacement policies. This is a critical decision point:

Area Replacement: MAS agrees to rebuild your home to the same square meterage, regardless of the cost at the time of the loss. Tip: You must be 100% accurate with your floor area (sqm) measurement—if you get this wrong, you could still be underinsured.

Agreed Value (Sum Insured): You set a maximum dollar limit for the rebuild. This is often better for homes with unique features or where you want to control the premium cost.

2. Contents: Watch the "Per Item" Limits While MAS offers robust "New-for-Old" coverage, standard policies have limits on single items (often capped at $5,000 for items like cameras, jewelry, or musical instruments unless specified).

Action: Audit your home for any single item worth over $5,000. You must list these as "Specified Items" on your policy to ensure they are fully covered.

3. Motor: Agreed Value vs. Market Value

Agreed Value: You and MAS agree on a fixed value for the car. If it’s a total loss, you know exactly what you’ll get paid. This is ideal if you owe money on the car or want certainty.

Market Value: MAS pays what the car is worth at the time of the accident. This is usually cheaper but carries the risk of a lower payout due to depreciation.

Bonus: Remember that MAS Comprehensive cover includes excess-free glass cover as standard. Don't pay extra for a "windscreen add-on" if you are comparing quotes elsewhere—it's already built in here.

4. Unlock the "Goldshield" Discount MAS rewards loyalty heavily. If you insure your House, Contents, and Motor (all three) with them, you qualify for the Goldshield discount, which typically offers their highest premium reduction.

Note: If you only have two (e.g., House + Contents), you still get a multi-policy discount, but it is lower than the Goldshield tier.

5. Adjust Your Excess to Suit Your Budget MAS allows you to choose higher voluntary excesses on House and Motor policies.

Strategy: If you have an emergency fund, raising your excess (e.g., from $400 to $1,000) can significantly drop your annual premium. Use the Quashed dashboard to weigh up the savings versus the risk.

Final Verdict

MAS is a credible, values-driven option for New Zealanders. Its mutual structure, strong claims support, and community contributions via the MAS Foundation make it a standout insurer. To see if it fits your needs get a tailored MAS quote online and also compare insurance quotes from other providers on Quashed.

Related Quashed Articles

How to Save Money on Your Insurance — Smart strategies to cut your premiums, avoid over‑insuring, and make the most of Market Scan.

Ultimate NZ Guide to Contents Insurance (2025) — A deep dive into how to calculate your contents sum insured, choose excesses, and uncover savings.

Multi‑Policy Discounts on Insurance in NZ: What You Need to Know (2025) — Explains how bundling works, changes to discounts, and how to make sure you're not paying more than you should.