Stop Overpaying: The 2026 Guide to Using Quashed for Cheaper NZ Insurance

Insurance in New Zealand has long been a "grudge purchase." It’s expensive, confusing, and time-consuming.

But with the Quashed Insurance Price Index showing the average cost of house insurance jumping ~50% since 2022 to hit $3,055 per year, "loyalty" has become a luxury most households can no longer afford.

Enter Quashed. We are not just another comparison website; we are your independent insurance headquarters. Now used by over 90,000 Kiwis, Quashed replaces the chaos of paper trails and multiple tabs with a single, intelligent dashboard.

Here is the data-backed case for why you should manage your insurance with Quashed.

1. You Are Likely Overpaying (And We Can Prove It)

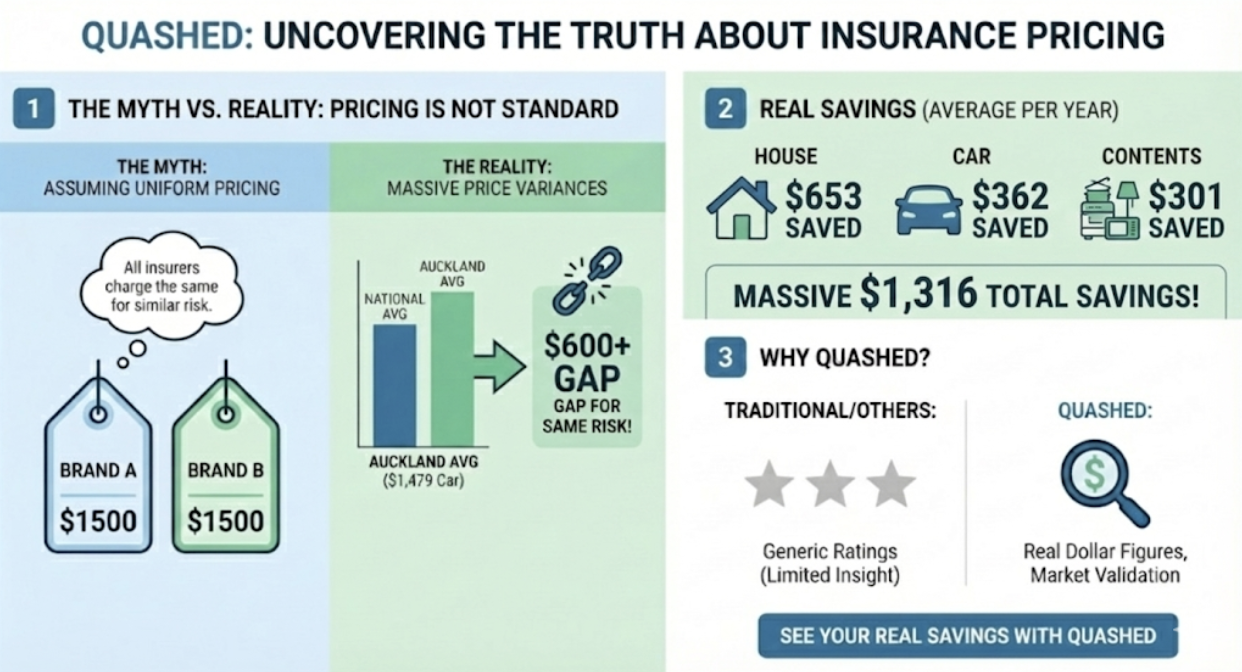

The biggest myth in insurance is that pricing is standard. Many Kiwis assume that if a big brand quotes $1,500, the others will be roughly the same.

The Reality: According to our latest Average Insurance Cost Report, there are massive price variances for the exact same risk depending on your postcode. While the national average for comprehensive car insurance is $1,236, prices in Auckland average $1,479—and the gap between the cheapest and most expensive quotes for the same car often exceeds $600.

The regional pain is even more significant for homeowners. In 2026, Wellington house insurance is often double the cost of Auckland, with average premiums hitting $4,700+ compared to Auckland's $2,100+. By uncovering these location-specific gaps, Quashed users identify average annual savings of $653 on house insurance, $362 on car insurance, and $301 on contents insurance for a massive $1,316 total.

Why Quashed? More Than Just Static Research: While there are many resources available to help Kiwis navigate the insurance market, not all tools are created equal. Unlike traditional research sites or standard brokers, Quashed provides a dynamic, personalised experience.

At a Glance: Research Sites vs. Your Quashed Dashboard

Feature | Research Sites (e.g., Canstar, MoneyHub) | Quashed Independent Headquarters |

Data Type | Static & General: Based on generic personas or "Star Ratings". | Personalised & Live: Based on your actual car, home, and risk profile. |

Effort | Manual: You read articles and then must visit individual sites to get quotes. | Automated: Enter details once to query the market and see real dollar figures. |

Management | None: These are one-off research tools. | Continuous: A live dashboard to track renewals, premiums, and total sum insured. |

Comparison | Limited: Often focuses on a small panel of providers. | Wide-Ranging: Aggregates data from diverse providers, including innovative challenger brands. |

The Quashed Difference: Interactive Empowerment. Most sites offer static content—helpful articles that provide a general idea of the market. Quashed is an interactive technology platform. We don’t just tell you that you could save money; we provide the Market Scan tool to prove exactly how much you can save based on your specific life circumstances.

By moving beyond "Star Ratings" to real dollar figures, we empower you to validate your premiums against the market in minutes.

2. We Compare the "Uncomparable"

The New Zealand insurance market is more concentrated than most Kiwis realise. While there are many brands, two main entities—IAG (owners of State, AMI, NZI) and Suncorp (owners of Vero and joint-venture partner in AA Insurance)—dominate the landscape.

This often leads to "illusionary competition," where you spend hours comparing quotes that ultimately funnel back to the same parent company.

The Quashed Difference: Quashed’s Market Scan breaks down these walls. Our Market Scan technology cuts through the manual chaos by aggregating real-time data from a diverse range of providers. We allow you to instantly compare prices from innovative challenger brands (like Cove, Protecta, and Trade Me Insurance) alongside other market options.

The Rise of Risk-Based Pricing: While IAG and Suncorp dominate the landscape, innovative challenger brands often utilise different risk models. A trending factor in 2026 is Risk-Based Pricing, which explains why many Kiwis are seeing premiums skyrocket even without making a claim. Unlike traditional insurers who might apply broad increases across an entire region, these challenger brands use data to price your specific risk more accurately. Quashed helps you identify which providers are currently offering the best rates for your specific profile rather than following the pricing of the big two.

Crucially, we solve the biggest headache of manual comparison—consistency:

The "Apples-to-Apples" Standard: When you visit individual insurer websites, it is easy to accidentally compare a policy with a $400 excess against one with a $1,000 excess. Quashed standardises these inputs. We present quotes based on a similar excess and sum insured across the board, ensuring the price differences are minimal due to setting differences.

Speed vs. Complexity: Instead of entering your vehicle registration and address five separate times on five separate sites, you enter it once on Quashed. We do the heavy lifting to query the market, presenting you with a clear list of options in seconds.

We don’t play favourites. We give you the access and the data so you can make the decision.

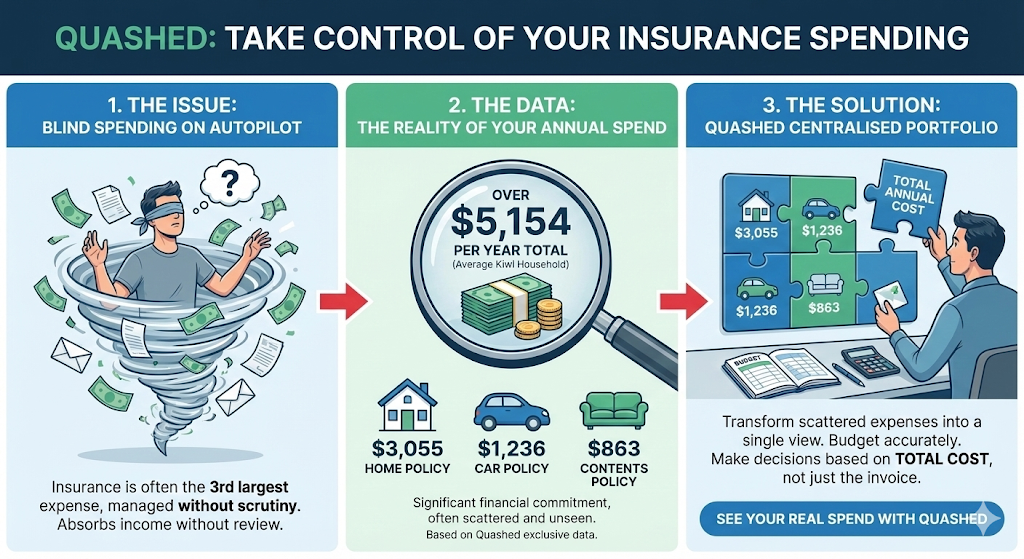

3. Turn Blind Spending into Financial Strategy

For most households, insurance is the third largest expense after tax and housing, yet it is often managed with little scrutiny.

The Data: The average Kiwi household now invests over $5,154 per year to protect their assets—specifically $3,055 on home, $1,236 on car, and $863 on contents policies. Without a centralised view, this significant financial commitment often runs on autopilot, absorbing income without review.

The Solution: Quashed transforms these scattered expenses into a single dashboard showing your number of policies, policy renewal dates, total premiums, and total sum insured. By uploading your policies, you move from "paying bills" to managing a portfolio. You get an immediate, aggregated view of your total risk spend, allowing you to budget accurately and make decisions based on total cost, not just the invoice in front of you.

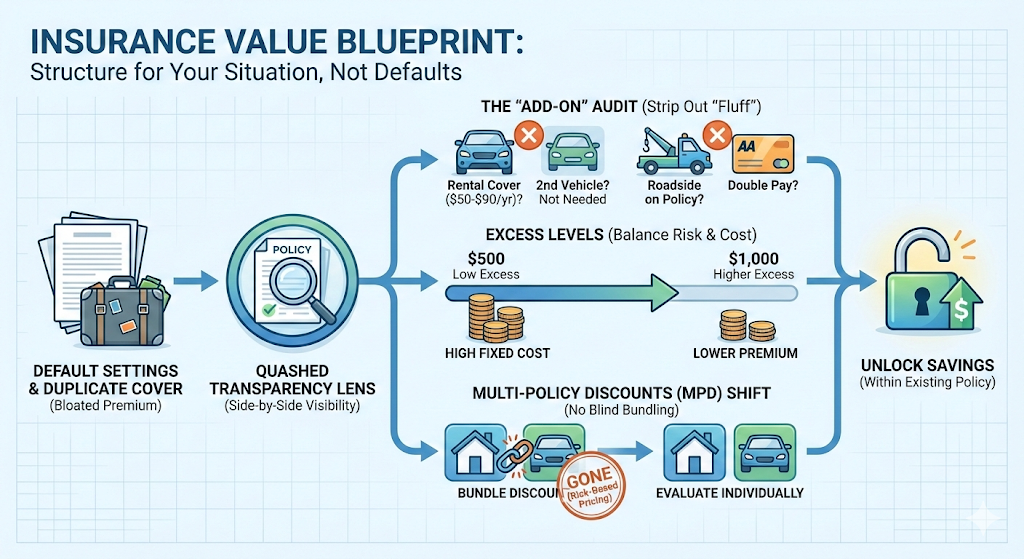

4. Structure Your Policy for Value, Not Just Convenience

Many Kiwis unknowingly pay a premium for default settings or duplicate cover. Policies often include perks which can be helpful, but do not maximise value for your given situation.

The "Add-On" Audit: Do not pay for what you don't need. Comprehensive policies often auto-include Rental Car Cover (approx. $50-$90 /year). If you have a second vehicle in the household, this may not be useful. Similarly, check if you are paying for Roadside Assistance on your policy while holding a separate AA Membership. If you are, you may be paying double for the same rescue.

Excess Levels: Many policies default to a low excess (e.g., $500). Our data shows that increasing this to $1,000 can reduce premiums. You are taking on a small portion of risk in exchange for a lower fixed cost.

The Glass Cover Tip: Many Kiwis don't realise they can often "unbundle" excess-free glass cover from their main policy. If you are willing to take on that specific risk, you can frequently save $100+ per year on your premium.

The Death of Multi-Policy Discounts: Major insurers like State, AMI, Tower Insurance and AA Insurance have moved to remove Multi-Policy Discounts (MPD) as they shift to "risk-based pricing". This means the financial incentive to "bundle" blindly is disappearing.

The Strategy: Quashed brings transparency to these levers. We explicitly list your benefits side-by-side, helping you identify where you are paying for "fluff" or duplicate coverage. This visibility empowers you to strip out unneeded extras to unlock savings within your existing policy.

5. We Are Consumer-First

When you speak to a bank about insurance, they sell you the bank's insurance. When you use a broker, they sell you policies from their specific panel.

The Quashed Promise: Quashed is independent. We are a Kiwi-owned technology company built to serve the consumer, not the underwriter.

Security: We use industry-leading technology, including Auth0 for authentication and Amazon AWS for infrastructure, to ensure your data is safe.

Privacy: We use your data to find you savings, not to spam you.

Cost: It is free for you to create a dashboard, upload policies, and compare prices.

Final Verdict: The Smartest Way to Insure

Most consumers wouldn't manage their bank account with paper statements and a calculator. In 2026, you shouldn't manage your risk portfolio that way either.

The market has shifted—loyalty taxes are real, multi-policy discounts are disappearing, and prices are rising. The "set and forget" approach could be costing you hundreds of dollars a year.

Quashed is the independent digital dashboard that puts you back in control. We replace the clutter of paperwork with a single view of your financial risk, empowering you to shop the market without the administrative headache.

Related Resources

Explore our expert guides to help you maximise your savings and master the 2026 NZ insurance market:

Ultimate NZ Guide to Car Insurance (2025): Compare & Find the Best and Cheapest Cover Don't guess what you should be paying. This guide breaks down exactly how premiums are calculated and includes access to our tools to see the real-time spread of prices for your specific vehicle.

Ultimate NZ Guide to House Insurance (2025): Compare & Find the Best and Cheapest Cover Premiums are rising, but you have options. From adjusting your excess to understanding area-replacement vs. sum-insured, this guide details six actionable steps to reduce your bill.

Multi-Policy Discounts on Insurance in NZ: What You Need to Know in 2025 Is bundling still worth it? With major insurers removing multi-policy discounts, we analyse whether keeping all your eggs in one basket is actually saving you money or costing you more.

Ultimate NZ Guide to Contents Insurance (2025): Compare & Find the Best and Cheapest Cover Whether you are renting or own your home, protecting your belongings is vital. Learn how to calculate the value of your stuff and avoid the common pitfall of under-insurance.

Find Cheaper Car Insurance in NZ (2025): 14 New & Proven Ways to Save Hundreds Price is important, but so is the claim experience. This guide walks you through 14 proven strategies to balance affordability with the reliability of cover you need on NZ roads.

Frequently Asked Questions

1. What is Quashed?

Quashed is an all-in-one insurance platform making it easy for Kiwis to sort out all our insurance in one place. Whether you're exploring insurance, looking to compare and find the best insurance for you, wanting to manage all your existing insurance on one dashboard, or chat to an expert, Quashed can help. We're NZ's first and only platform that does what we do. And, it's free!

2. Is Quashed for me?

YES! If you have insurance, we make it easy for you to stay on top of it. If you are looking to explore or get insurance, we are your one-stop independent online platform that can help you simply and transparently.

3. How do I use Quashed?

Sign up in less than 60 seconds for your secure account. The best way to use Quashed is to start by dropping off (uploading) all your existing insurance policies. It's quick and easy. Our technology picks up your information and creates your new insurance dashboard so you can see what you have, how much you're spending and stay on top of your insurance. From there, hit the magic Market Scan button to find better insurance covers for you.

4. What's Market Scan?

It's our super feature that allows you to compare and find better covers in just a few clicks. You can skip the time and effort it takes to visit multiple different insurance websites to enter the same information and try to compare the benefits by reading all the different policies. Use Market Scan to compare your existing policy to see how it stacks up or find a brand new cover for you.

5. How much can I save on insurance?

It depends on what you currently have. We're mostly finding price differences of roughly $300+ a year on policies. That means if you have a couple of cars, a house and a contents policy, that could all add up to savings of hundreds or even thousands of dollars. Not only that, our customers can easily see the benefits across different policies and providers, and find better covers for them on top of saving money.

6. Do you compare all insurance providers in NZ?

We compare the widest range of insurance providers at Quashed, but not all. There are more than 30+ insurance companies and brands in New Zealand. While our desire is to work with all of them, not all insurance companies are open to being compared. We are constantly working to bring on more insurance companies onto the platform so check back in from time to time for more options.

7. Does it cost more to buy insurance via Quashed?

No. We do not add on any fees nor charges to the prices you see. The price you see on Quashed and end up paying for a policy should be the same when you go directly to the insurers' website. As long as the information used is the same (e.g. sum insured, excess, accident history, age).

8. Is Quashed an insurance adviser or insurance broker?

While we hold a FAP licence, we do not provide advice on any insurance products on the platform. We make information easily accessible and transparent on Quashed which help consumers to make better decisions. We also do not charge any fees which brokers and advisers sometimes charge (which can range anywhere from $50 to $500).

9. Can Quashed find me the cheapest insurance and best insurance policy?

That's our goal. To find and display a wide range of options so you can choose to buy the cheapest and/or the best insurance policy for you. The cost of insurance can vary a lot across insurance companies. For the same car, one insurance company may charge $800 for a comprehensive and another may charge $1,600. Our hope is to make it easy for you to find the cheapest and the best insurance policy in the market.

10. How is this different from my insurance experience today?

Great question. All the things you find difficult about insurance today - we're making them easy! Store all your policy documents in one place, track how much you're spending and how much more you're paying each year, and know when your insurance is expiring/renewing so you stay covered. We'll even see if there are better insurance covers and deals for you.

11. Is my data safe?

Yes. We are a New Zealand company bound by the Privacy Act. We use industry-standard encryption to keep your policy documents and personal details secure.

12. How does Quashed make money if it's free?

We believe in total transparency. Quashed is a free platform for consumers to manage and compare insurance. We do not charge the user fees, whereas traditional brokers or advisers may charge anywhere from $50 to $500. Instead, we are typically paid a commission by the insurance provider if you choose to purchase a policy through our platform. This does not increase your premium; the price you see on Quashed is the same as going directly to the insurer. We remain independent to ensure you see the widest range of market options.