Contents Insurance - Sum Insured & Excess Decoded by Quashed 2025

Buying contents insurance usually feels like a grudge purchase. You reach the quote screen, ready to get it over with, and suddenly you freeze. Two boxes stare back at you: Sum Insured and Excess.

Most Kiwis panic. They guess. They tick the default box just to move on with their day.

Big mistake.

In 2025, with the cost of living and replacement goods higher than ever, guessing is gambling. You are either risking financial ruin if disaster strikes (underinsurance), or you are voluntarily handing over extra cash in premiums every single month that you don't need to pay (overinsurance).

Stop guessing. Quashed is here to fix it. This is your definitive, 5-minute guide to hacking these numbers so you stay protected and keep more money in your pocket.

Part 1: What Is Sum Insured? (And Why You May Be Underinsured)

Your Sum Insured is a critical number in your policy. It is the total maximum amount your insurer will pay if everything you own is destroyed in a single event—think of a house fire, a major flood, or an earthquake.

Many people make the mistake of thinking Contents Insurance only covers "valuables" like jewellery and electronics. They forget the everyday stuff.

The "Upside Down" Test

Think of it this way: If you turned your house upside down and shook it, everything that falls out is generally contents. Example:

Yes: Furniture, clothes, electronics, appliances, rugs, and curtains (sometimes).

No: The walls, the roof, the fixed kitchen bench (that’s House Insurance).

The Hidden Dangers of Underinsurance

Here is the reality check: Most people drastically underestimate the value of their stuff.

You count the TV ($1,500) and the couch ($2,000), but you forget the accumulation of life.

The Wardrobe: The average professional wardrobe (shoes, coats, suits, casual wear) can easily top $10,000 per person.

The Kitchen: Pots, pans, blenders, mixers, cutlery, and crockery often exceed $5,000.

The Linen Cupboard: Towels, sheets, and duvets add up fast.

If your policy covers $50,000, but your life actually costs $80,000 to replace, you are on the hook for the $30,000 difference. In a total loss situation, that is money most people simply don't have.

Part 2: How to Calculate Your Sum Insured Like a Pro

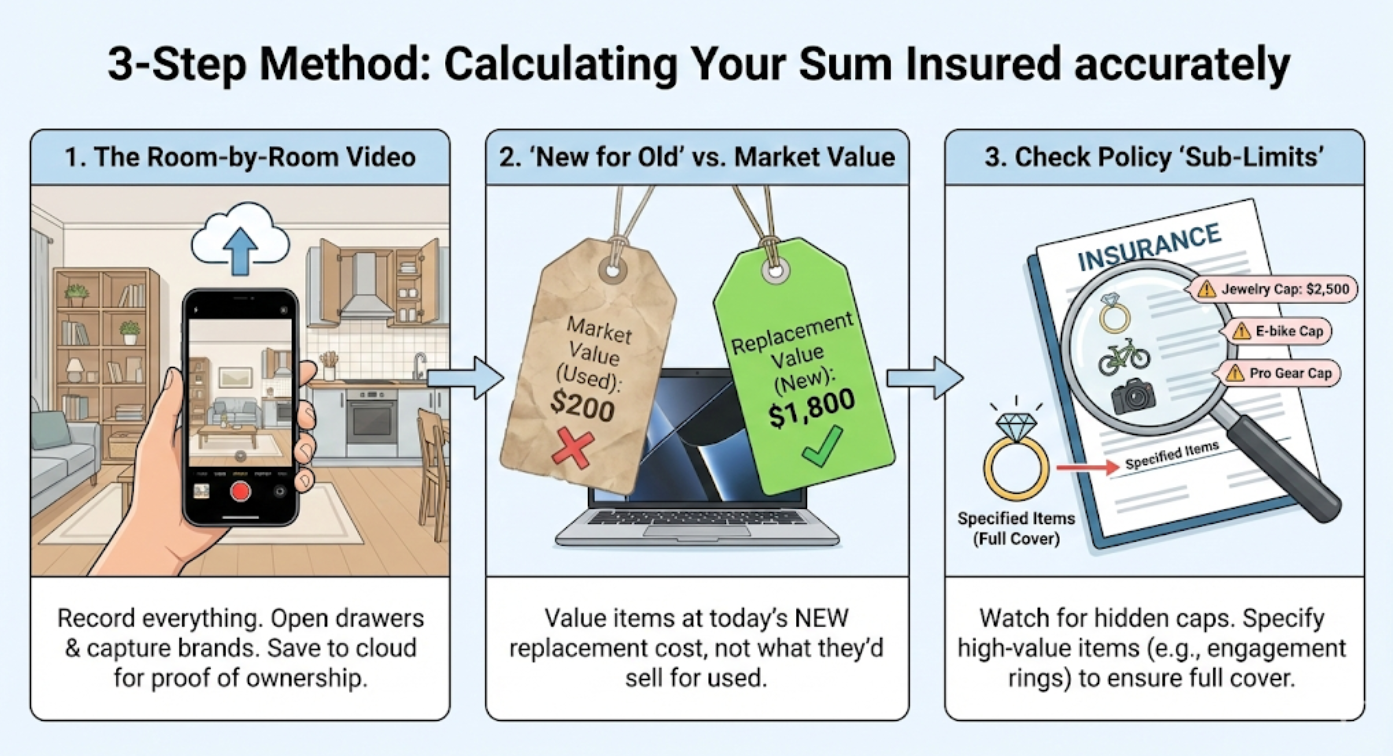

Don't pull a number out of thin air. To get your claim paid without stress, you need accuracy. Here is the 3-step method:

1. The Room-by-Room Video Method

Memory is unreliable during a crisis. Walk through your house today with your phone recording a video.

Open every drawers and cupboards.

Scan the books on the shelf.

Record the brand names of your appliances.

Pro Tip: Save this video to the cloud. It helps you estimate value now, and may serve as proof of ownership if you ever need to claim.

2. Understand "New for Old" vs. Market Value

Most modern policies in NZ are "Replacement" policies (New for Old). This means the insurer buys you a new version of what you lost.

Don't value your 5-year-old laptop at $200 (what you’d get selling it on TradeMe).

Do value it at $1,800 (what it costs to buy the equivalent new model at a store today).

3. Check Policy "Sub-Limits"

This is a classic "gotcha." Most policies have caps on specific categories. If you don't list them, you aren't covered for their full value.

Jewellery: Often capped at $1,500 or $2,500 per item unless specified.

E-bikes: Often capped or require specific lock requirements.

Cameras: Professional gear may need to be listed separately.

If you have a $10,000 engagement ring, you must tell your insurer, or you might only get $2,000 for it.

Part 3: Insurance Excess Explained (The Money Saver)

Your Excess is your "skin in the game." It’s the amount you agree to pay towards a claim before the insurer pays the rest.

Example: You have a $500 excess. Your $2,000 laptop is stolen. You pay $500; the insurer pays $1,500.

This is the easiest lever to pull to save cash on your monthly payments instantly, yet most people ignore it.

The Seesaw Effect

There is a direct correlation between Excess and Premium:

Higher Excess ($1,000+) = Significantly Lower Premiums.

Lower Excess ($250 - $400) = Significantly Higher Premiums.

Which Strategy Fits You?

1. The "Savvy Saver" (High Excess Strategy)

Who: You have a healthy emergency fund ($2k+) sitting in the bank.

Strategy: You bump your excess up to $1,000 or even $2,000.

The Win: Your annual premium might drop by hundreds of dollars. Over 3-5 years without a claim, the savings often exceed the cost of the excess itself. You are essentially "self-insuring" the small stuff to save big on the premium.

2. The "Cash Flow Protector" (Low Excess Strategy)

Who: You budget tightly week-to-week.

Strategy: You keep your excess at $400 or $500.

The Win: You pay more monthly, but if you have a loss next week, you don't need to panic about finding $1,000 instantly. It’s peace of mind for cash flow.

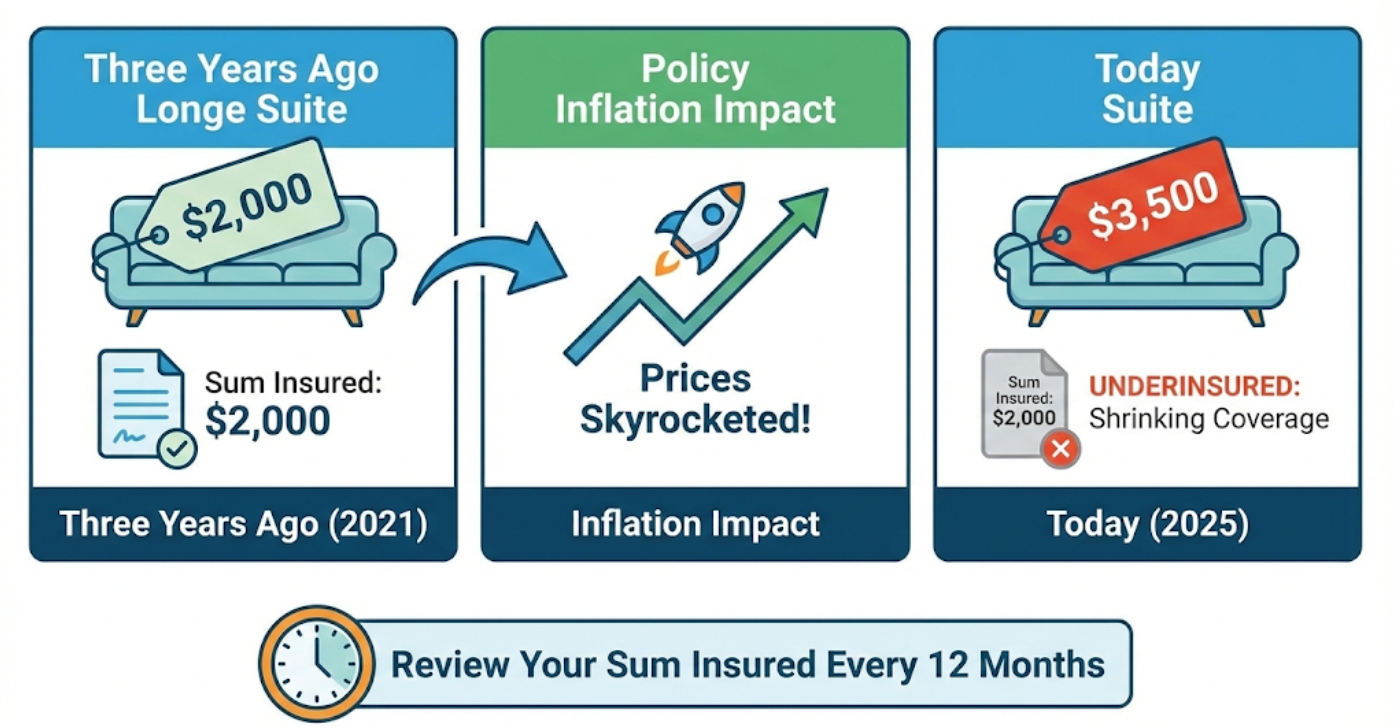

Part 4: The Inflation Trap (Why 2025 is Different)

If you set your Sum Insured three years ago and haven't touched it, it is wrong.

The price of furniture, technology, and imported goods has skyrocketed. A lounge suite that cost $2,000 in 2021 might be $3,500 in 2025. If you haven't adjusted your Sum Insured to match inflation, you are effectively shrinking your coverage every year.

Review this number every 12 months. It can take as little as ten minutes, and it ensures that when you need your insurance, it actually works.

Part 5: Stop Guessing. Market Scan It.

Finding the perfect balance of Sum Insured and Excess used to mean opening twenty tabs, calling call centers, and drowning in PDFs. That’s the old way.

The Quashed way is smarter.

We let you compare policies side-by-side. You can toggle your Excess levels and watch the Premium price change in real-time across different insurers. You can see who offers the best value for your specific Sum Insured.

Don't leave money on the table in 2025.

Run a Quashed Market Scan Today to check your rates, adjust your excess to see the savings, and stop overpaying for cover you don't need.

Need to organize all your policies in one place? Sign up for free at the Quashed Website.

Read More, Save More: Master Your Insurance

You’ve nailed your Contents cover, but don't stop there. Most Kiwis are overpaying on at least one of their insurance policies. Dive into these expert guides to tighten up the rest of your financial world.

Comparing Insurance in New Zealand Are your carpets "house" or "contents"? What about your curtains? Avoid the expensive "double-up" trap and ensure your home's structure is covered correctly.

Find Cheaper Car Insurance in NZ (2025): 14 New & Proven Ways to Save Hundreds Car insurance premiums are rising fast. Find out why staying loyal to your insurer is costing you hundreds and how to find a better deal in under 5 minutes.

How to Set Your Sum Insured for Contents Insurance Got expensive toys or jewellery? Learn how to calculate replacement costs accurately so you aren't left heartbroken (and broke) after a theft.

Is Contents Insurance Worth It for Renters? Think you don't need insurance because you don't own the house? Think again. Learn about protecting your tech and the crucial importance of "renters' liability."

Ready to see all your insurance in one place? Sign up to Quashed for free and take control today.

Disclaimer: This article provides general information only and does not constitute financial advice. Policy terms, benefits, and savings vary by provider. Always read the specific policy wording before making a purchase decision.