Getting the Best Deal? Read this Contents Insurance Comparison Guide by Quashed (2025)

How much would it cost to replace everything you own? For the average Kiwi household, the replacement value of contents is often $70,000 or more.

With increasing global reinsurance costs and rising theft and natural disaster claims in New Zealand, contents insurance premiums have soared in recent years. If you haven't shopped around for your policy lately, you are likely overpaying.

This comprehensive guide breaks down everything you need to know to save on your contents insurance. We’ll show you how premiums are calculated, the key differences between cover types, and how to find significant savings without compromising the value of your possessions.

Don't pay more than you need to! Compare free, no-obligation quotes from New Zealand's leading contents insurers in minutes on Quashed and see how much you could save. Compare & Save Now!

The Real Cost of Contents Insurance in NZ (2025)

Based on the latest data from Q2 2025, the national average cost of Contents Insurance across New Zealand is $863 a year or approximately $72 a month.

Source: Data based on a Quashed Market Scan Example from the Quashed Index data, illustrating premium savings for specific Sum Insured and Excess combinations.

*Actual costs will vary depending on the insurer, policy coverage, sum insured levels, and location.

The average cost of contents insurance in New Zealand has significantly increased, making it more important than ever to check your property's specific risk profile using the Natural Hazards Portal and compare your options now.

How is my Premium Actually Calculated? How do I Get the Best Deal?

The best way to find the cheapest price for you is to use a comparison tool like Quashed’s market scan to compare multiple providers based on your specific profile.

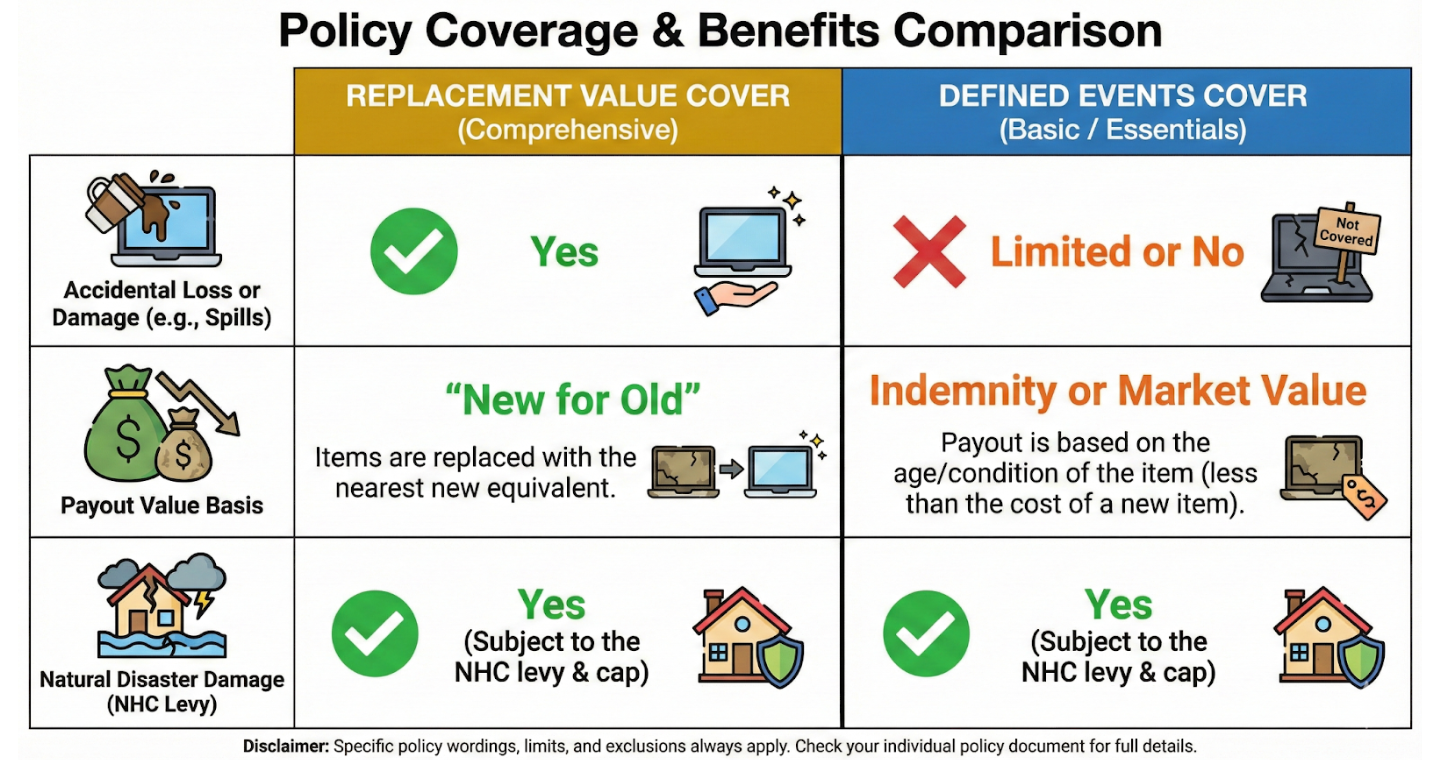

Decoding Cover Types

Choosing the right type of policy is your first major decision.

Replacement Value Cover: Guarantees you can replace a destroyed or stolen item with a brand new one. This is the recommended standard.

Defined Events Cover (Often called "Basic" or "Essentials"): A cheaper, limited option that typically pays Indemnity Value (market value/second-hand worth) rather than the replacement cost. This is only recommended if you are on a strict budget, as the payout may not be enough to buy new items.

Your Sum Insured & Excess, What Gives?

These two levers have the biggest impact on your premium.

Sum Insured: The maximum amount the insurer will pay. This should be calculated based on the cost to replace everything you own. Insurers such as MAS Insurance offer content calculator tools to provide a quick estimate.

Excess: The amount you agree to cover first when you make a claim.

Key Takeaways:

A higher excess will lower your premium: Increasing your excess from $250 to $1,000 can save you 30% or more, but ensure you can afford the higher upfront payment.

Do not lower your sum insured to save money: Lowering it below replacement value leaves you underinsured and financially exposed if a total loss occurs.

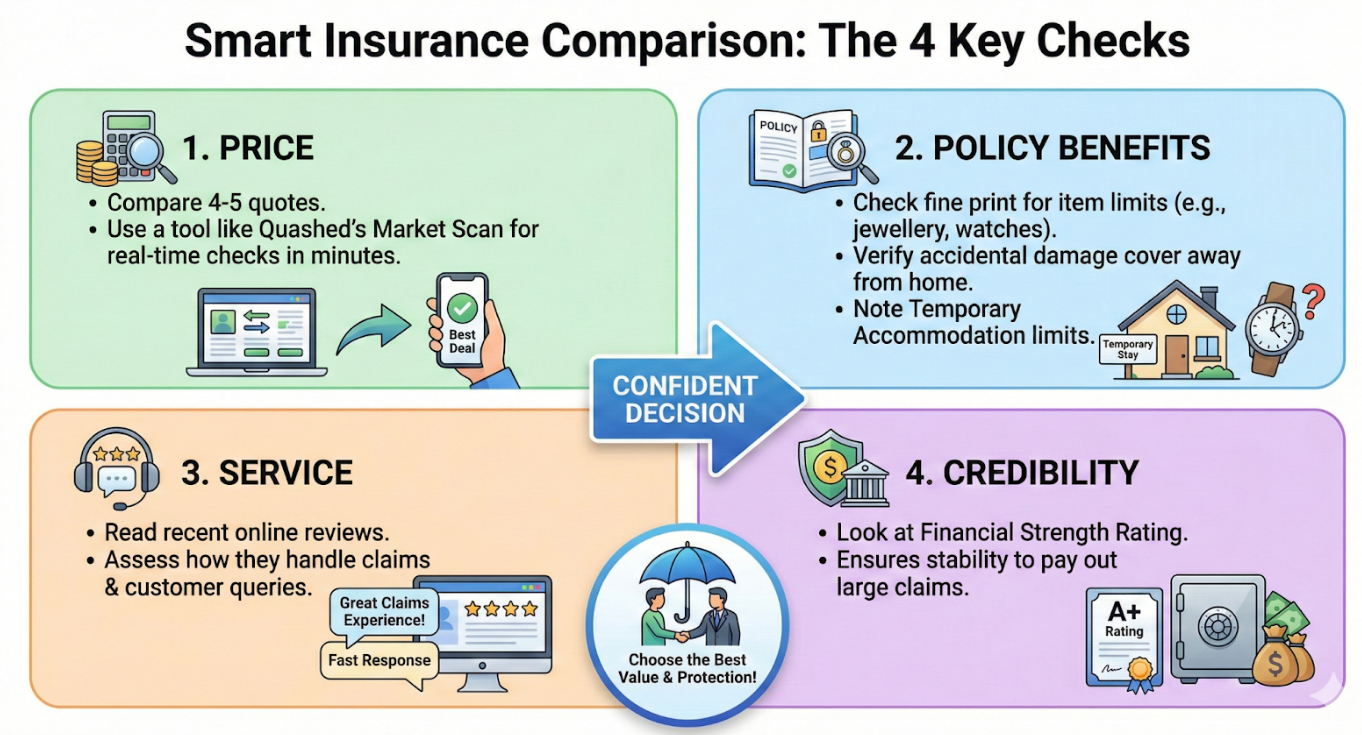

Value for Money - Checklist

Now that you understand the basics, use this framework to compare policies effectively:

Price: Compare quotes from at least 4-5 different providers. Use a tool like Quashed’s Market Scan to check real-time quotes in minutes.

Policy Benefits: Check the fine print for limits on specific items (like jewellery and watches), accidental damage cover away from home, and the limit on Temporary Accommodation.

Service: Read recent online reviews to see how the insurer handles claims and customer queries.

Credibility: Look at the insurer's Financial Strength Rating. This ensures they have the capital and financial stability to pay out large claims.

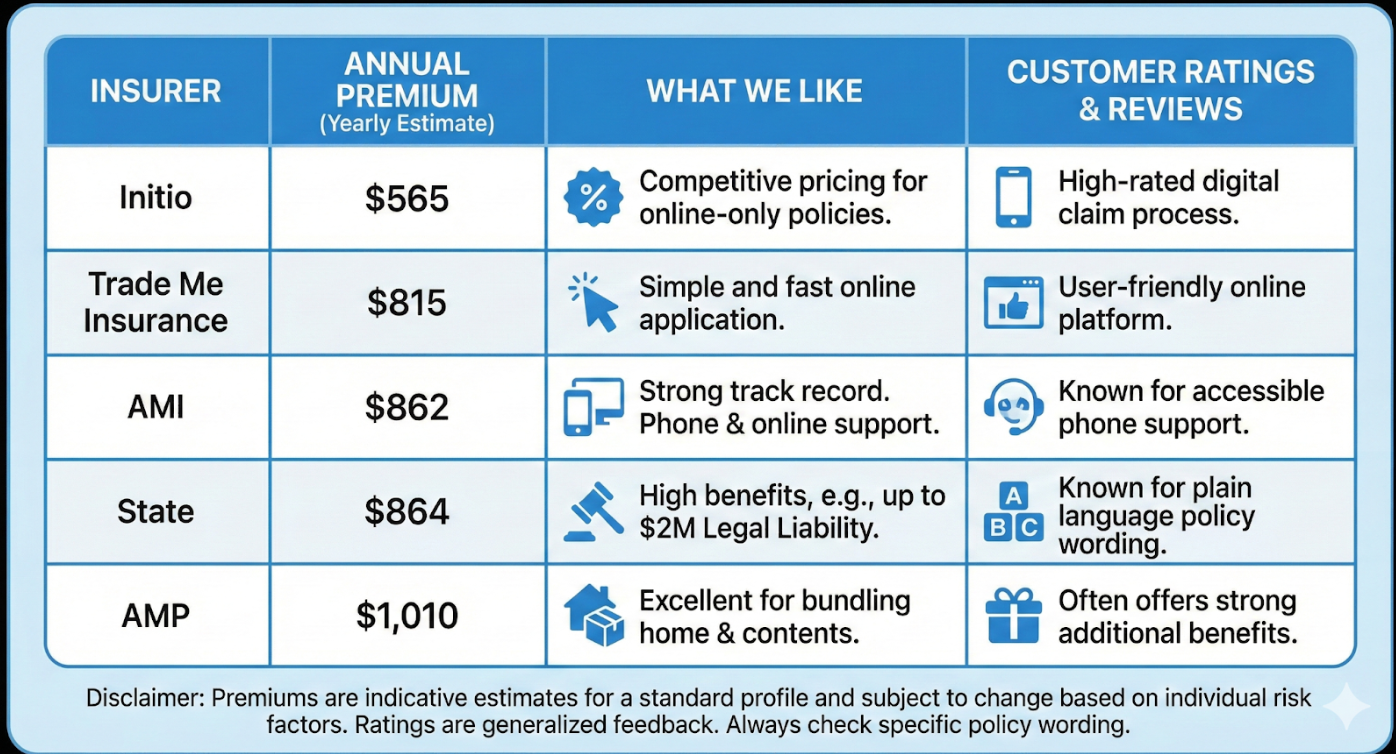

Insurance Providers Compared (2025)

Here is a look at how premiums can vary between some of the major and alternative providers in the NZ market for the same level of contents cover (Example: $100,000 Sum Insured, $1,000 Excess, located in Whakatāne):

Source: Data based on a Quashed Market Scan Example for a specific $100k Sum Insured profile, illustrating price variation across providers.

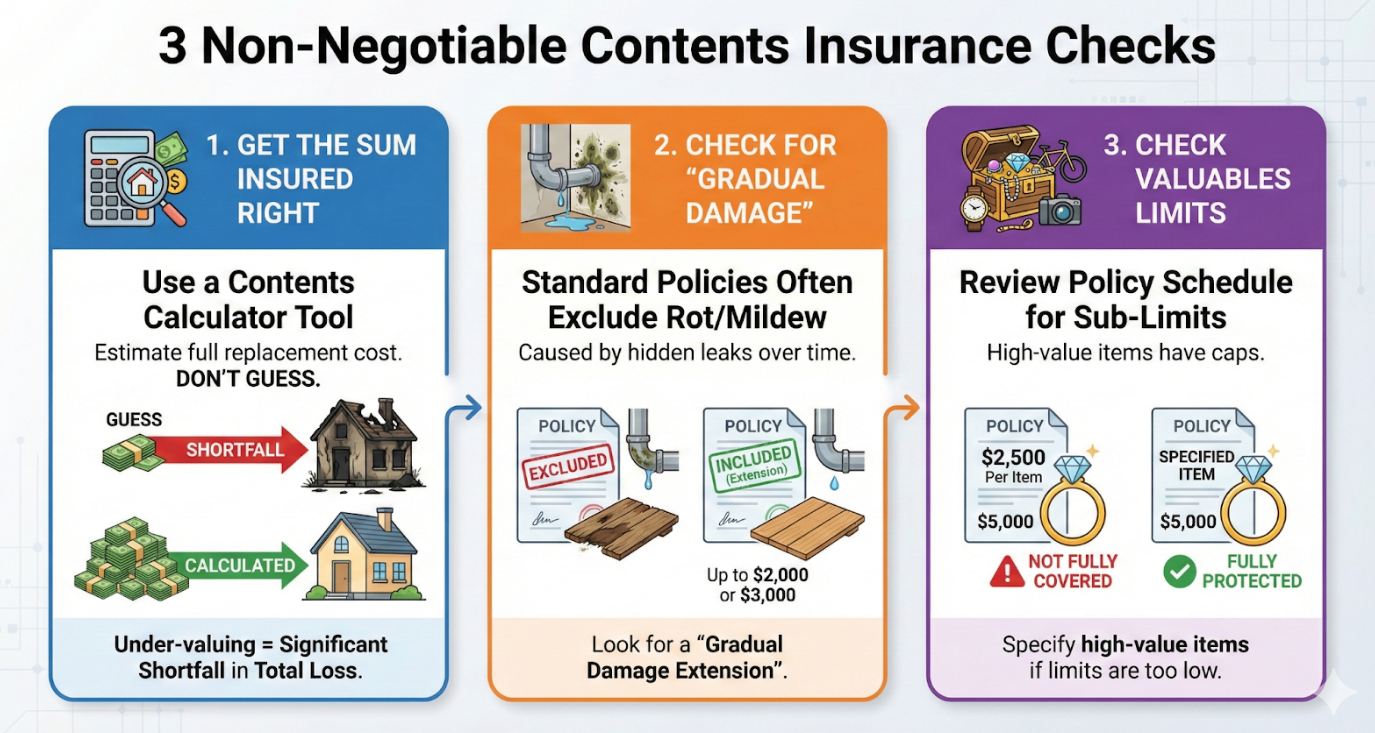

Hot Tips

When you are ready to purchase or review your contents insurance, simplify the process by focusing on the three non-negotiable checks that determine whether your policy will pay out correctly:

Get the Sum Insured Right: Use a Contents Calculator Tool to estimate the full replacement cost of your belongings. Don't guess. Under-valuing is the most common mistake and can lead to a significant shortfall if you suffer a total loss.

Check for "Gradual Damage": Standard policies often exclude rot or mildew caused by hidden leaking pipes. Look for a policy that includes a "Gradual Damage Extension" (usually up to $2,000 or $3,000) to cover you for leaks you couldn't see.

Check Valuables Limits: Review the policy schedule for sub-limits on high-value items like jewellery, watches, bikes, and collections. If the limits are too low (e.g., $2,500 per item), you must specify these items to ensure they are fully protected.

Related Reading

The Average Cost of Car, House, and Contents Insurance in New Zealand

Ultimate NZ Guide to House Insurance (2025): Compare & Find the Best and Cheapest Cover

Canstar vs Quashed: Which Platform Helps Kiwis Save More on Contents Insurance in 2025?

Disclaimer: This article provides general information only and does not constitute financial advice. Policy terms, benefits, and savings vary by provider. Always read the specific policy wording before making a purchase decision.