Towing Your Boat or Caravan in NZ: Does Your Policy Cover the Trailer? (2026 Quashed Deep Dive)

Summer in Aotearoa isn't complete without a road trip. Whether you are hauling a caravan to a Top 10 Holiday Park in Taupō, towing the tinny to the Coromandel for the morning bite, or dragging a trailer load of green waste to the tip, towing is a national pastime.

However, a common misunderstanding plays out on our roads every holiday season. A driver might damage their trailer or caravan in an accident, call their insurer confident in their car policy, and discover that while their vehicle is protected, the item being towed has very limited cover.

It is a frequent—and expensive—insurance surprise in New Zealand.

At Quashed, we believe you should pay for cover, not assumptions. Many owners unknowingly face significant financial risk the moment they hook up their trailer.

This guide clarifies exactly where your car insurance stops and where your financial risk begins when towing.

Step 1. The "Liability" vs "Damage" Gap

The Issue

Most Kiwis assume that because their car is fully insured, anything attached to it is fully insured too. They believe their "Full Cover" extends seamlessly to the towball and everything behind it.

The Reality

Standard comprehensive car insurance policies in New Zealand typically cover Liability for the trailer, but often exclude or strictly limit Own Damage coverage for the trailer itself.

Scenario A (Liability - Usually Covered): You merge lanes on State Highway 1 and your caravan sideswipes a parked ute. Your car policy will generally pay for the damage to the other vehicle (the ute). This protects you from being held liable for the repairs to the third party.

Scenario B (Own Damage - Usually Limited): You reverse into a bollard at the boat ramp, smashing the hull of your boat and snapping the trailer axle. Your car policy will likely pay zero for the boat and very little for the trailer itself.

The Lesson

Do not confuse protecting other people with protecting your assets. Liability cover stops you from facing a large bill if you hit someone else, but it won't help you replace your own boat. If you want your boat or caravan fixed after a crash, a standard car policy is rarely enough.

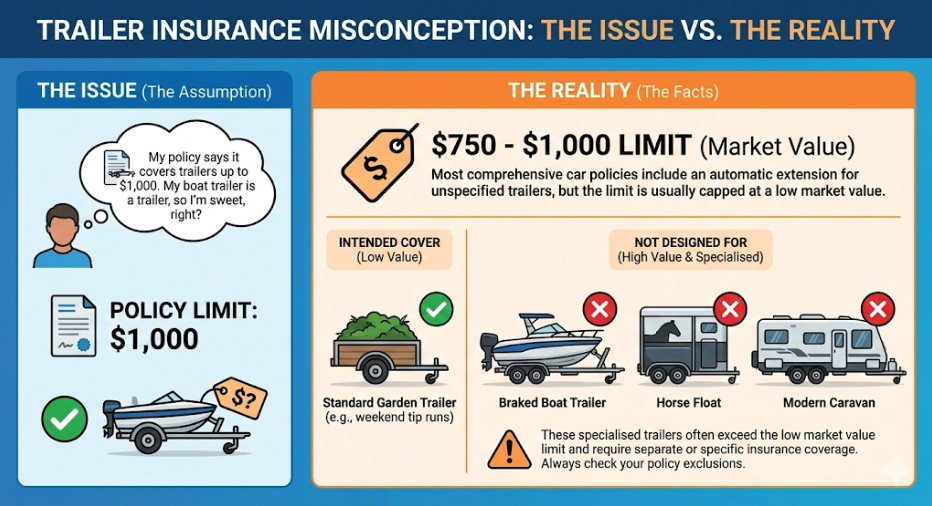

Step 2. The $1,000 Limit (The Garden Trailer Rule)

The Issue

"My policy says it covers trailers up to $1,000. My boat trailer is a trailer, so I’m sweet, right?" This is a risky assumption for towing enthusiasts.

The Reality

Most comprehensive car policies include an automatic extension for unspecified trailers, but the limit is usually capped at a low market value, often around $750 or $1,000.

This coverage is designed for a standard garden trailer you use for weekend runs to the tip. It is not designed for:

A braked boat trailer.

A horse float.

A modern caravan.

The numbers

If you write off a $60,000 caravan and rely strictly on your car insurance’s built in trailer coverage, you could be left with a payout of just $1,000. That leaves you with a $59,000 shortfall and no holiday home on wheels.

The Lesson

Check your policy wording for the "Trailer Limit". If your trailer is worth more than this limit (which it almost certainly is), you need a separate policy.Check comprehensive car coverage limitations using the Quashed market scan today.

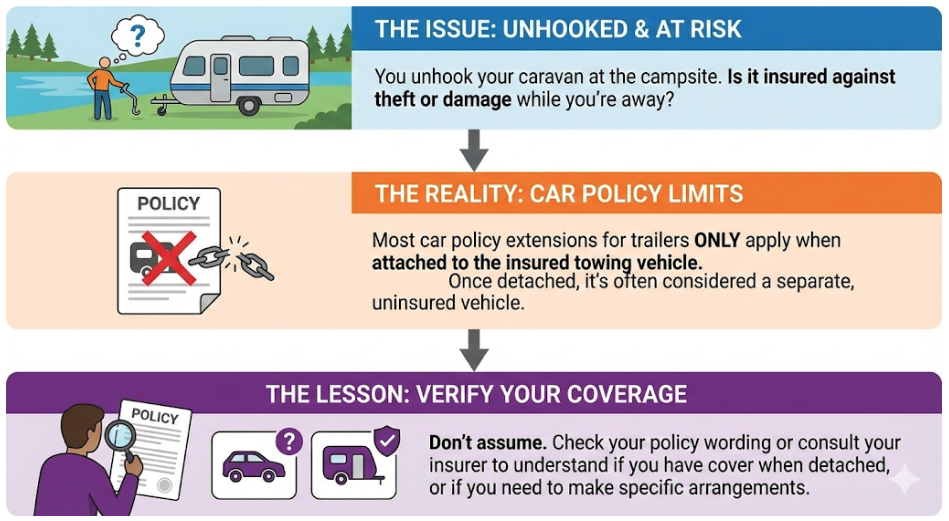

Step 3. The "Uncoupled" Risk (Campground Theft)

The Issue

You arrive at the campsite, unhook the boat trailer, and drive into town for supplies. While you are gone, the trailer is stolen.

The Reality

Many car insurance extensions for trailers apply only while the trailer is attached to the insured vehicle.

Once you unhook that trailer, it is often legally considered a separate, uninsured vehicle. If it rolls into a river, gets damaged by a storm, or is stolen while detached, your car policy generally provides zero protection.

The Lesson

You may need a standalone policy for caravans and boat trailers that covers them anywhere in New Zealand, whether they are being towed, parked in your driveway, or sitting detached at a campsite.

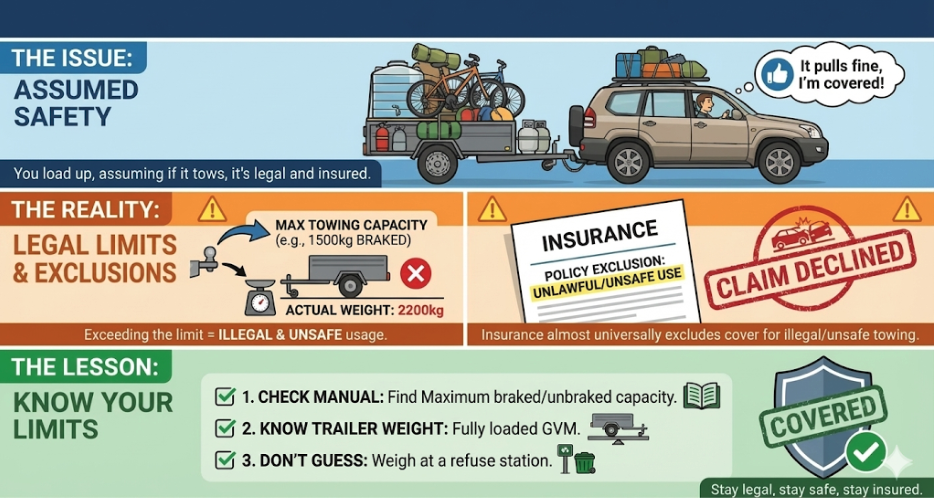

Step 4. The "Weight Check" (GVM & Towing Capacity)

The Issue

You load up the trailer with water, bikes, BBQ gas bottles, and camping gear. It’s heavy, but the vehicle can pull it, so you assume you are covered.

The Reality

Every vehicle has a Maximum Towing Capacity (braked and unbraked). If you exceed this limit, you are operating the vehicle outside of its legal specifications.

Insurance policies almost universally exclude cover if the vehicle is being used in an "illegal or unsafe manner". If an accident occurs and the assessor finds your caravan was over your car's towing limit, your claim could be declined.

The Lesson

Check your vehicle's manual for its towing capacity and know the fully loaded weight of your trailer. Don't guess—weigh it at a refuse station if you aren't sure

Step 5. The Contents Exposure (What's Inside Matters)

The Issue

You load up the trailer for a weekend job or trip—tools, fishing gear, camping equipment, or expensive electronics. You lock the trailer, hitch it to your insured car, and assume everything inside is covered if it gets stolen.

The Reality

Your car insurance does not cover the contents inside your trailer. It only covers the vehicle itself.

If your trailer is broken into or stolen while attached to your car, your car policy generally pays $0 for the items inside.

Home Contents Extension: You typically have to rely on your Home Contents policy for these items under a "temporarily removed from home" clause.

The "Forced Entry" Requirement: Insurers often have a strict rule: if there's no sign of a break-in—like a smashed lock or broken window—they won't pay out. Theft from an open tent usually doesn't count. If the trailer was left unlocked or the tarp was just untied, you likely have no cover.

Business Tools: Your personal contents policy typically covers work tools, but caps the payout (often at $1,500 – $3,000). If your trailer holds $10,000 of gear, you are significantly underinsured.

The Lesson: Never leave expensive gear in a trailer overnight unless you have confirmed your Home Contents policy covers it. If you carry work tools, check if your business liability or tools policy extends to items in transit. Check contents policies and what they cover using Quashed’s market scan today.

Step 6. The "WOF & Rego" Clause

The Issue

It is easy to let the WOF (Warrant of Fitness) or Rego on a trailer lapse, especially if it sits on the front lawn for 11 months of the year.

The Reality

Insurance policies require your vehicle and anything it tows to be in a roadworthy condition.

If you have an accident and the assessor discovers your trailer had bald tyres, a rusted coupling, or no current WOF, they can decline your claim—even if you have a specific trailer policy.

The Lesson

Before you hook up this summer, check the trailer lights, tyres, and WOF. An administrative oversight could cost you thousands in a declined claim.

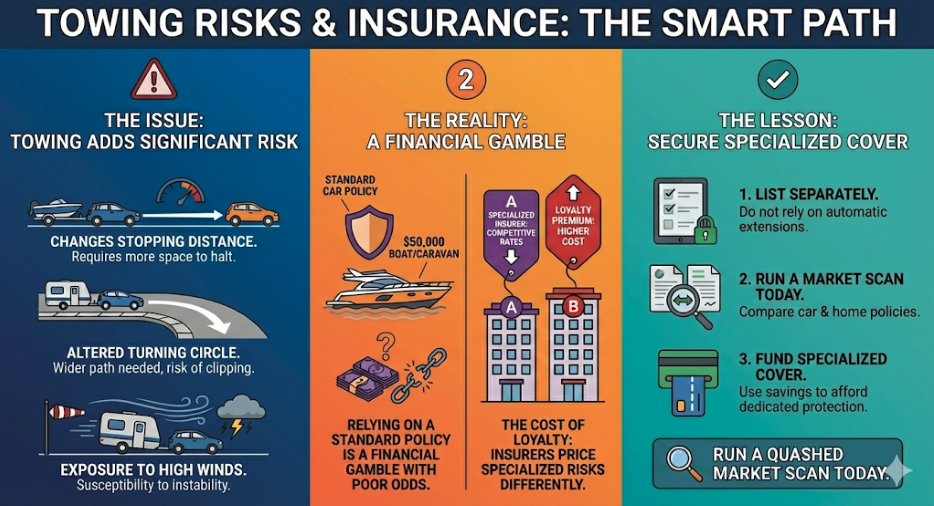

Final Verdict: Don't Tow Uninsured

The Issue

Towing adds significant risk to your drive. It changes your stopping distance, your turning circle, and your exposure to high winds.

The Reality

Relying on a standard car policy to protect a $50,000 boat or caravan is a financial gamble with poor odds.

The cost of loyalty applies here too—insurers price specialized risks differently. One provider might offer excellent caravan rates while another charges a massive premium.

The Lesson

List your boat or caravan as a separate item. Do not rely on automatic extensions. Run a Quashed Market Scan today to compare your car and home policies—the savings you find on your main insurance can help fund the specialised cover your toys need.

Related Reading

Keep your summer adventures safe and your premiums low with these related guides from the Quashed team:

Ultimate NZ Guide to Car Insurance (2025): Compare & Find the Best and Cheapest Cover This comprehensive guide breaks down everything you need to know to save on your car insurance, including how premiums are calculated and what to look for in a policy.

Comparing Insurance Costs for the Most Popular Cars in NZ Towing with a Hilux or Ranger? See how different makes and models compare when it comes to insurance costs and risks.

How to Compare Car Insurance in NZ and Find the Best Deal We explain the factors that influence your premium—like location and age—and how to shortlist the best options for your vehicle.

Getting the Best Deal? Read this Contents Insurance Comparison Guide by Quashed (2025) Ensure the gear inside your caravan is protected. This guide covers "temporarily removed" items and the limits you need to watch for.

Key Considerations with Car Insurance We bust common myths (like "My car insurance covers everything I tow") and explain why self-insurance is a risky gamble.

Multi-Policy Discounts on Insurance in NZ: What You Need to Know in 2025 Find out if bundling your car, house, and boat insurance is actually saving you money, or if recent industry changes mean you should split your policies.

Frequently Asked Questions: Towing Insurance

1. Does my car insurance cover my boat trailer?

Only if it's worth less than $1,000. Most policies cover damage you cause to other cars, but won't pay to replace your own boat or trailer if you crash. You typically need a standalone marine policy.

2. I have a 15-year-old caravan. Can I just use the trailer extension?

Only if the caravan is worth less than the limit stated in your policy (usually $750 - $1,000). If it's worth more, you are essentially self-insuring the difference.

3. Can my claim be declined if I overload my trailer?

Yes. Standard insurance policies explicitly exclude cover if you are towing a weight that exceeds your vehicle's manufacturer specifications (its "towing capacity").

If you tow a heavy boat or caravan that pushes your car beyond its rated Gross Combination Mass (GCM)—or if you tow an unbraked trailer heavier than 750kg when your car isn't rated for it—your insurer can decline your claim for both the car and the trailer, even if the weight didn't cause the crash.

4. What happens if my trailer isn't WOF'd?

If the lack of roadworthiness contributed to the accident (e.g., failed brakes, rusted coupling, or bald tyres), your insurer can legally decline the claim. Always check your WOF before a trip.

5. Are the belongings inside my caravan covered?

Generally, no. Standard caravan or trailer insurance policies cover the structure and permanent fittings (like a built-in fridge or stove). They explicitly exclude loose personal items like clothing, bedding, electronics, and fishing gear.

These items typically fall under your Contents Insurance policy (often under a "contents temporarily removed" clause). However, you must check your limit—coverage for items away from home is often capped at a low amount (e.g., $3,000 total), which may not cover a fully packed family caravan.

6. Does my insurance cover me if I exceed the towing weight limit?

No. If you are towing a load heavier than your vehicle's rated towing capacity (braked or unbraked), you are breaking the terms of your policy (unsafe usage). This is a common reason for declined claims. Always check your vehicle's manual and the towbar rating.