Car Registration in NZ: A Guide to Licensing Costs and Insurance Requirements

Car ownership in New Zealand comes with a stack of ongoing obligations—and costs that catch many drivers off guard. Rego renewals, Warrant of Fitness checks, ACC levies, road user charges, and car insurance premiums all add up. But here’s what most Kiwi drivers don’t realise: these costs are closely intertwined. Let one lapse, and you could find yourself uninsured, fined, or both.

From January 2026, vehicle licensing (rego) fees increased again—the second staged increase in as many years—adding further pressure to household budgets already squeezed by rising insurance premiums. Our data at Quashed shows the average New Zealand driver is now paying $1,298 per year for car insurance alone, while rego and WoF costs add hundreds more annually.

Drivers who compare car insurance providers save an average of $367 per year—for identical coverage. This guide breaks down what you’ll pay, what’s legally required, and exactly how to stop overpaying.

Step 1. Understand Rego Costs—What You’re Actually Paying For

Many drivers treat rego renewal as a fixed, unavoidable cost and barely glance at the amount before paying. In reality, rego fees vary by vehicle type, fuel type, and duration—and they’ve just gone up again.

The Data:

Vehicle licensing fees in New Zealand are set by Waka Kotahi NZ Transport Agency and include an ACC levy, an annual licence fee, and an administration fee. The annual licence fee portion had not increased since 1994 until the Government introduced staged increases—first from January 2025, then again from January 2026. These increases added $25 per year for most standard vehicles each time, meaning the annual cost of rego has risen by around $50 for the majority of drivers since 2024.

As noted by 1News reporting on the January 2026 changes, the 12-month licence for a standard petrol private passenger vehicle rose from approximately $144 to approximately $173 per year. For all vehicles, fuel types, and renewal durations, fees can be confirmed via the NZTA Rightcar fee checker (reccomended) - components vary per vehicle. For quick reference, you can also check the NZTA Common licensing fees table.

Key points to understand:

Paying for 12 months upfront saves approximately 20% compared to quarterly renewals.

Motorcycles, mopeds, and commercial vehicles have different fee schedules — check the NZTA website for specifics.

The Lesson:

Rego costs are no longer the minor, static expense they once were. The 2025 and 2026 annual licence fee increases—$25 each time—have meaningfully raised the baseline cost for every registered vehicle in New Zealand. Diesel owners face a further financial consideration: road user charges (RUC) are paid separately, on top of rego. Use the NZTA Rightcar tool to calculate your complete annual licensing cost before buying a vehicle.

The Action:

Use the NZTA Rightcar tool to check your vehicle’s exact rego fee before renewal. Consider paying for 12 months upfront where cash flow allows—the savings are real. And set a calendar reminder so you never let your rego lapse. A $200 fine from police or parking wardens is a steep price for an oversight.

Step 2. Your WoF and Why It’s Critical to Your Insurance Policy

The Warrant of Fitness (WoF) is an inspection that confirms your vehicle is safe to drive on New Zealand roads. Most drivers know it’s a legal requirement—but far fewer realise that an expired WoF can directly affect their ability to make a car insurance claim.

The Data:

WoF requirements in New Zealand depend on vehicle age:

Vehicles first registered after 1 January 2000: WoF required annually.

Vehicles first registered before 1 January 2000: WoF required every six months.

Brand new vehicles: WoF valid for three years from first registration.

The cost of a WoF typically ranges between $40 and $100. As a benchmark, AA charges $76 for members and $85 for non-members, with VTNZ similarly priced. Some providers, such as Tony's Tyre, offer inspections from $39. For more, see our Guide to Car Ownership in New Zealand.

Here is the critical point that many drivers miss: not having a valid WoF or rego at the time of an incident can give your insurer grounds to decline your claim. Under the Insurance Law Reform Act 1977, insurers cannot automatically deny a claim solely because a WoF has lapsed—but they can and do deny claims when the vehicle’s condition contributed to the accident. If your bald tyres (which would have failed a WoF) caused you to skid, or your faulty brakes contributed to a collision, your claim could be rejected entirely.

The Lesson:

A lapsed WoF creates a grey zone that insurers can use against you. Even if your car is fundamentally safe, an expired WoF gives the insurer an investigation trigger—delaying your payout and adding stress at an already difficult time. The risk isn't just legal (a $200 fine); it's financial. Your $1,298 average annual insurance premium offers you no protection if a claim is denied due to vehicle compliance issues.

As Quashed explains in our guide to debunking car insurance myths: if the expired WoF means your car was unsafe, you could run into serious issues when claiming. Keeping your WoF current isn’t just about avoiding a fine—it’s about keeping your insurance valid.

The Action:

Treat your WoF expiry date with the same urgency as your rego. Set reminders using the NZTA Waka Kotahi app, which will notify you before both your WoF and rego expire. If your car fails a WoF, do not drive it until defects are repaired—driving an unroadworthy vehicle voids legal protections. And when shopping for a WoF, compare prices: the cheapest certified inspection provides exactly the same legal protection as the most expensive one.

Step 3. Car Insurance—The Hidden Cost Drivers Consistently Underestimate

Car insurance is not legally compulsory in New Zealand, but with over 90% of Kiwi drivers holding some form of cover, it is effectively a social norm—and for good reason. Without it, a single at-fault accident can result in repair bills running into tens of thousands of dollars with no protection.

The Data:

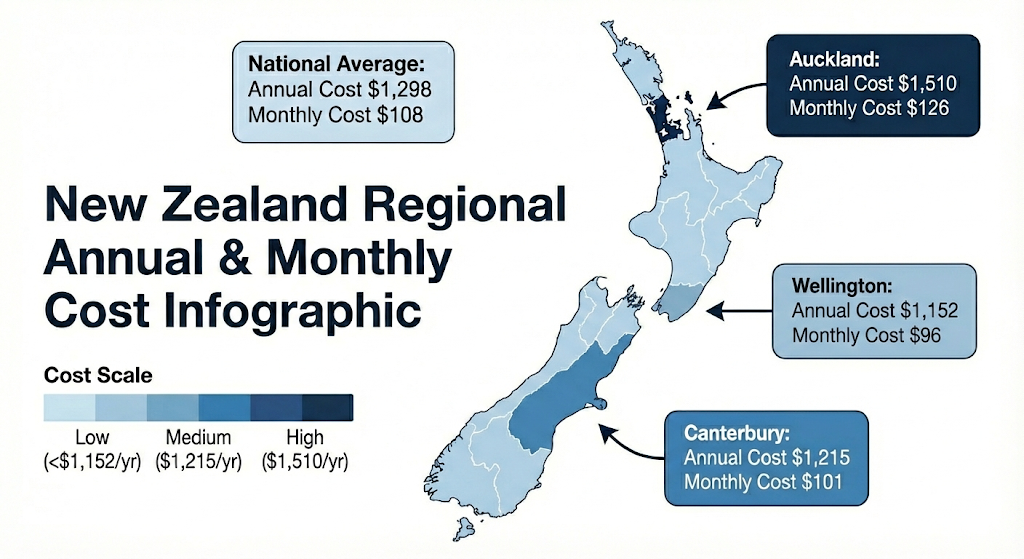

Based on Q4 2025 Quashed Index data, the average annual comprehensive car insurance cost in New Zealand is $1,298 per year ($108 per month). But regional and individual variation is significant:

Region | Annual Cost | Monthly Cost |

National | $1,298 | $108 |

Auckland | $1,510 | $126 |

Canterbury | $1,215 | $101 |

Wellington | $1,152 | $96 |

Factors that drive your specific premium higher or lower include your age and driving history, the make, model, and age of your vehicle, your location and where the car is parked overnight, your agreed value or market value sum insured, and your chosen excess amount.

Car insurance premiums in New Zealand have also been rising. Like home insurance, increased reinsurance costs, natural hazard events, and vehicle repair inflation have all contributed to higher premiums across the board.

The Lesson:

Car insurance is not one-size-fits-all, and the premium you’re quoted reflects a complex risk assessment unique to your profile. Two drivers with identical cars in the same suburb might receive wildly different quotes from the same insurer—and very different relative pricing from different insurers. This is why comparison is essential.

Your excess choice also matters. Increasing your excess from $500 to $1,000 can reduce your premium by 10–15%. For a driver paying $1,298 annually, that could mean $130–$195 in savings per year—though it means higher out-of-pocket costs if you do claim.

The Action:

Run a Quashed Market Scan to understand what a competitive premium looks like for your profile. Enter your details once and compare quotes from multiple insurers on identical coverage terms. Don’t make decisions based on your renewal notice alone—that figure does not represent the market.

For a deeper look at what your policy actually covers and the common exclusions to watch for, read our guide to debunking car insurance myths.

Step 4. Compare Providers—The Loyalty Tax Is Costing Kiwi Drivers Hundreds

If you’ve been with the same car insurer for more than a year without comparing quotes, you may be overpaying.

The Data:

According to Q4 2025 Quashed Market Scan data, 80% of drivers who compared car insurance found a cheaper policy, with average savings of $367 per year. The average difference between the highest and lowest quotes for equivalent coverage across insurers on the Quashed platform was $679 in Q1 2025.

The "loyalty tax" across car, house, and contents insurance combined averages $1,351 per year. For car insurance alone, that's $367 left on the table annually by drivers who accept their renewal notice without shopping around.

Multi-policy discounts—once a reason to bundle all policies with one insurer—have also been officially discontinued by major providers including AA Insurance, AMI, State, Tower, and Vero following regulatory action. The incentive to stay loyal has largely disappeared, making comparison even more critical.

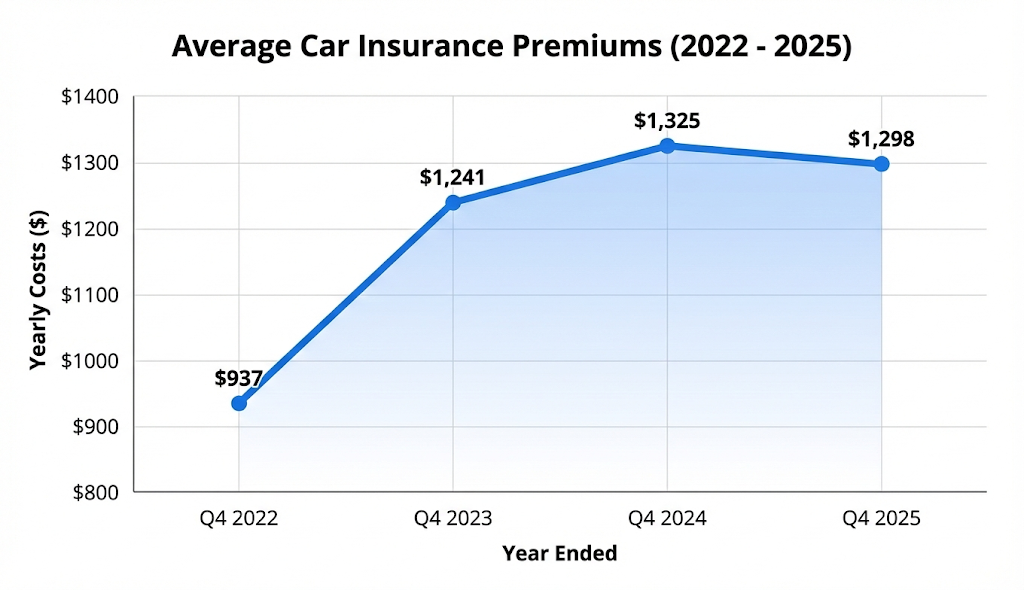

Year (Q4) | Average Annual Car Insurance Premium | YoY Change |

2022 | $937 | — |

2023 | $1,241 | +$304 (+32%) |

2024 | $1,325 | +$84 (+7%) |

2025 | $1,298 | −$27 (−2%) |

Source: Quashed Index historical data. Actual premiums vary by profile.

The Lesson:

Insurers price risk differently. One insurer might heavily penalise drivers under 25, while another is actively targeting that demographic with competitive rates to grow market share. One provider might offer lower premiums for older Japanese imports; another might specialise in high-end European vehicles. These variations mean there is no ‘standard market price’ for your policy—only the price that individual insurers are willing to offer you at a given moment.

The Action:

Use the Quashed Market Scan before your renewal date every year and when you buy a new vehicle. Enter your details once and see comparable quotes side by side—same excess, same coverage type, same sum insured. If you find a better deal, switch. Loyalty should be earned by your insurer with competitive pricing, not assumed because changing feels like effort.

Final Verdict: Take Control of Your Total Car Ownership Costs

For New Zealand drivers, the true cost of running a car goes well beyond the purchase price. Rego fees have increased by around $50 per year since 2024 for most vehicles. WoF costs add $40–$100 annually. And car insurance—at an average of $1,298 per year—represents by far the largest ongoing variable cost, and the one over which you have the most control.

The figures make a compelling case for action. Drivers who don't compare insurance providers pay an average of $367 more per year for identical coverage. Over five years, that's $1,835 in unnecessary spending.

Beyond the financial case, the rego-WoF-insurance connection is one that every driver must understand. Letting your WoF or rego lapse is not just a legal risk—it is an insurance risk. An expired warrant creates grounds for claim denial if your vehicle’s condition contributed to an incident, potentially leaving you to absorb the full cost of an accident yourself.

Key Recommendation: Keep your rego and WoF current at all times. Compare your car insurance every year and whenever you switch vehicles using the Quashed Market Scan, and switch when you find better value. The few minutes this takes could save you significantly—money better spent on fuel, maintenance, or reducing your excess.

Related Reading

Ready to take a deeper dive into car and home ownership costs? The Quashed team has the guides you need:

Guide to Car Ownership in New Zealand: Rules, Costs and What You Need to Know to Save – A comprehensive breakdown of rego, WoF, insurance, and maintenance costs for NZ drivers.

Debunking Car Insurance Myths – Separating fact from fiction on coverage, WoF obligations, claim denials, and more.

Average Cost of Car, House & Contents Insurance in NZ 2026 – Regional cost breakdowns and the loyalty tax data that proves comparison pays.

House Insurance: A Homeowner’s Guide – If you own or plan to own a home, understand sum insured, regional pricing, and what’s covered.

8 Budget Hacks for House Insurance – Proven strategies to cut insurance premiums without sacrificing meaningful coverage.

Frequently Asked Questions: Car Registration and Insurance in New Zealand

How much does car rego cost in New Zealand in 2026?

From January 2026, the annual licence fee component increased by a further $25 for most passenger vehicles—the second staged increase since January 2025. Based on 1News reporting of the January 2026 changes, the 12-month licence for a standard petrol private passenger vehicle rose from approximately $144 to approximately $173 per year. Fees for other durations (3 or 6 months), diesel vehicles, electric vehicles, and motorcycles differ and can only be confirmed precisely via the NZTA Rightcar fee checker, as fee components vary by vehicle type.

Can my car insurance be voided if my WoF is expired?

Your insurer will not automatically decline a claim just because your WoF has lapsed. However, if your vehicle had a safety defect that would have caused it to fail a WoF—and that defect contributed to the accident—your insurer can decline your claim. Bald tyres, faulty brakes, or broken lights that caused or worsened an incident are common examples. Driving without a valid WoF is also a legal offence carrying a $200 fine. The safest approach is to keep your WoF current at all times.

What is the fine for driving with an expired rego or WoF in NZ?

Both offences carry a $200 infringement fee, which can be issued by police or parking wardens on public roads. Repeat offences or more serious compliance failures can escalate to vehicle impoundment. A $200 fine significantly outweighs the cost of a WoF ($40–$100) or a rego renewal, making prompt compliance always the financially rational choice.

Is car insurance compulsory in New Zealand?

No. Unlike many other countries, New Zealand does not legally require drivers to hold car insurance. However, given that ACC (the Accident Compensation Corporation) only covers personal injury—not vehicle damage—an at-fault driver is personally liable for the cost of repairing the other party’s vehicle. Without insurance, a single serious accident can result in a bill of tens of thousands of dollars. Over 90% of New Zealand drivers hold some form of car insurance.

How much can I save by comparing car insurance in New Zealand?

Based on Q4 2025 Quashed Market Scan data, 80% of drivers who compared car insurance found a cheaper policy, with average savings of $367 per year. The average difference between the highest and lowest quotes for equivalent coverage across insurers was $679 in Q1 2025. Use the Quashed Market Scan to compare quotes from multiple insurers on identical terms.

How often do I need to renew my WoF in New Zealand?

Vehicles first registered after 1 January 2000 require a WoF annually. Vehicles registered before that date require a WoF every six months. Brand new vehicles receive a WoF valid for three years from their first registration. You can check your WoF expiry date online via the NZTA website or through the NZTA Waka Kotahi app.

What does NZ rego actually pay for?

Your vehicle licensing (rego) fee in New Zealand covers several components: the annual licence fee (which funds road infrastructure and NZTA operations), an ACC motor vehicle levy (which funds injury treatment for road accident victims), and from July 2025, a standardised ACC levy for electric vehicles. Diesel vehicles pay a higher rego fee than petrol vehicles, and are also required to separately purchase Road User Charges (RUC) based on distance travelled.

Should I pay for 3, 6, or 12 months of rego?

Paying for 12 months upfront is generally the best value — as we note in our Guide to Car Ownership in New Zealand, this saves roughly 20% compared to renewing for 3 months. The 6-month option sits between the two in cost, and suits drivers who want some flexibility without paying the premium of quarterly renewals. If you're uncertain about continuing to use the vehicle, or it's due for significant maintenance, a shorter period may make more sense. You can also put your vehicle 'on hold' with NZTA if it won't be driven for an extended period, which pauses rego obligations without accruing debt.

Do multi-policy discounts still exist for car and home insurance in NZ?

As of early 2026, major insurers including AA Insurance, AMI, State, Tower, and Vero have discontinued multi-policy discounts (MPDs) for new and renewing customers, following regulatory action and significant penalties for failing to apply them correctly. The strategy of bundling all your insurance with one provider to receive a discount no longer applies for most Kiwis. Shopping around for the best rate on each policy separately is now the only reliable way to reduce costs.