Rethinking Insurance for First-Time Homebuyers

Buying your first home in New Zealand is a huge milestone—but finding affordable house insurance for first-time buyers? That’s not always exciting or straightforward. It’s tempting to think of insurance as just another bill. But what if it’s actually one of the smartest ways to protect your new home and your financial future? When done right, insurance doesn't have to drain your wallet. Instead, it’s a safety net that provides security and confidence. Let’s explore how first-time buyers like you can rethink house insurance—without feeling overwhelmed.

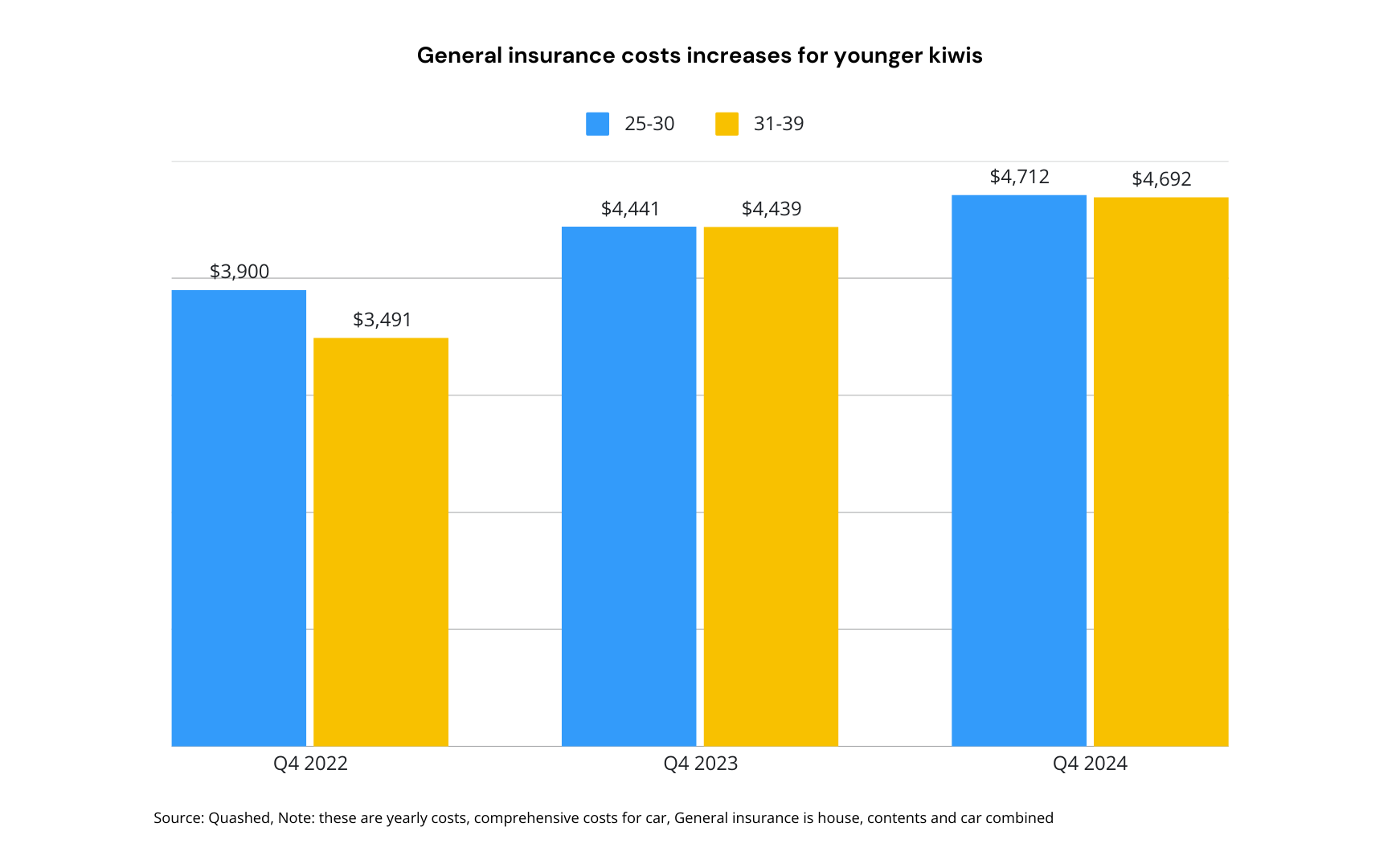

Younger generations and rising insurance costs

Insurance costs in New Zealand keep climbing, and younger Kiwis are feeling the pinch. According to the Quashed Index, general insurance costs (house, contents, and car combined) have surged over the past two years:

Ages 25–30: Up 20.8% from $3,900 (Q4 2022) to $4,712 (Q4 2024).

Ages 31–39: Up 34.4% from $3,491 (Q4 2022) to $4,692 (Q4 2024).

The sharpest jump happened between Q4 2022 and Q4 2023, and while the pace has slowed, costs remain high.

The chart below highlights these increases, showing how premiums have risen across both age groups.

Want to dive deeper into the reasons behind these increases? Check out our detailed analysis on why house insurance premiums are increasing and what it means for Kiwi homeowners.

Understanding why premiums are rising is the first step. But beyond managing costs, it’s important to see insurance as more than just another expense.

Let’s explore why insurance plays such a crucial role in your financial stability.

Why insurance is more than just a bill

Think of insurance as your financial safety net. Sure, we hope you never have to use it, but insurance is the tool that gives you peace of mind, security, and financial protection. Here are some reasons to reframe insurance as a crucial part of your financial strategy:

It’s your financial safety net (that’s getting pricier)

Insurance protects you when things go wrong. The Financial Services Council reports that while 98% of homeowners in New Zealand insure their homes, a staggering 80% of Kiwis lack income protection insurance, leaving many households vulnerable if sickness or job loss disrupts their income.

Unlike council rates, which are fixed, you can control your insurance

Platforms like Quashed allow you to compare policies for home, car, or contents insurance in one place, helping you find options that suit your needs and budget. However, 47% of New Zealanders struggle to balance risk and return when managing insurance, according to the Financial Services Council.

Beware of the risks of cheap coverage

Cheap as insurance policies might seem attractive, but they can leave you vulnerable. According to the Financial Services Council, underinsurance often occurs when people underestimate their coverage needs.

Insurance safeguards you from life’s uncertainties

In New Zealand, 91% of people see life and health insurance as valuable, yet only 41% have life insurance, according to the Financial Services Council. By protecting your home, health, and income, insurance lets you focus on living your life with confidence, knowing you’re prepared for the unexpected.

By reframing insurance as a proactive financial tool, you’re not just protecting what matters most—you’re building a stronger financial future.

Whether it’s freeing up cash for your KiwiSaver or finding smarter ways to balance costs and coverage, insurance can play a key role in your overall financial strategy.

Making insurance part of your financial plan

Insurance isn’t just another bill—it’s a powerful tool in shaping your financial future. The choices you make today, especially as a first-time homeowner, can have a big impact down the road.

Take KiwiSaver, for example. If you used it for your deposit, you’re likely thinking about rebuilding those savings quickly.

Here’s the thing: Making small changes to your house insurance—like shopping around or adjusting your coverage—could free up cash. For first-time buyers, this extra money can go straight back into KiwiSaver, helping you rebuild your savings faster. For instance, saving $300 annually on premiums could significantly grow your KiwiSaver over time, thanks to compounding returns.

Before you make any decisions, ask yourself:

Are you comparing insurance options regularly to get the best deal?

Would raising your excess reduce your premiums enough to make a difference?

How much more could your KiwiSaver grow if you reinvested these savings?

The right insurance doesn’t just protect your home—it protects your future. By making smart decisions today—such as comparing options or adjusting coverage—you’re setting the stage for a stronger financial foundation.

Ready to tackle the challenges of finding the best insurance as a first-time homebuyer? Let’s explore some practical strategies to help you navigate your options.

How can first-time homebuyers in New Zealand overcome insurance challenges?

Figuring out the best insurance deal can feel overwhelming, especially with so many options on the table. But here’s the good news: a few smart strategies can help you find the right policy for your needs and budget without the stress. Here are a few tips to get you started:

Bundle your policies

Bundling home, car, and contents insurance can save you money and simplify things. Many insurers offer discounts for bundled policies, but it’s not just about the savings—it’s about ensuring each policy meets your needs. Before committing, double-check that all the coverage options align with your situation.

Adjust your excess

Raising your excess (the amount you pay out-of-pocket on a claim) can lower your premiums, but you need to find an amount that you’re comfortable paying in case of an emergency. It’s all about balancing cost savings with real protection.

Shop around every year

Think twice before auto-renewing your policy. Insurance prices change regularly, so take the time to explore alternatives. Tools like Quashed make it easy to compare rates and find a deal that works for you.

Customise your coverage

Every home is different, so your house insurance policy should reflect that, especially for first-time buyers in New Zealand. If you’ve got an older home, for example, you may need extra coverage for repairs. A newer home might allow for more cost-effective coverage.

Insurance doesn’t need to be complicated. Small steps, like adjusting your excess or shopping around, can unlock significant savings and help you find the right policy.

Reimagine your house insurance

First-time buyer? Join 45,000+ Kiwis who have signed up for Quashed.

Compare house insurance in minutes—no stress, no calls, just tailored options for your home & budget.

Further reading

Check out these helpful reads:

8 Budget Hacks for House Insurance: Smart ways to cut your costs.

Average Cost of Car, House, and Contents Insurance: What Kiwis are really paying.

Why Are House Insurance Premiums Increasing?: The reasons behind rising costs.

House Insurance: A Homeowner’s Guide: Everything you need to know.

How to Compare House Insurance Quotes: Get the best deal easily.

Top House Insurance Questions: Straight-up answers to common questions.

Key Considerations for House Insurance: What to think about first.

FAQs

Why do I need house insurance before I’ve even moved in?

Most lenders require proof of house insurance before settlement to protect their financial interest in the property. Without it, your mortgage funds may not be released. It's best to arrange cover before settlement day to avoid delays.

How do I figure out how much house insurance I need as a first-time buyer?

Use a rebuild cost calculator to estimate the amount needed to fully rebuild your home in case of total loss. Avoid guessing, as under-insuring can leave you short, while over-insuring means you’re paying more than necessary.

Does house insurance cover everything inside my home?

No—house insurance covers the structure of your home, but not your personal belongings. To protect furniture, electronics, and valuables, you’ll need contents insurance. Many first-time buyers bundle both policies for better coverage and possible discounts.

Can I change my house insurance provider after I’ve bought my first home?

Yes, you’re not locked into one insurer. Many first-time buyers stick with the first policy they get for their mortgage, but you can switch anytime if you find a better deal. Just ensure there’s no gap in coverage when switching.

What’s the easiest way to save money on house insurance as a first-time buyer?

Choose a higher excess (you’ll pay more in a claim but save on premiums).

Bundle house and contents insurance for a discount.

Pay annually instead of monthly to avoid extra fees.

Compare policies regularly—prices and cover levels vary by insurer.

What’s the difference between house insurance and mortgage protection insurance?

House insurance covers damage to your home. Mortgage protection insurance helps cover your mortgage payments if you’re unable to work due to illness, injury, or redundancy. Some lenders may offer it as an option when setting up your loan.

Does house insurance cover damage from earthquakes or flooding?

Yes, but coverage varies. Earthquake cover is partly funded by EQC (Earthquake Commission), with private insurers covering additional damage. Flood cover depends on the insurer, so check your policy details, especially if buying in a high-risk area.

This article provides general information only and does not constitute insurance or financial advice. Insurance policies vary between providers, and you should check with your insurer or a licensed adviser for guidance specific to your situation. For full details, refer to Quashed’s terms and conditions.