Contents insurance is an important policy for both homeowners and renters alike.

If your home, or the property you rent, was to suffer from a fire, natural disaster, accident, water damage or theft, it is likely that some or all of your possessions would also be impacted.

Contents insurance covers the loss of your personal possessions.

It covers the replacement of everything in your house that isn’t attached to the structure of the building itself. This includes items such as jewellery, appliances, furniture, clothes, bedding and curtains, so that when your home is fixed or rebuilt, you can also afford to replace lost possessions.

This article will explain everything you need to know about contents insurance in New Zealand, from whether you need it, how much coverage you should have, how much it costs and extra things to look out for.

Do I Need Contents Insurance?

As with most insurance policies, contents insurance is optional but advisable.

Gambling on your assets is risky business, but having contents insurance protects you from the unplanned expenses that would come with having to replace some or all of your personal belongings.

If you consider the amount that it would cost to replace all of your things, only you can decide whether that’s an amount that you’d be comfortable having to pay. (Top tip - the amount that it all adds up to is often more than people expect.)

But contents insurance also protects you for individual items that could get lost, broken or stolen. Items most commonly claimed in contents insurance policies are phones, laptops and jewellery.

Do I Need Contents Insurance if I’m Renting?

Many people purchase contents insurance at the same time as house insurance when they purchase a property. But contents insurance is just as important for renters as it is for homeowners. After all, the risk of losing your possessions in a fire or through theft is arguably no different if you’re a renter or homeowner.

In saying that, if you are a student, or just renting a room with few valuable possessions, you may decide against contents insurance until you have furnished a house, or simply choose the lowest tier of cover that includes your phone and laptop. (Check out our guide to flatting in New Zealand if this is you.)

But bear in mind that some contents insurance policies actually cover kids who are studying at university, under their parents’ coverage, so this is worth checking out. On the other hand, if you are renting a whole house and own items such as a washing machine, couches, television or sports equipment, then purchasing contents insurance would be a sensible choice.

Lastly, many people don’t realise that contents insurance often provides temporary accommodation cover which is particularly beneficial for renters. The cost of temporary accommodation, if you are displaced from your home, can quickly mount up into the tens of thousands.

The average Kiwi household can save

$2,023.79 a year by shopping their insurance!

Find out how your renewal prices stack up against other options out there!

What Doesn’t My Contents Insurance Cover?

What your contents insurance policy doesn’t cover will depend on the policy you buy. But as a rule, it pays to double-check that your policy covers your phone and laptop, as this isn’t a given, and in New Zealand, phones are the most common item to have claims made for.

If you want to know more about contents insurance for your tech, particularly Apple products, have a read of our article comparing contents insurance to AppleCare.

You may also need to check other items specifically such as kayaks, bikes and carpet. Carpet is usually considered a part of house insurance, so many contents insurance policies only cover loose floor coverings such as rugs. However, some policies do cover carpet, so if this is something that is important to you, it’s worth checking.

Lastly, it’s not enough just to check that an item is included, but how much it is covered for, as even with a policy worth $50,000, individual items will have limits. For example, jewellery may have a limit of $1,500 per item, or there may be a limit of $5,000 for artwork.

How Much Contents Insurance Should I Get?

You have a few options when it comes to calculating the amount of contents insurance that you should buy.

Make a List

The DIY method involves tallying up everything you own according to its current value. This could be more accurate if you have fewer possessions than the average Kiwi in your living situation, but be careful not to forget anything!

Use an Online Valuation Tool

Using an online tool is the most straightforward way to calculate the value of your personal possessions. Online options use information such as the number of rooms in your property and the number of people living in the house to estimate the value of your contents. Alternatively, Quashed’s contents valuation tool provides prompts to ensure that you have included all of your possible possessions when making your list.

Use a Valuer

For items such as jewellery or antiques that have been gifted or passed down from family members, it can be hard to know what they’re worth. Your best option in this case is to get each item valued by a professional so that you know exactly how much to insure it for.

How much contents insurance you choose to buy could vary from anywhere from $2,000 to over $100,000. But as a rough guide, an average two-adult household usually has contents worth around $50,000-$80,000.

Whichever route you take to decide on a figure, be sure to review it regularly so that you always have the level of cover you need, and you’re not paying more than you need to in premiums.

To get you started, below are two example lists for working out the value of your possessions. However, these are just starting points, and it’s important to note that the actual list and associated values vary a lot from person to person and family to family.

Young Professional (Age 25, Renting) | Family of Four (Homeowners) | ||

|---|---|---|---|

Item | Cost | Item | Cost |

Electronics (Phone, laptop, TV) | $2,500 | Electronics (Phone, laptop, TV) | $5,000 |

Sports Equipment | $1,000 | Sports Equipment | $3,000 |

Lounge Furniture | $2,500 | Lounge Furniture | $3,500 |

Bedroom Furniture | $1,500 | Dining Furniture | $2,500 |

Kitchenware (Cutlery, plates, pots, pans etc.) | $1,000 | Bedroom Furniture | $5,500 |

Appliances (Fridge, washing machine, microwave) | $3,000 | Kitchenware (Cutlery, plates, pots, pans etc.) | $2,000 |

Clothes and Accessories | $3,000 | Appliances (Fridge, washing machine, microwave) | $6,500 |

Sheets and Towels | $500 | Clothes and Accessories | $8,500 |

Artwork | $1,000 | Sheets and Towels | $2,000 |

Jewellery | $1,000 | Jewellery/Watches | $3,000 |

Toys and Games | $2,000 | ||

Books and Media | $1,500 | ||

Artwork | $4,000 | ||

Total: | $17,000 | Total: | $49,000 |

Shop smarter with Quashed

Insurance just got way easier with Quashed. Compare, shop and track all your insurance in one place.

How Much Does Contents Insurance Cost?

How much your contents insurance will cost depends on the amount of cover you choose, the excess you select, and what inclusions you add on.

Cover refers to the sum insured amount that you select. This is the maximum amount that could be paid out to you in a claim.

Excess is the contribution payment that you have to make when you make a claim, before you are paid out. How much you choose is entirely up to you, based on how much you’re happy to pay in the event that you have to make a claim.

Premiums are the monthly or annual payments that you make to purchase your insurance policy and to stay covered.

Lower cover and higher excesses result in lower premiums. Higher cover and lower excesses result in higher premiums.

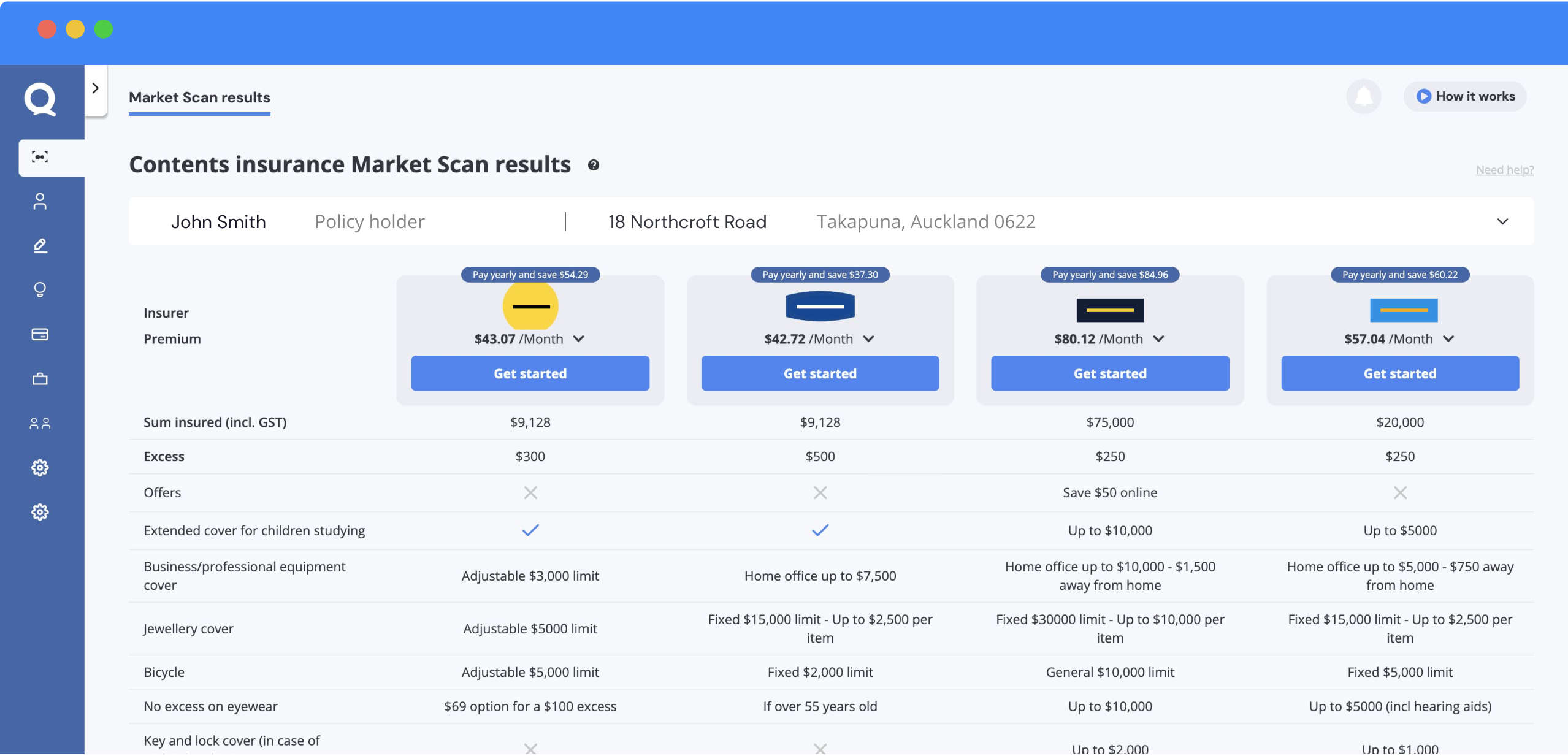

Now that we’ve got that sorted, let’s take a look at how different insurance policies compare. The table below shows a range of annual premium options for a female living in Wellington with $50,000 of cover and a $500 excess.

Renter (Age 25) | Renter (Age 35) | Renter (Age 45) | Homeowner (Age 25) | Homeowner (Age 35) | Homeowner (Age 45) | |

|---|---|---|---|---|---|---|

AA | Unavailable at time of scan | $670 | $630 | $640 | $585 | $540 |

AMI | $970 | Unavailable at time of scan | Unavailable at time of scan | Unavailable at time of scan | Unavailable at time of scan | Unavailable at time of scan |

Tower | $885 | $785 | $750 | $780 | $585 | $540 |

State | $1,040 | $955 | $870 | $975 | $585 | $540 |

TradeMe | $1,010 | $900 | $850 | $885 | $855 | $755 |

For these premiums, AA, State and TradeMe are providing a high level of cover, while AMI and Tower provide medium coverage.

But premiums aside, it’s essential to compare each policy in more detail. For example, while AA is the only of these insurers to offer coverage for an elderly relative in a rest home, it is the only provider which doesn’t include illegal credit card use. There are also large variations in liability cover, ranging from State’s $1 million, to Tower and TradeMe’s $20 million.

As another example, glasses and hearing aids are some of the most commonly claimed for items in New Zealand, and while these things will likely be included in your policy, the excesses vary, and some providers only cover these items for people aged 55 and over.

With these things in mind, the best contents insurance policy for you might not necessarily be the cheapest, but the one that includes the kind of coverage you prioritise.

Market Scan quotes are direct from insurers

So you won’t pay more with Quashed

Things to Look For in Your Policy

As mentioned above, different insurers provide slightly different forms of coverage in their contents insurance policies.

Different policies may or may not include:

Extended cover for children studying

Business/professional equipment cover (ie. home office)

Mobile phone and laptop cover

Watercraft cover

Compromised cover if you are away from home for more than 60 days

Temporary accommodation cover

Spoiled food/perishables

Vet bills

These are just a few examples. There are many more factors to compare, and how important each inclusion is will depend on your personal situation.

Use Market Scan for Easy Comparisons

When deciding between policies, the easiest way to compare premiums and different types of cover is to use Market Scan.

Market Scan does the research for you and matches policies to your criteria from multiple insurers. You can then select the right policy for you with all of the information in front of you.

How to Save on Your Contents Insurance

Besides from shopping around for the best deal, there are other things that you can do to make sure you’re only spending what is necessary to get the coverage you need.

Accurately work out the value of your possessions

This might sound like common sense, but if you take the easy route of an automated valuation, you may end up over-valuing your possessions and paying a higher premium than necessary. If some of your stuff is second-hand or worn out, or you’re fairly minimalist with your stuff, then less coverage might be adequate.

Increase your excess

Just as with any other kind of insurance policy, agreeing to a higher excess means that your premiums are lower. Just make sure that you will be able to afford the excess that you select in the event that you have to make a claim.

Keep an Eye on Price Changes

The price of insurance fluctuates from year to year, and there are no rules saying that you have to stick with the same insurer if there are better deals to be had elsewhere. Just make sure you take into account the possibility of a no-claims bonus before you leave your current insurer.

Use the Same Insurer for all of your Policies

On the other hand, it may pay to stick with the same insurer if you have multiple policies. Some companies offer bundle deals for different types of insurance that may save you money on individual premiums.

Hopefully you’ve found this information useful and feel confident that you know how to begin your contents insurance journey. If you want to keep reading, we have more information about contents insurance here.